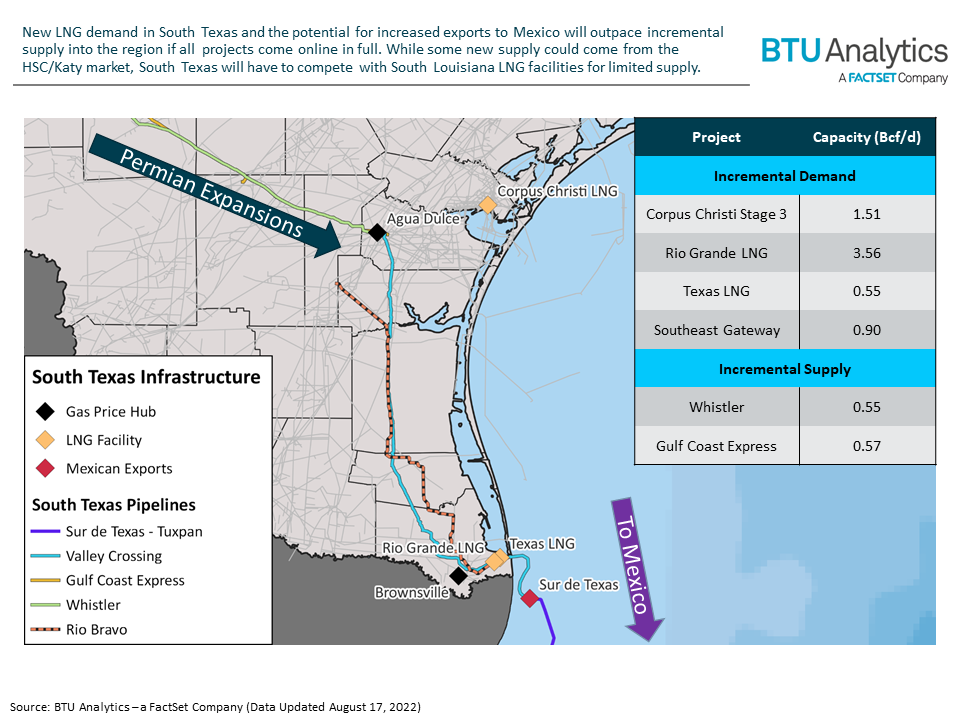

BTU Analytics has written extensively about the midstream challenges that are materializing as US LNG demand along the Gulf Coast continues to grow. While most of the attention has been focused on Southern Louisiana, especially given the concentration of LNG facilities in the region, a similar set of challenges to supplying LNG is developing in South Texas. With three US LNG facilities making progress and the potential for new export demand in Mexico, the South Texas region could become short gas within the next five years without new pipeline infrastructure.

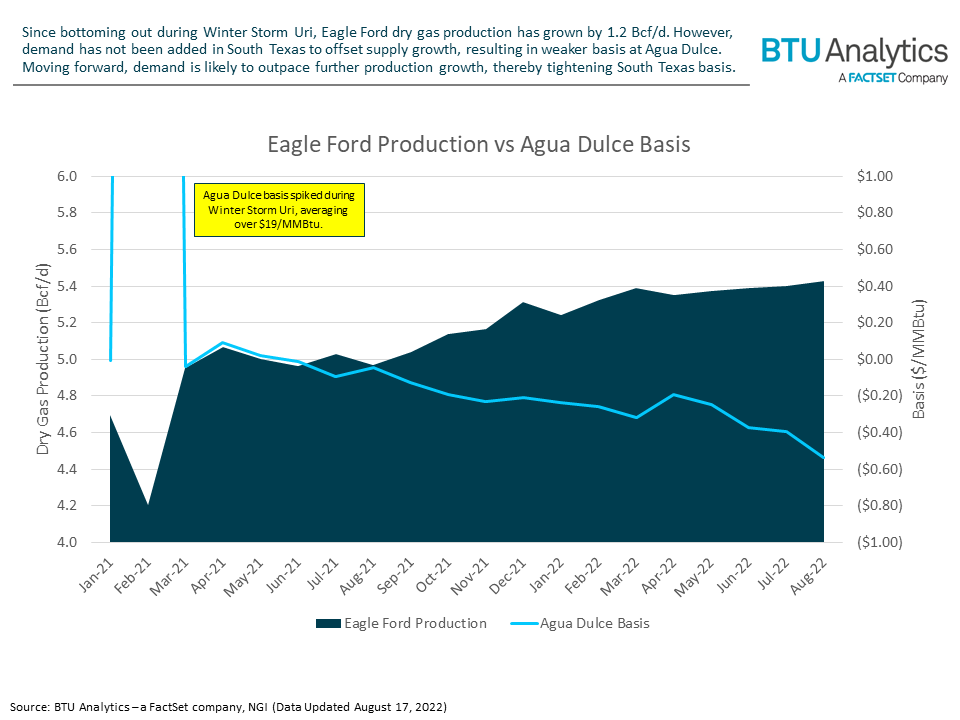

Over the past two years, South Texas basis has weakened in response to growing dry gas production in the Eagle Ford and increased flows from the Permian. In March 2021, after Winter Storm Uri upended the Texas gas market, basis at Agua Dulce averaged just $(0.04)/MMBtu. Since then, basis has gotten progressively weaker, with July 2022 averaging $(0.40)/MMBtu. Over the same period, Eagle Ford dry gas production has increased by 0.44 Bcf/d, a 9% increase compared to March 2021 levels. With demand growth in South Texas currently limited to increased exports to Mexico, the growth in supply has outpaced demand, thus contributing to weaker basis.

However, that dynamic could be set to shift in the coming years as new US LNG facilities and the potential for new Mexican exports could outpace incremental supply into South Texas. Cheniere has made positive FID on the Corpus Christi Stage 3 Expansion (1.51 Bcf/d). Neither Texas LNG (0.55 Bcf/d) nor Rio Grande LNG (two phases totaling 3.56 Bcf/d) have made FID yet, but both facilities have announced offtake agreements and pipeline supply agreements that indicate they could move forward as early as the end of 2022. That demand alone is enough to upset the balance in South Texas, but the imbalance between supply and demand could be further exacerbated by new demand in Mexico. New Fortress Energy has signed an agreement with Mexico’s CFE to build an LNG export hub while TC Energy announced a deal to build a new 1.3 Bcf/d pipeline to serve demand in Southeast Mexico. Both projects would likely source gas out of South Texas via the Sur de Texas pipeline off the coast of Brownsville.

Crucially, this level of demand growth far outpaces new sources of inbound supply. Whistler Pipeline has made FID on an expansion that would expand capacity by 0.55 Bcf/d, and Kinder Morgan is considering an expansion to Gulf Coast Express that would add 0.57 Bcf/d, although that project does not appear to be moving forward at this time. Regardless, the collective expansions are not enough to meet incremental demand if all projects come online. While additional supply could likely be sourced from further up the Gulf Coast, South Texas demand will have to compete with LNG facilities in South Louisiana for limited supply in the HSC/Katy market. Without significant growth in the Eagle Ford or the addition of a new greenfield pipeline, South Texas could be left short gas with significant impacts on Agua Dulce basis. BTU Analytics will be covering South Texas basis dynamics in depth in the upcoming August edition of our natural gas basis report: the Gas Basis Outlook. Request a sample below or by emailing btuanalytics@factset.com.