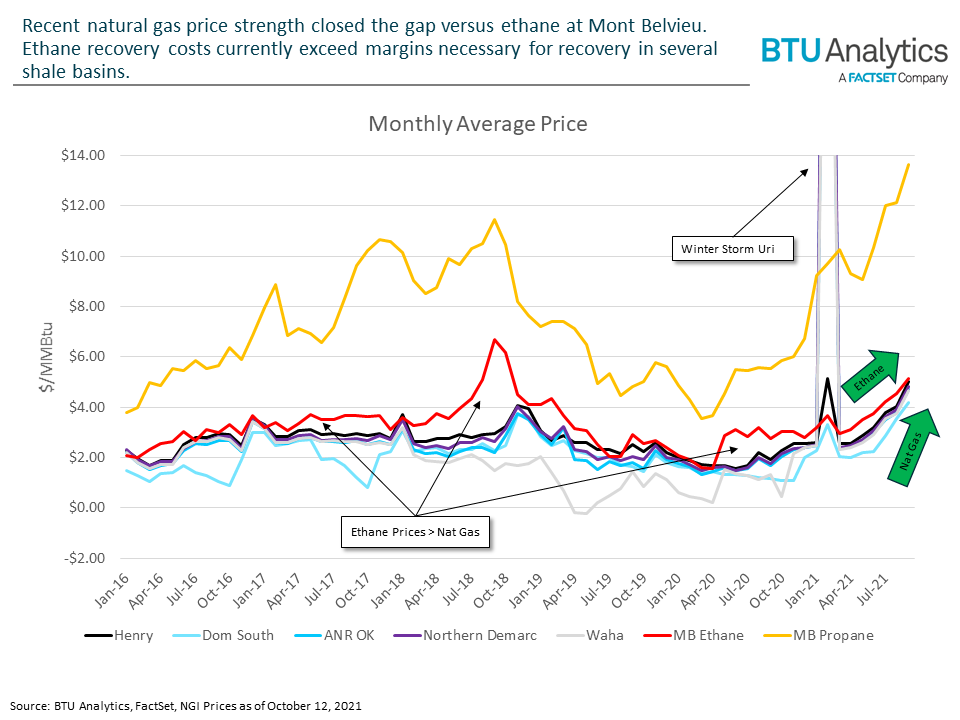

Ethane prices have been on the rise in 2021, reaching levels at Mont Belvieu that have not been observed since 2018. Propane pricing is climbing even faster as we approach winter with US propane/propylene stocks that are below the five-year average according to the latest weekly EIA report. Despite strong NGL prices, a threat to ethane recovery is emerging – natural gas prices. In today’s Energy Market Insight, BTU Analytics will outline how recent commodity pricing dynamics challenge the economics of ethane recovery.

Natural gas liquids pricing is typically linked to movements in crude prices; however, ethane deviates from these correlations. Instead, ethane pricing typically moves in relation to Henry Hub – until it doesn’t. Natural gas prices have rallied in recent weeks amid tepid supply growth heading into the winter storage withdrawal season, but ethane prices have not risen at the same rate, as shown below.

The acceleration of increasing natural gas prices at key pricing points, such as Henry Hub, ANR (Oklahoma), Northern Demarc (Williston), and Waha (Permian) has closed the gap known as the ethane frac spread in recent months. Even Dom South, which suffers from pricing pressure due to congestion as the Northeast remains takeaway capacity constrained, has tightened the ethane frac spread recently. A small amount of propane is usually recovered in tandem with ethane, but its proportion of the incrementally recovered y-grade mixture is small enough that propane’s price strength has limited impact on the economics of ethane recovery. The ethane frac spread must be wide enough to cover incremental transportation and fractionation (T&F) costs incurred to economically recover ethane, which has been jeopardized by recent gas price strength. Natural gas production is fetching better prices than we’ve seen in the US in many years, which could pressure producers to reject ethane if incremental costs of recovery are outweighed by higher realized natural gas prices.

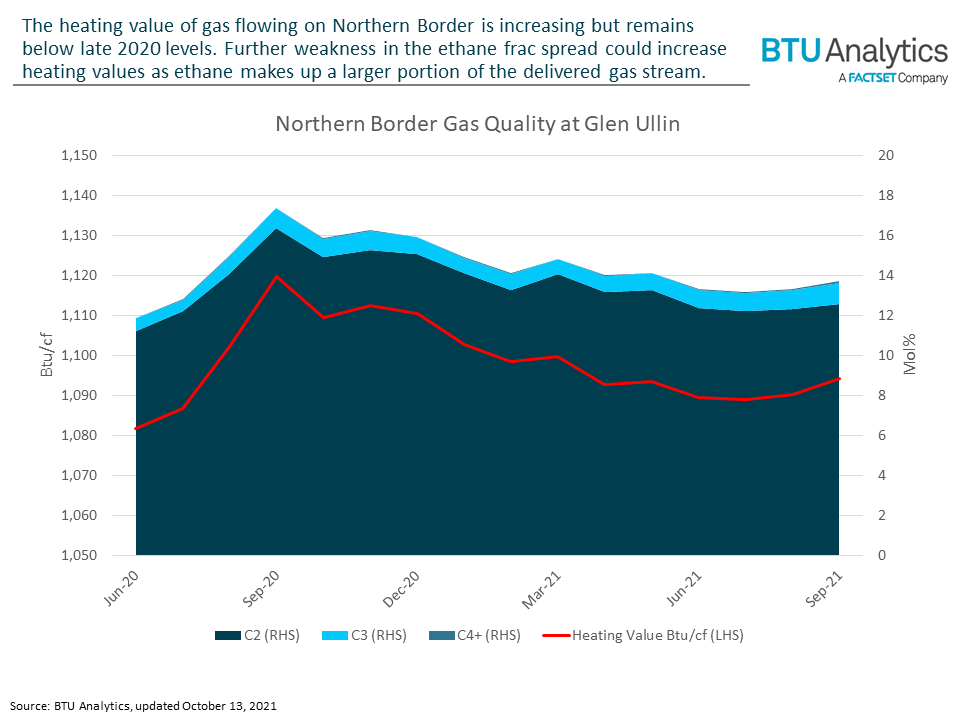

As a result, ethane that would otherwise be recovered at current Mont Belvieu pricing will instead be finding its way to market blended into the natural gas takeaway pipes. The limitation to this dynamic is that the gas flowing on long-haul takeaway pipes cannot exceed a heating value specified in each pipe’s tariff, typically around 1,100 Btu/cf. One region where ethane rejection has been widely observed historically is the Williston Basin, where most of the produced natural gas flows on Northern Border. While Northern Border does not currently have an upper limit on the heating value of its supply, displacement of leaner Canadian volumes by Williston Basin gas has pushed the heat content of gas flowing on Northern Border higher, potentially creating issues for downstream pipes that do have limits, such as NGPL.

The chart below highlights the heat content of natural gas on Northern Border just downstream of the Bakken. High T&F costs for ethane have historically limited ethane recovery in the region, and as shown on the right hand side of the chart, ethane makes up roughly 12% of the gas stream on Northern Border and is the primary driver of higher heat content for natural gas on the pipeline.

Due to the high T&F costs in the Williston Basin and lack of upper heat content restrictions on Northern Border, it is unlikely that ethane recovery will increase materially until the ethane frac spread widens. However, the decision to recover ethane might not be entirely driven by economics in other regions. Permian producers’ unhedged natural gas production is likely to include more rejected ethane volumes in the near term, potentially filling gas takeaway capacity sooner than previously anticipated. Many producers’ recent commitments to ESG goals, including reducing flaring, might force ethane recovery regardless of the ethane frac spread in the Permian Basin. For more information about BTU Analytics’ ethane production forecast, see BTU Analytics’ Upstream Outlook.