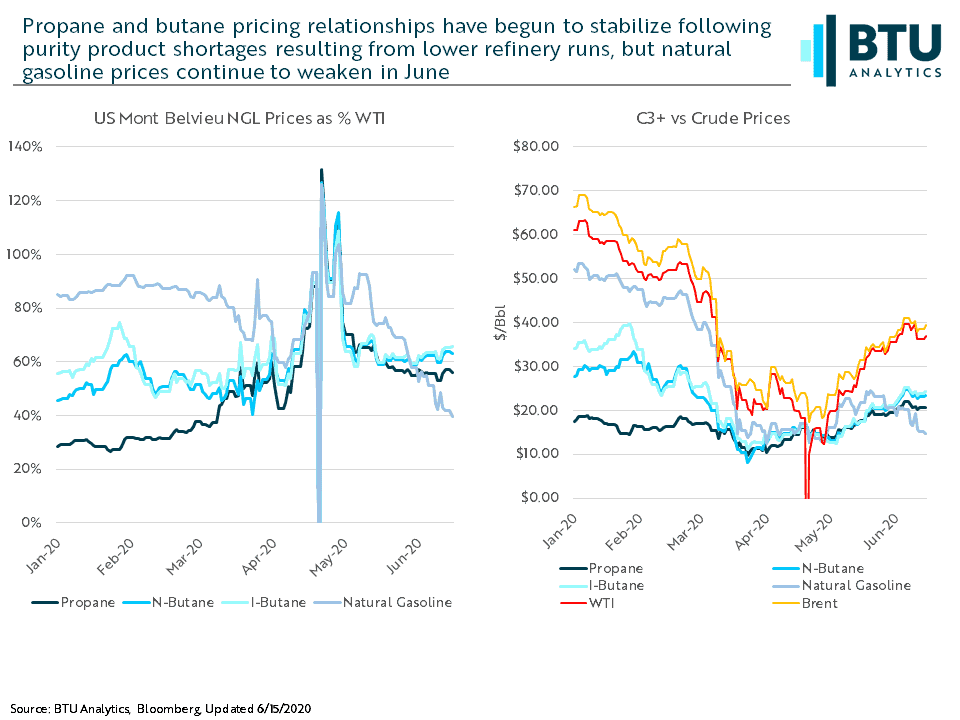

Earlier last month, BTU Analytics’ Energy Market Insights examined the supply outlook and historical prices for natural gas liquids (NGLs). NGL production plummeted in April as associated gas production declined from oil-directed curtailments and refineries reduced throughput. These two supply impacts diminished April’s NGL supply faster than global demand fell, causing purity product prices for NGLs to skyrocket. More recently, we’ve begun to see a bifurcation. While propane and butane prices have stabilized relative to WTI, natural gasoline pricing continues to weaken.

Natural gasoline historically maintained the strongest pricing relationship to WTI. The 2020 YTD average price at Mont Belvieu for natural gasoline stands at 78% of WTI compared 85% in 2019. However, more recently, a barrel of natural gasoline was valued at $14.70 at the end of trading on June 15, 2020, a mere 40% of what WTI spot prices closed at. Conversely, propane pricing continued to maintain strength, valued at 56% of WTI on June 15, up from just 40% of WTI on average in 2019. Pricing for NGLs is typically correlated to their heat content, but in a COVID-impacted world, these conventions have been thrown out the window.

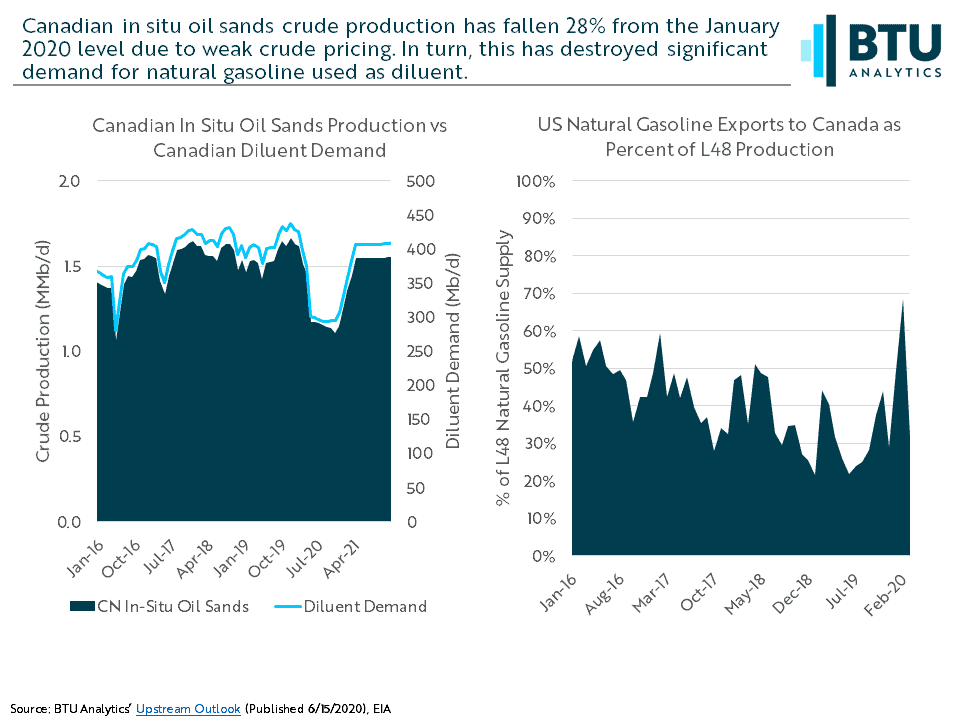

US natural gasoline demand comes primarily from Canadian exports and motor gasoline blending. Today’s analysis will focus on the demand impact of exports to Canada because they made up 69% of US Lower 48 natural gasoline supply in February 2020, which was a seasonal peak compared to 2019’s average of 31%. These exports are used primarily as diluent for crude produced from Canadian in situ oil sands and allow the highly viscous oil to flow more easily through pipelines. As seen in the chart above, Canadian in situ oil sands crude production has fallen 28% from January 2020 to just under 1.2 MMb/d in June due to crude pricing weakness and oil storage constraints. Barring a sudden major pricing improvement for crude, the outlook for Canadian oil sands is mostly static for the balance of 2020, giving no additional support to natural gasoline demand. Propane, by comparison, has much more inelastic demand, which is supported by heating and cooking needs. The source industry of purity product demand is critical as end users are now in various stages of transitioning back to “normal” after governments took actions to stunt the spread of the novel coronavirus.

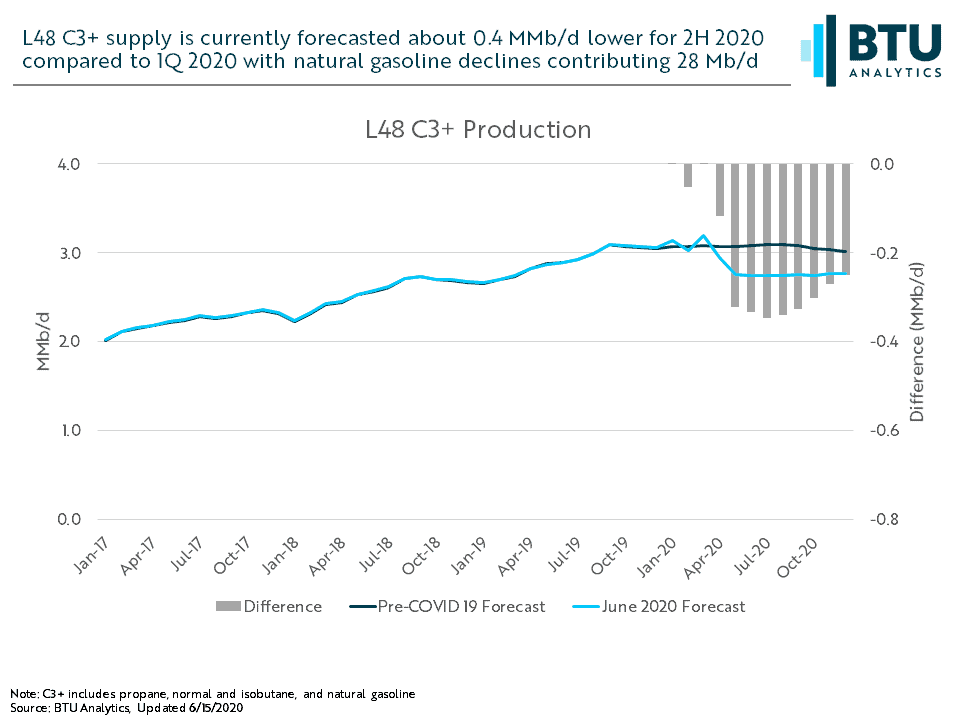

Our June outlook estimates that 2H 2020 C3+ supply will average 0.4 MMb/d lower than 1Q 2020. For the remainder of 2020, natural gasoline production is expected to average 28 Mb/d lower than average 1Q 2020, whereas diluent demand is expected to remain 120 Mb/d lower for the remainder of 2020 compared to 1Q 2020. Given that demand destruction for natural gasoline as diluent alone outpaces supply cuts by roughly 90 Mb/d in the remainder of 2020, it is quite likely that natural gasoline supply will continue to outpace total demand.

For more information on BTU Analytics’ supply outlook for NGL production forecasts, request information about our Upstream Outlook.