In the wake of second quarter earnings last month, BTU Analytics discussed how NGL pricing in 2019 compares to historical averages as operators shift to liquids-rich portions of their acreage. Purity product pricing dipped well below five-year averages this year, further eroding NGL uplift. After gas processing and fractionation costs are weighed against natural gas liquids revenues, is it still advantageous to target regions that yield mostly natural gas liquids? Today’s commentary quantifies the flipside of last month’s NGL pricing analysis – the declining NGL uplift at current natural gas liquid prices.

Typically, pricing for the propane plus fractions of the NGL stream makes their removal at gas processing plants an obvious financial benefit. However, given weak NGL pricing in 2019, the costs of gas processing and NGL fractionation vs. the NGL revenue have reached nearly (and sometimes below) zero.

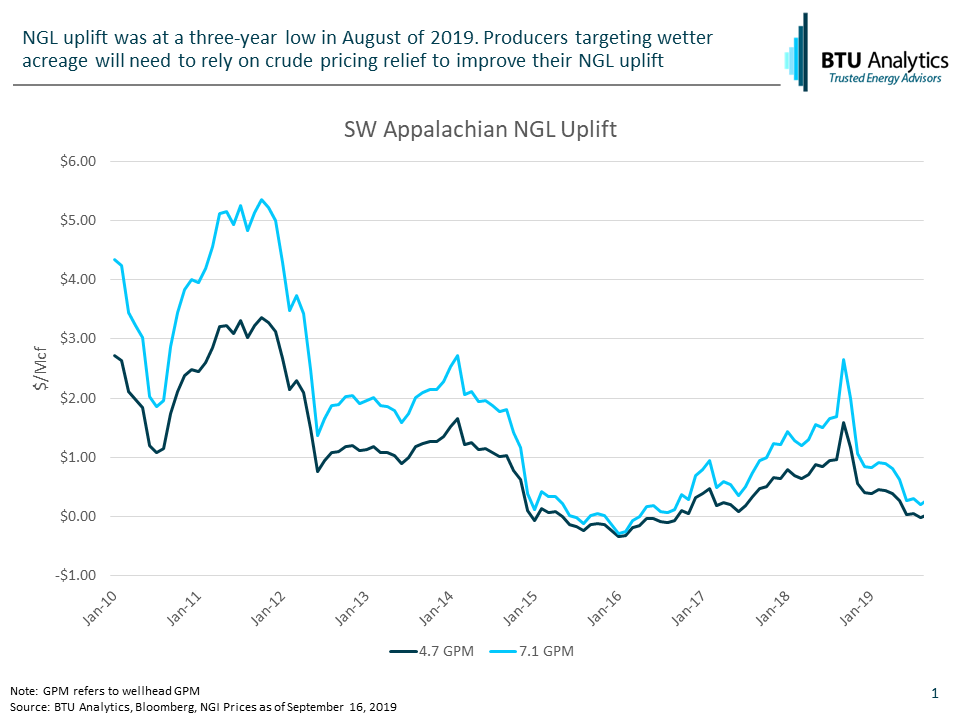

Above, the calculated NGL uplift compares the profitability from 1 Mcf of gross gas processed at a typical Southwest Appalachian processing plant to a hypothetical case in which NGLs were left in the gas stream or producers were paid the natural gas equivalent value for their NGLs. This hypothetical case ignores the real-world constraint of dry gas pipeline specifications that limit the maximum heat content of gas transmitted. For example, Tennessee Gas Pipeline (TGP) limits the heat content to 1,110 BTU/scf and below. However, producers can capture this outcome via keep whole contracts with processors and were often utilized prior to the MLP boom.

The two scenarios above depict the produced gas heat content measured at the wellhead. Gross gas containing 1,200 BTU/scf roughly equates to 4.7 GPM at the wellhead, and 1,300 BTU/scf is about 7.1 GPM. For reference, the average 2019 production-weighted GPM for Range Resources’ (NYSE: RRC) wells comes out to approximately 5.1 GPM (1,220 BTU/scf). For the drier 4.7 GPM scenario, uplift dropped to -$0.01/Mcf using average August 2019 commodity pricing, implying producers opted not only for ethane rejection but bypassing processing entirely if pipelines could accommodate the higher heat content of the gross gas. There is still positive NGL uplift for wetter 7.1 GPM gas wells, measuring $0.20/Mcf at the same point in time. Regardless of GPM, Southwest Appalachian uplift hasn’t been this low since September of 2016.

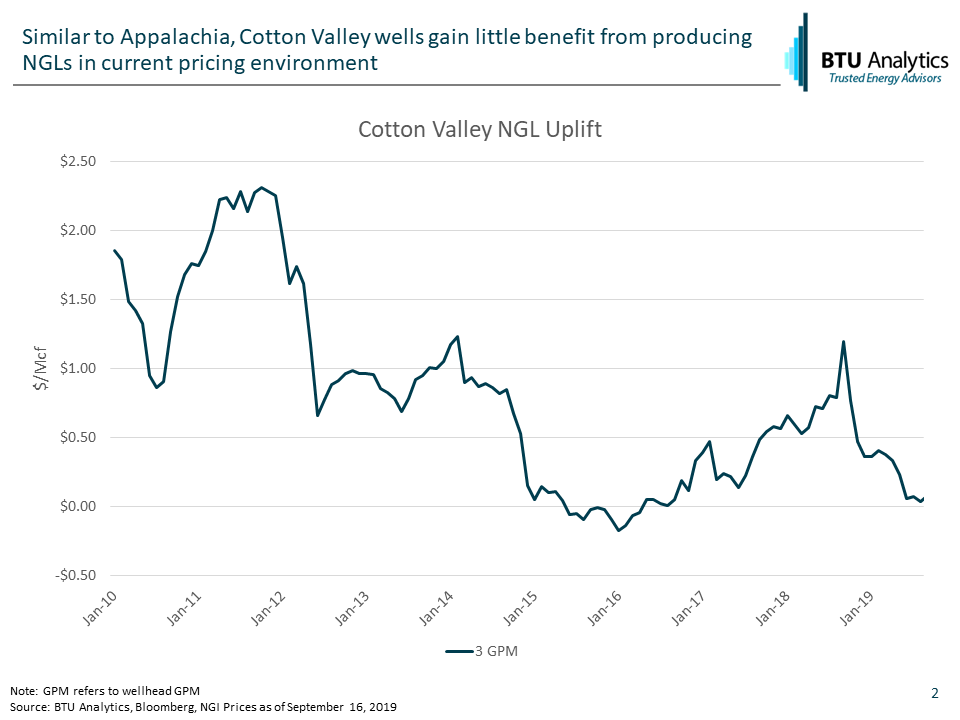

Another wet gas play affected by this NGL uplift dilemma is Cotton Valley. With production-weighted GPMs coming in around 3 in BTU’s Carthage sublocation in East Texas, there are fewer molecules available in the gross gas stream to process into liquids than in Southwest Appalachia. The scenario depicted above, 3 GPM (1,140 BTU/scf), shows nearly zero NGL uplift in recent months, down from $1.20/Mcf one year ago despite closer proximity to Mont Belvieu and lower overall processing costs.

Today’s weak NGL prices are compounding already weak natural gas pricing for gas-focused operators. With recent strength in crude pricing due to international tensions, liquids pricing may benefit in the short term, but can demand for natural gas liquids keep up with supply growth? BTU Analytics provides answers to these types of questions and more through our Upstream Outlook service.