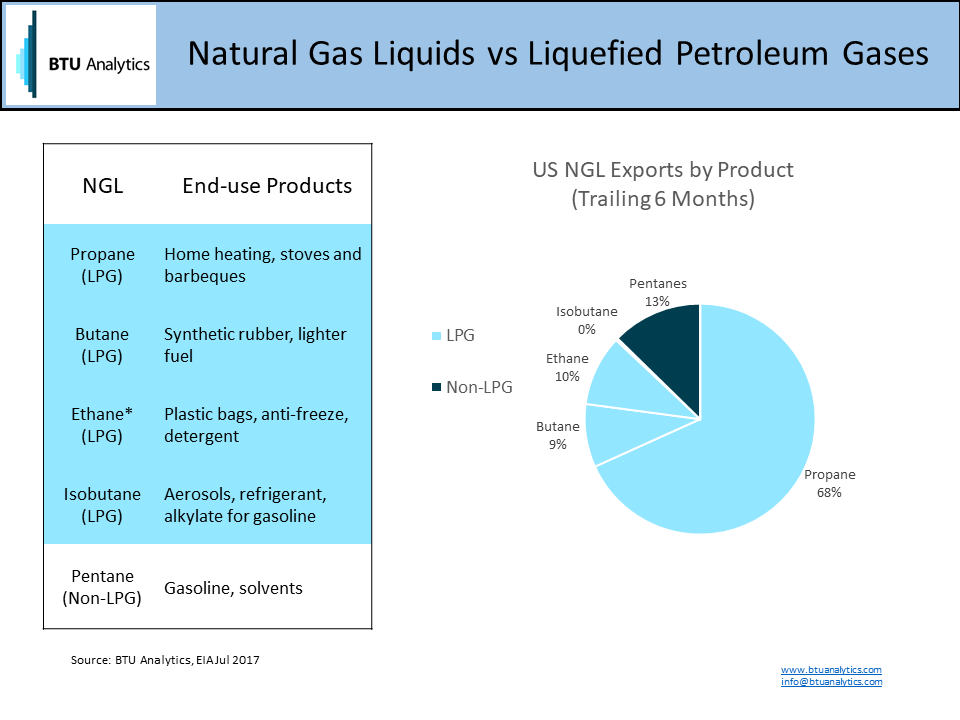

Per the World Health Organization, almost three billion people cook and heat their homes using biomass (agricultural waste, firewood, animal dung, etc.), and the resulting indoor pollution causes approximately four million premature deaths each year. Many developing countries are transitioning to more efficient fuel sources such as Liquefied Petroleum Gases (“LPG”), which include fuels, or mixes of fuels, like propane and butane (think BBQs and lighters). Ethane is included in the EIA’s definition of LPGs; however, LPG typically refers only to propane and butane. LPGs are a subset of Natural Gas Liquids (“NGL”), and propane has historically dominated the NGL / LPG export mix.

LPGs are stable liquids at warmer temperatures and lower pressures than natural gas, making them easier and cheaper to transport and store. Those properties also make them good transitional fuels for developing countries that lack an interconnected pipeline network. India, for example, is investing in infrastructure to improve LPG access for poor households, converting around 100 million households to LPG between 2016 and 2019 by some estimates. Per Bloomberg, India has now surpassed Japan as the second largest LPG importer, trailing only China.

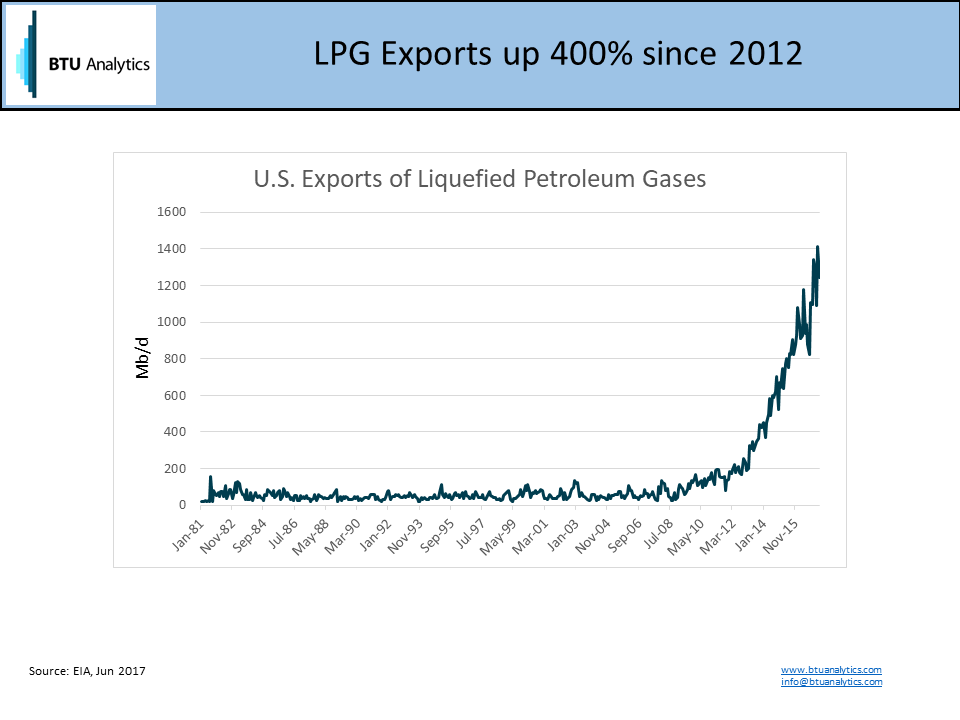

In the United States, the implications for growing global LPG demand have been clear. In 2012, the US became a net exporter of LPG. The US is now the largest LPG exporter in the world, and NGL processing capacity continues to expand. Ongoing NGL pipeline projects, including Enterprise’s, recently announced Shin Oak pipeline (250 Mb/d), Targa’s Grand Prix pipeline (300 Mb/d), and DCP’s Sand Hills pipeline (85 Mb/d) will increase capacity to export hubs on the Gulf Coast. These pipeline projects complement concurrent processing plant expansions, as well as several new ethane crackers in Texas. Greater pipeline capacity and processing capacity will enable more products to reach the Gulf for export.

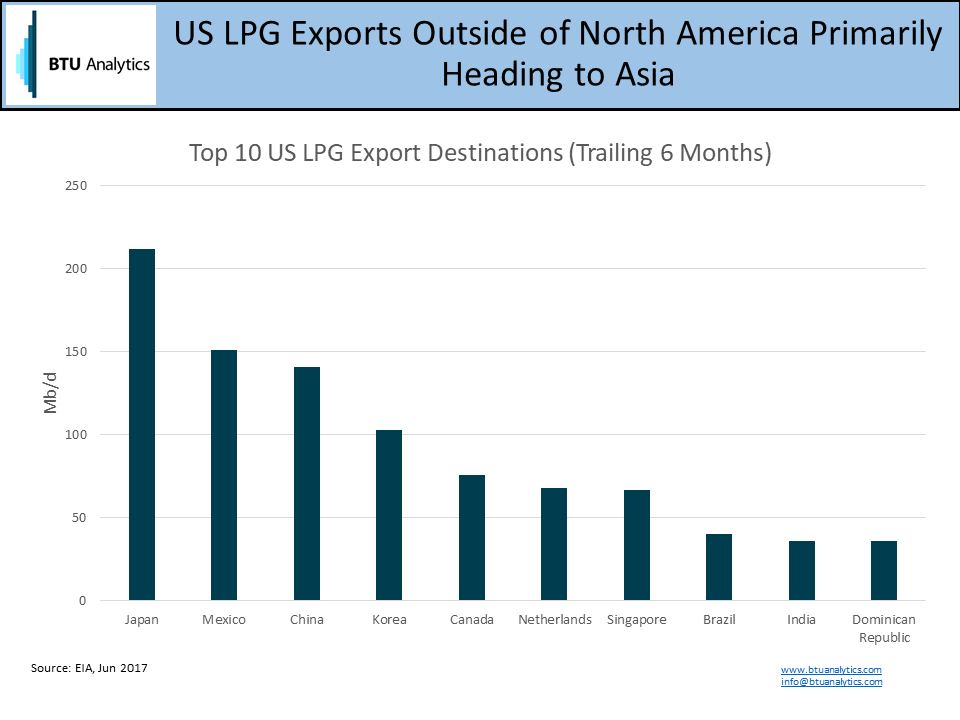

NGL economics are important for maximizing producing hydrocarbon streams. LPG demand from developing countries is a growth opportunity within the NGL value chain, which is evident by looking at the top 10 export destinations for US cargoes in the chart below. As the middle classes develop in these countries, and as countries like Japan transition away from LPGs towards natural gas, it will be important for US LPG products to be competitive with other oil producing regions, especially the Middle East.

The US is expanding capacity to process and transport NGLs, and as capacity expands, producers have additional flexibility to transport and sell volumes, which is important because NGL economics can impact investment and production decisions. In this price environment, producers must delicately balance producing enough volume to generate sustaining cash flow without producing themselves, and each other, into insolvency. The expanding NGL market may influence future investment decisions for upstream and midstream companies, which might have significant regional implications in the US. Learn more about BTU Analytics’ NGL forecast in the latest Upstream Outlook.