Since the announcement of Apache’s Alpine High discovery in the Delaware Basin in 2017, the company has rapidly advanced its development. Alpine High has since become an important piece of Apache’s portfolio, as shown by the company’s relationship with Altus Midstream and natural gas commitments on the new Gulf Coast Express and Permian Highway pipelines. Now more than two years into developing the Alpine High, Apache announced Alpine High will now need to compete with other Apache assets for capital. With this in mind, today’s analysis will analyze the potential impacts to the Permian if Alpine High development ceased.

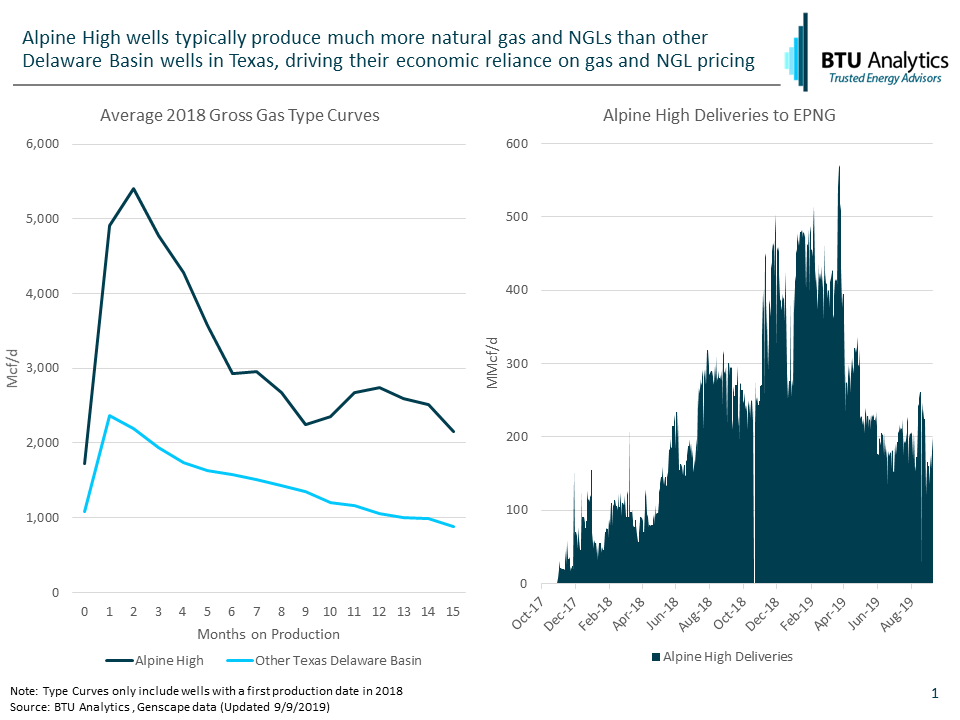

Alpine High is different than other development areas in the Permian. In the core areas of the Midland and Delaware, wells produce 60-90% liquids, but in the Alpine High, wells typically yield significantly more natural gas than liquids. The chart below on the left shows average 2018 gross gas type curves in the Alpine High and elsewhere in the Texas portion of the Delaware Basin. Gross gas type curves in the Alpine High show IP rates almost 130% higher than elsewhere in the Texas Delaware Basin. Given this higher gas production, and lower oil production, gas, and NGL pricing generally impact Alpine High well economics much more than elsewhere in the Delaware Basin.

This came to a head during the spring as Waha natural gas pricing weakened to as much as negative $9/MMbtu. Waiting on the startup of the Gulf Coast Express, which would provide 2 Bcf/d of relief to Permian natural gas production (of which Apache has contracted 500 MMcf/d), Apache elected to shut in Alpine High volumes instead of accepting depressed Waha pricing. Ahead of the impending full startup of Gulf Coast Express, some Alpine High volumes are likely still shut in, as shown by the chart above on the right. The chart above does not represent all Alpine High volumes as some volumes are flowing into intrastate pipelines.

It’s no secret that, in addition to depressed Waha pricing, benchmark natural gas prices at Henry Hub have been near historic lows this summer. To the extent that weak natural gas pricing continues, Apache may find it more prudent to use capital previously dedicated to Alpine High in more oily assets, like its Midland Basin acreage. Based on BTU Analytics’ E&P positioning report estimates as of 2Q2019, Alpine High wells completed since 2018 show an average gas breakeven of more than $5/MMbtu. However, Apache’s Midland assets, which are more sensitive to oil economics, show oil breakevens of less than $45/bbl on wells completed since 2018. The breakevens in Apache’s portfolio indicate that at current pricing Alpine High development may struggle to compete for capital if historical well performance alone dictates future investment.

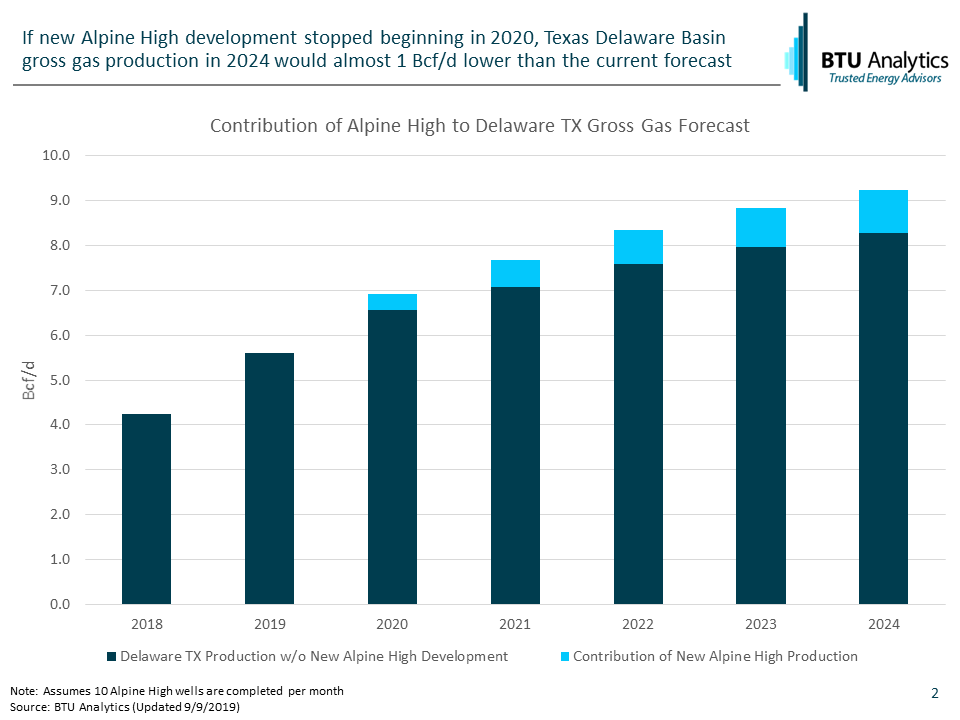

The chart below shows what Texas Delaware Basin gross gas production could look like if Alpine High development fell to zero beginning in 2020. A lack of new Alpine High development would result in gas production an average 960 MMcf/d lower than BTU Analytics’ current forecast for the Texas Delaware Basin by 2024. This represents more than 10% of the current gross gas forecast for this region and 4.5% of the total Permian forecast.

However, it’s likely that this capital would be funneled elsewhere in the Permian. If Apache were to complete 10 wells per month in the Midland Basin instead of the Alpine High (split evenly between the Central and Southern Midland Basin), that would represent an additional 240 MMcf/d of gross gas production in 2024. Overall, this shifting of activity from the Alpine High to the Midland Basin represents gross gas volumes 720 MMcf/d lower than the current forecast in 2024.

While there are many important factors to consider before shifting capital from Alpine High to another asset, including pipeline commitments, gas processing commitments, LNG terminal buildout, and natural gas and NGL pricing outlook, a shift out of the Alpine High could have a large impact on overall Permian gross gas volumes. To see BTU Analytics’ view on natural gas pricing over the next five years, request a sample of the Gas Basis Outlook. Additionally, BTU Analytics recently published a study on LNG Wave 2 buildout including where midstream constraints may develop, what infrastructure is needed to meet Wave 2, and where the US could source the necessary supply.