US LNG demand has had a record-setting month in April. Feedgas deliveries to US LNG export facilities averaged over 11 Bcf/d. While 2020 was a disruptive year for US LNG, Wave 1 facilities are now almost fully operational and appear to be poised for a much better summer in 2021. As April comes to an end, a combination of strong international prices, depleted European natural gas storage, and continued Asian demand growth point to strong summer LNG demand for US LNG exporters.

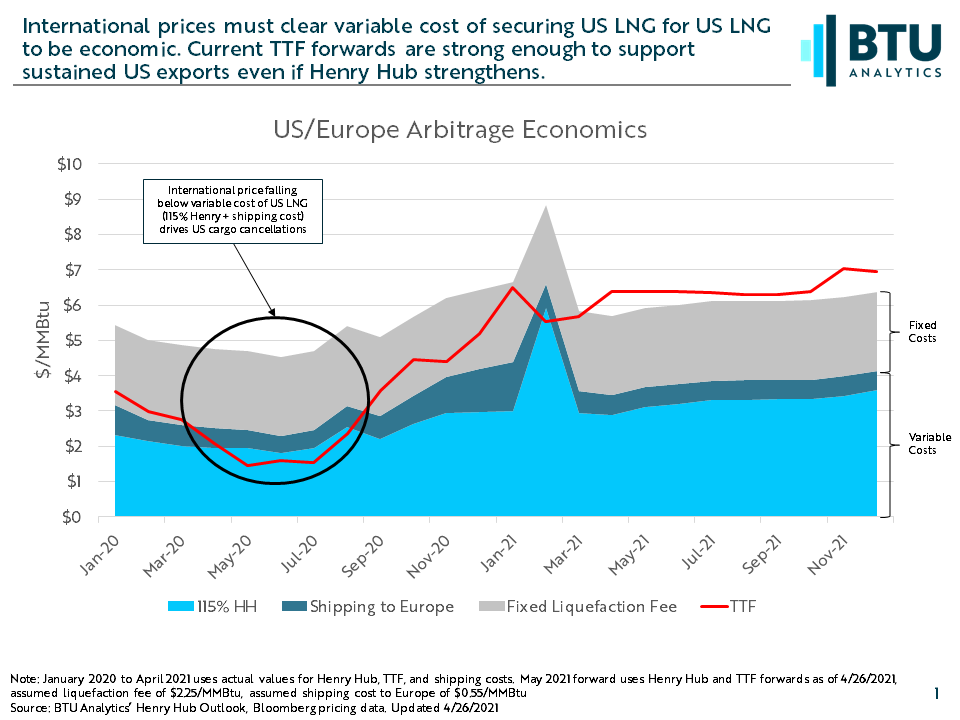

First, the biggest driver of US LNG exports is international pricing. European and Asian natural gas prices are being supported by low storage inventories in Europe and strong demand growth in Asia. 2020 provided a demonstration of the fragility of US LNG exports as demand destruction from COVID-19 led to plummeting prices in Europe and Asia. Cratering prices for natural gas abroad resulted in numerous cargo cancellations from the US. In 2021, the risk of cargo cancellations looks increasingly unlikely given the current strength in international natural gas prices. Natural Gas forward strip pricing for the remainder of summer at TTF (Northwest Europe) currently sits at $6.35/MMBtu. JKM (Asia) is slightly higher at $8.00/MMBtu. Even with the recent strength observed at Henry, $2.84/MMBtu on April 26th, spreads to both Europe and Asia are strong enough to cover a fully loaded cargo with room to spare. Barring a collapse in global pricing, these spreads should be conducive to sustained US LNG exports through the summer.

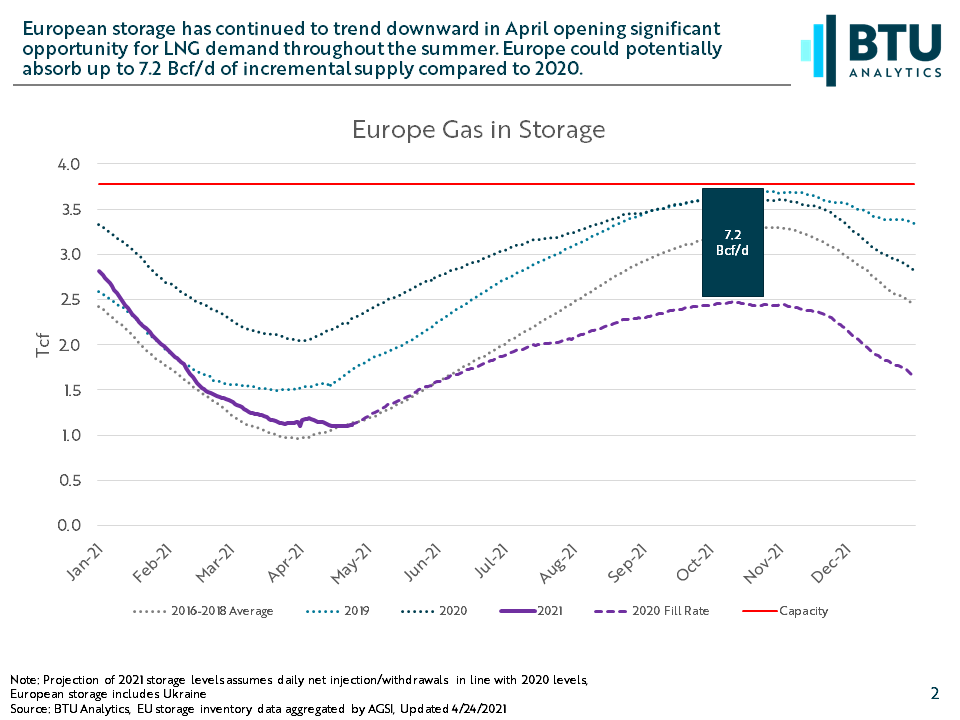

One of the primary factors driving strength at TTF is the historically low level of natural gas in European storage. As of April 24th, European gas storage sits at 1.12 Tcf. Inventories are now 0.61 Tcf lower than the same point in 2019 and nearly 1.17 Tcf lower than in 2020. Low inventory in storage gives Europeans plenty of room to absorb increased LNG imports in 2021. In 2020, Europe added 1.56 Tcf over the course of the summer to inventory. If that refill rate were to continue in 2021, Europe would be projected to reach just 2.45 Tcf by the end of October leaving nearly 1.33 Tcf of spare storage capacity. With 184 days between the start of May and end of October, Europe could potentially absorb up to 7.2 Bcf/d of incremental gas relative to 2020, all else equal.

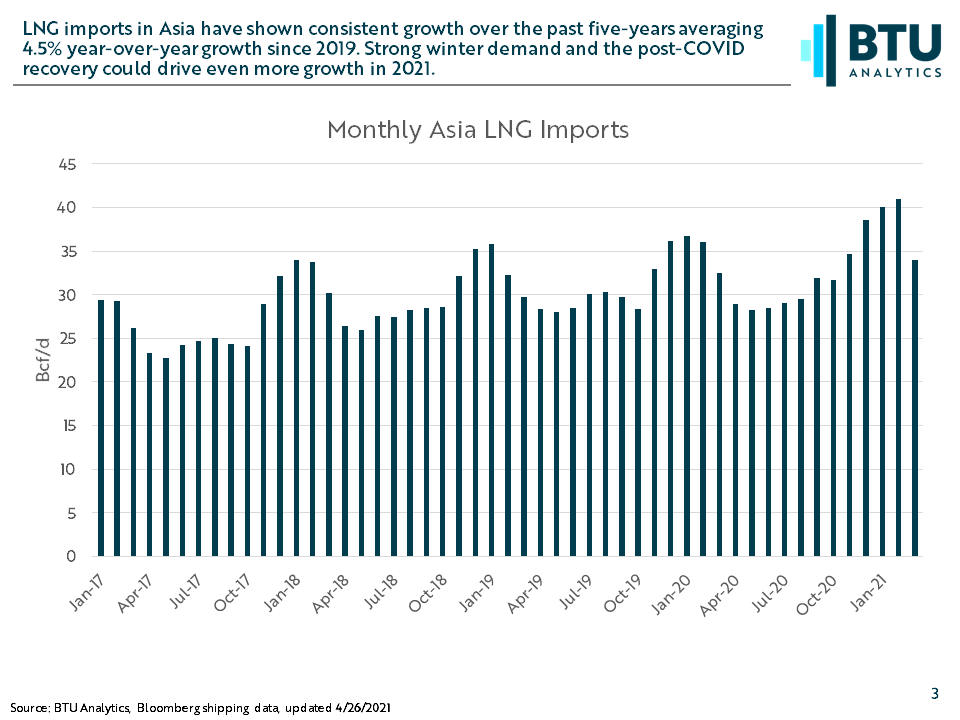

While European storage refill demand alone could be enough to incentivize full US LNG utilization this summer, Asian demand is also likely to increase this year providing further support. One of the factors driving the European storage deficit has been increased Asian LNG imports during the Winter of 2020-2021. An extremely cold start to winter sent Asian demand soaring in December and January. Asian LNG imports increased by an average of 2.8 Bcf/d or an 8% increase compared to the previous winter. Strong winter imports continued a trend of growth in Asian LNG imports that is likely to continue in 2021 despite ongoing COVID-related issues. Since the beginning of 2019, Asian imports have increased by an average of 4.5% year-over-year. Assuming just average growth in Asia would result in an incremental 1.35 Bcf/d of demand for global LNG.

With all signs pointing to growing demand for LNG in both Europe and Asia, US LNG is well positioned to capitalize on a tight global gas market. While certain risks remain, including increased supply from global LNG competitors, current dynamics indicate a strong summer ahead for US LNG. For BTU Analytics’ forecast for US LNG and its impact on the US gas market, request a sample of the Henry Hub Outlook.