In Tuesday’s Energy Market Commentary, BTU Analytics raised the question, which pipeline is the next to get cancelled or delayed? With both Northeast Energy Direct Pipeline (NED) and Constitution losing out to permitting battles and opposition forces, it is certainly not unquestionable to assume more greenfield projects will feel the burn of activists who oppose new fossil fuel infrastructure. While NED and Constitution both targeted New England markets, what happens if a major Southbound pipe gets the ax or delayed significantly? Under this scenario, two major greenfield pipes come to mind: Atlantic Coast Pipeline (ACP) and Mountain Valley Pipeline (MVP), both slated for a 2018 in service date. While both projects being cancelled seems unlikely, what impact would the cancellation of one have or significant delays in both pipelines?

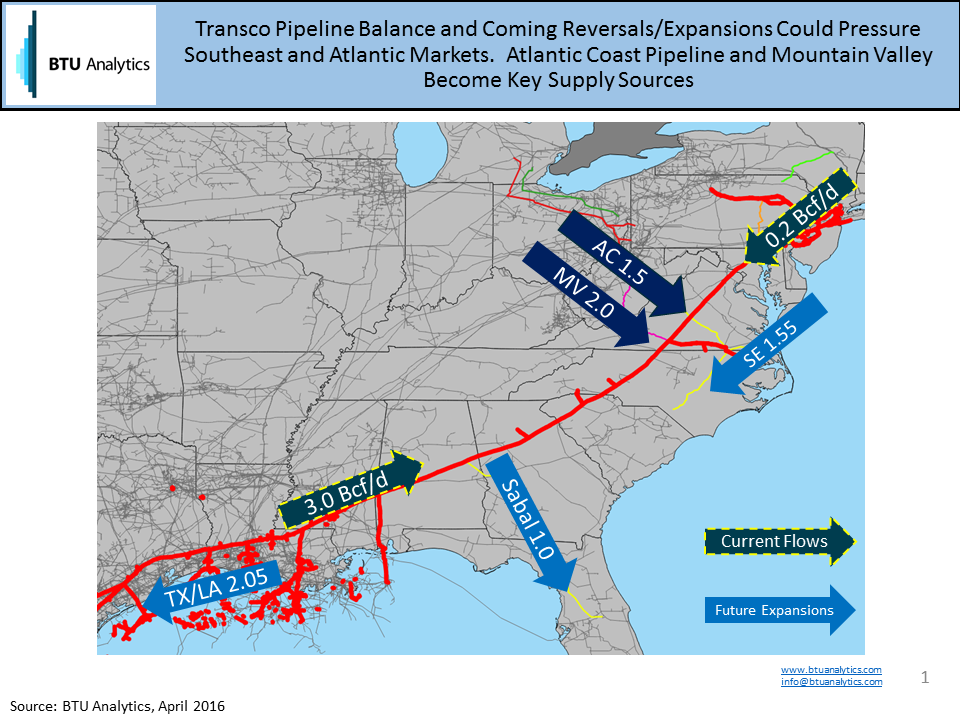

Atlantic Coast Pipeline plans to bring natural gas from West Virginia to utilities and power generators in Virginia, North Carolina and eventually into the Southeast via an interconnect with Transcontinental Gas Pipeline (Transco), the only major north/south interstate pipeline that currently serves the Southeast and Atlantic Coast markets. A look at current Transco natural gas flows show that approximately 3 Bcf/d of natural gas flows north from the station 85 compressor on the pipeline from the Gulf region. But change is on the horizon. In 2017, Sabal Trail Pipeline is scheduled to enter service, taking up to 1 Bcf/d of gas from Transco and transporting it into the Florida market to serve natural gas fired power plants. New demand is also emerging in Texas and Louisiana due to increased Mexican and LNG exports combined with new industrial projects means that competition for gas supply serving the Transco Station 85 market will only increase.

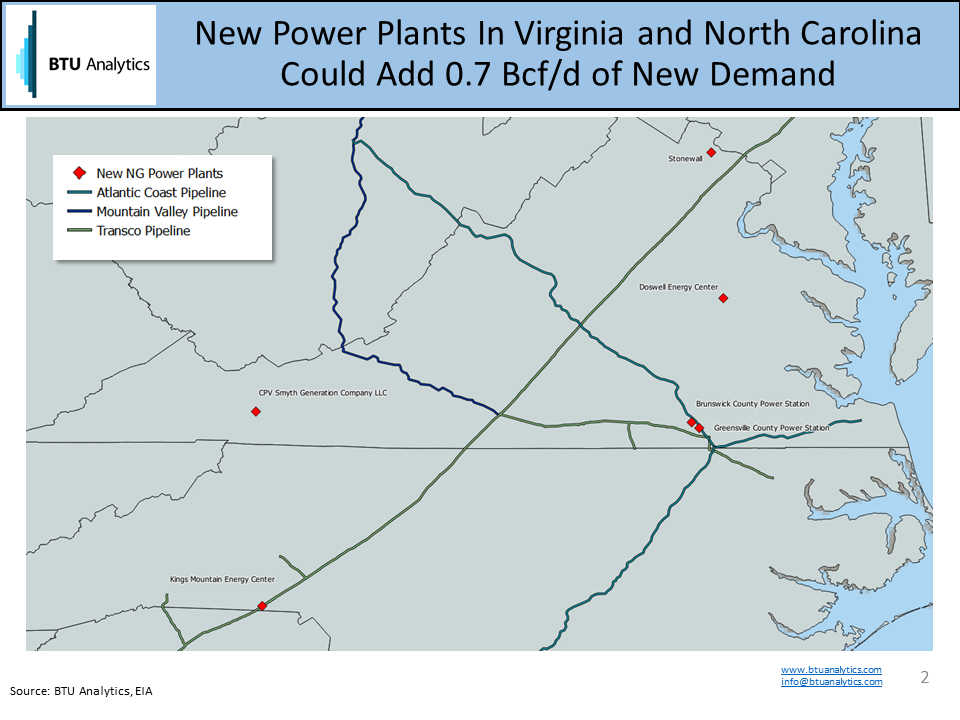

This all means less natural gas makes its way past the Sabal Pipeline interconnect in Alabama and ultimately into Georgia, the Carolinas, and Virginia. Combined, these markets averaged 5.1 Bcf/d of demand in 2015, up from 4.6 Bcf/d in 2014. Power demand accounted for the largest increase in 2015, up 0.69 Bcf/d and totaling 2.7 Bcf/d, representing just over 50% of demand. New power demand in the region is coming as well. The map below shows the location of 6 new natural gas fired power plants that at an 80% utilization rate would represent an additional 0.7 Bcf/d of demand.

With this much demand on the line, it is no surprise that Atlantic Coast pipeline is almost fully subscribed by power facilities, with 79% of the committed volumes headed to natural gas electric generators. This volume equates to 1.1 Bcf/d of power burn demand, a sizable chunk compared to the 2.7 Bcf/d consumed in the region in 2015.

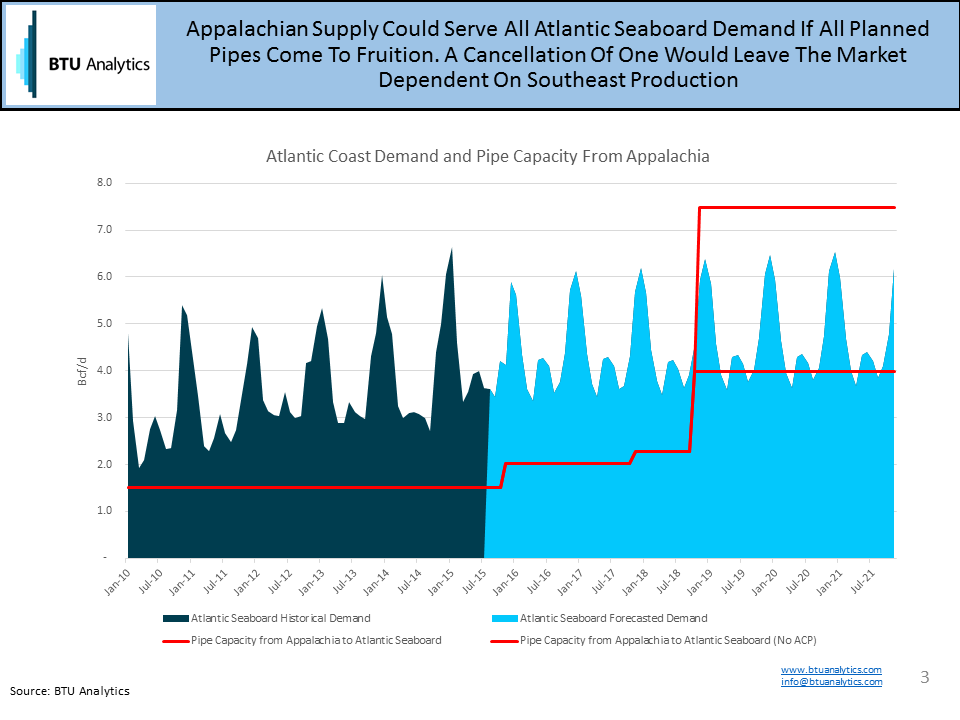

So what happens going forward as a handful of market forces collide in the Southeast? As the chart above shows, if all planned pipelines into the Atlantic Coast are realized, the region would have ample supply for future demand growth. Any cancellation of a project would leave the region dependent on Southeast and Gulf production. For more information on the ever evolving US natural gas infrastructure build out and supply and demand ramifications, request a sample of BTU Analytics’ Northeast Gas Quarterly.