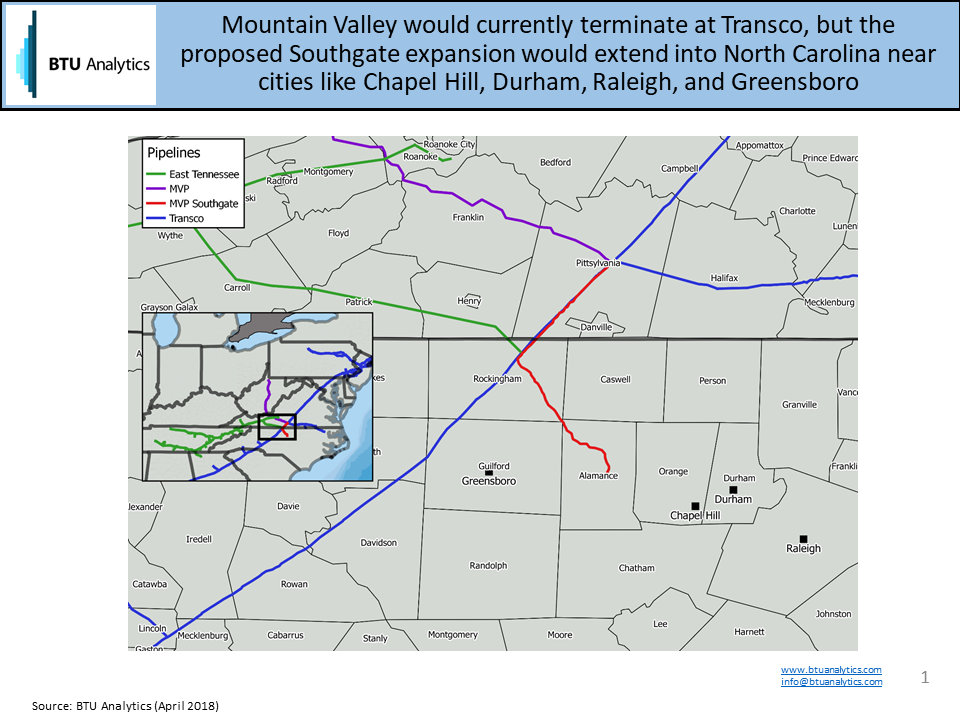

Last week, Mountain Valley Pipeline (MVP) announced an open season for Mountain Valley Pipeline Southgate (MVPSG) that would extend the 303-mile pipeline another 70 miles into North Carolina. PSNC Energy, a local natural gas distribution company, is the anchor shipper to take delivery of the volume, with MVPSG targeting a late-2020 startup. MVP is an important project that we discuss monthly in our Northeast Gas Outlook, and environmental opposition makes for an interesting discussion, but today we’ll dive deeper into the expansion project. Even though the MVP Southgate expansion will not allow incremental production growth out of Appalachia, it could provide an opportunity for improved Appalachia producer netbacks but will price and demand growth justify the project?

MVP will currently terminate at Transco, where shippers would then need to utilize Transco to transport gas downstream to demand markets in the Gulf and Atlantic Seaboard. Since MVP was first proposed, Transco’s null point has continued moving south, a topic we’ve looked at in previous publications, and with supply growth targeting Transco’s overwhelming demand growth in the Atlantic Seaboard, we expect to see the null point continue moving south. Driving the null point further south will be a combination of new projects including MVP. The chart below highlights the change in flows on Transco over the last several years.

The Transco pipeline will be gaining additional supply upstream of MVP through the Atlantic Sunrise project (1.7 Bcf/d) and PennEast Pipeline (1.0 Bcf/d), which are expected to be online in 2018 and 2019. Additionally, Atlantic Coast Pipeline will likely capture demand currently served by Transco in the Carolinas when the pipeline adds 1.5 Bcf/d of capacity from Appalachia in late 2019.

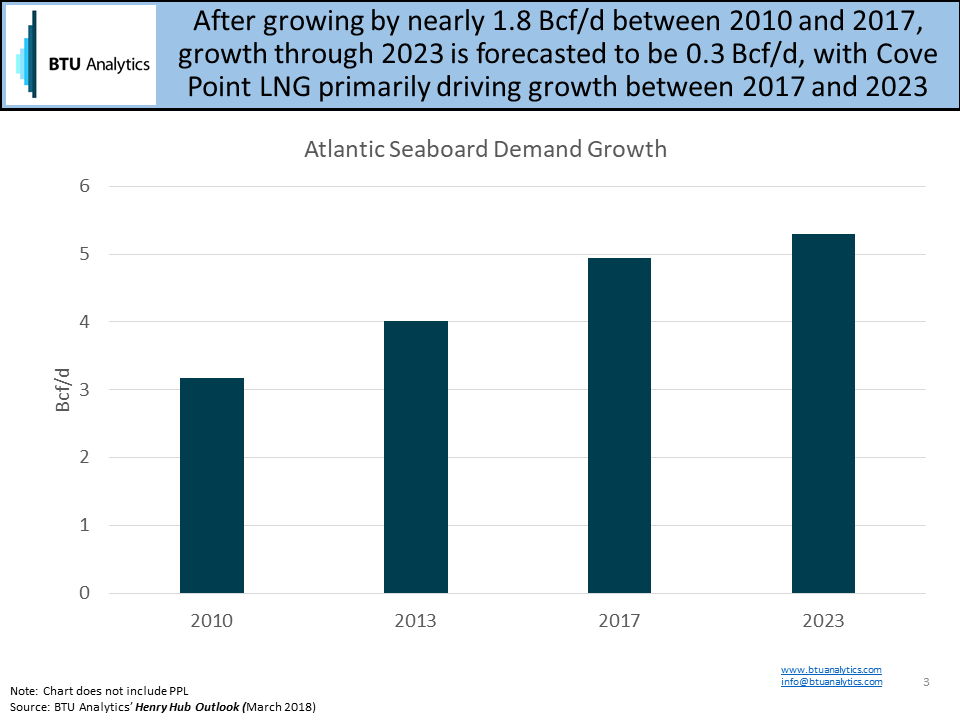

The Transco dynamics are important for the MVP expansion as shippers would be competing with Northeastern Pennsylvania gas from Atlantic Sunrise and Penneast for regional market share, but the MVP expansion project will likely be subscribed by utilities rather than producers. The rationale for the project is likely rooted in supply reliability as the region’s historical demand growth hasn’t been matched with large scale infrastructure. Atlantic Seaboard demand has grown nearly 1.8 Bcf/d over the last 7 years, but over the next 5.5 years, BTU Analytics is forecasting only a net of 0.3 Bcf/d of growth, most of which is attributable to Dominion’s Cove Point LNG facility offsetting efficiency gains in other sectors.

![]()

With Atlantic Seaboard residential, commercial, and power demand growth being flat or in decline, MVPSG makes sense in terms of adding reliability for existing demand beyond Transco and to support additional power demand gains in the longer term should nuclear plants continue to face challenges. Atlantic Coast Pipeline (ACP) is also backed by utilities in North Carolina and Virginia, and while these projects tout accessing cheap Marcellus and Utica gas, BTU Analytics expects that the end of 2019 will cement a new phase for higher Southwest Appalachia gas prices. Find out more about how MVP, ACP, Atlantic Sunrise, and other projects will impact prices with a subscription to the Northeast Gas Outlook, or check out the Henry Hub Outlook for more on US gas market supply and demand dynamics.