My 8-year old son asked me the other day while we were cooking dinner where our natural gas comes from. My short answer was that it comes from oil and gas wells in Colorado and Wyoming since CIG runs right through Denver and both states produce more gas than they consume. The fact of the matter is most people don’t have any idea how to answer this question. And in some states the answer is a moving target as growing natural gas production is reshuffling North American natural gas pipeline dynamics.

It is no secret that we are a couple of innings into a massive change in the North American natural gas industry. Starting in late August was a case in point when the William’s Transco pipeline corridor, which runs from Texas to New York City with a leg up into Pennsylvania, had 3 pipeline expansion projects announced in the same week representing over 4 Bcf/d of capacity to take Marcellus and Utica production from the Northeast to serve markets in the mid-Atlantic and Southeast markets. For those not familiar, the Transco pipeline has moved natural gas from Texas and Louisiana to the Northeast demand markets for decades and these projects would reverse that flow pattern. In addition to the Transco corridor, there are dozens of pipeline expansions being proposed to provide Marcullus/Utica producers with take-away capacity in pipeline corridors to New England, Canada, the Midwest and the Southeast/Gulf.

![]()

In order to understand the magnitude of changes I decided to look at EIA supply/demand data for January-June 2014 and then use BTU Analytics projections to look at how the East Coast market is going to change by 2019.

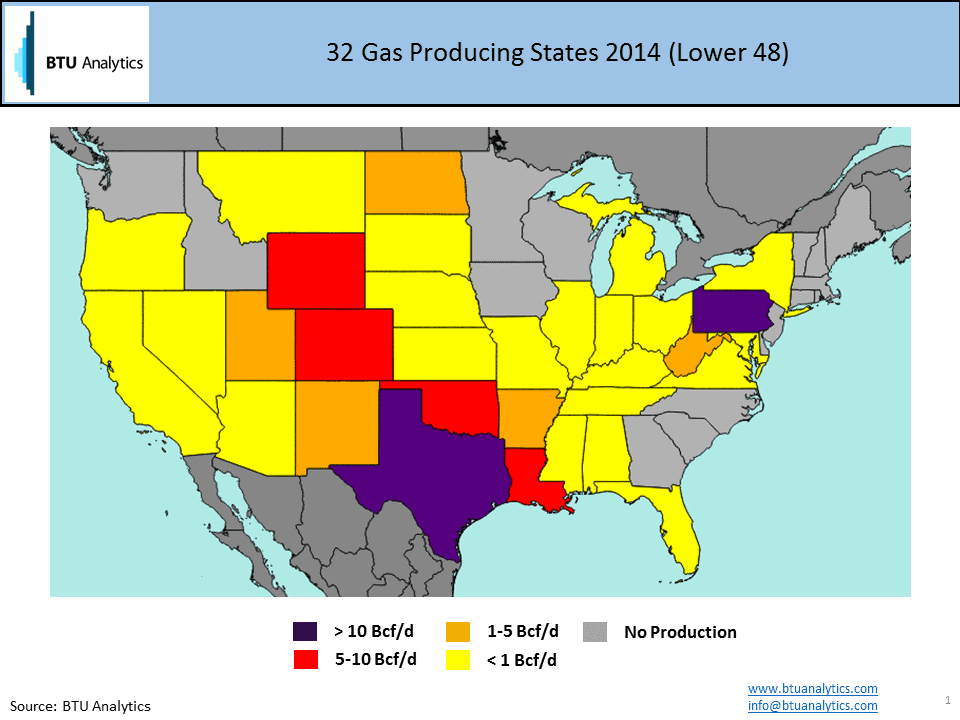

To start, it is worthwhile to take a look at which states produce gas. As the map shows below, in the lower 48, 32 states produce gas but there is a broad distribution of production levels – see map below where colors show different production levels by state. Marketed production from the lower 48 for the first half of 2014 was 74 Bcf/d. In terms of state production, the big dogs are Texas at 21 Bcf/d, Pennsylvania at 11 Bcf/d, Louisiana at 9 Bcf/d, Colorado at 6 Bcf/d and Oklahoma at 6 Bcf/d. Note, Pennsylvania was not even in the top 10 producing states in 2008 (pre-Marcellus).

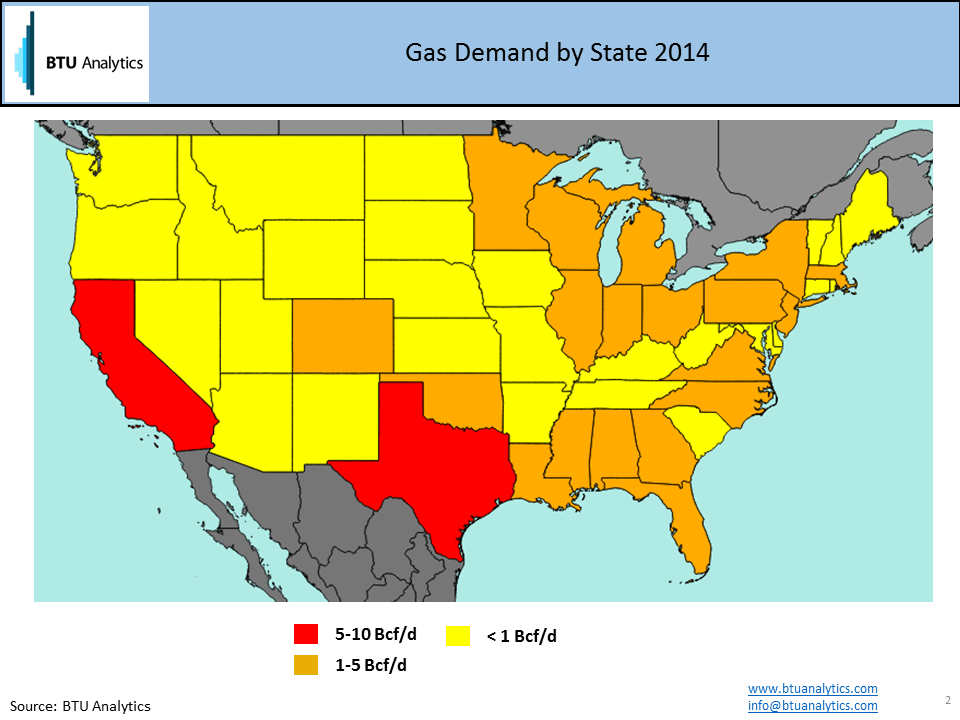

If we then look at natural gas demand we see all lower 48 states consume natural gas but again with a broad distribution depending on population, industry, etc. (see map below). The top five demand states by order are Texas at 9.5 Bcf/d, California at 6.1 Bcf/d, New York at 4.2 Bcf/d Louisiana at 3.7 Bcf/d and Illinois at 3.5 Bcf/d.

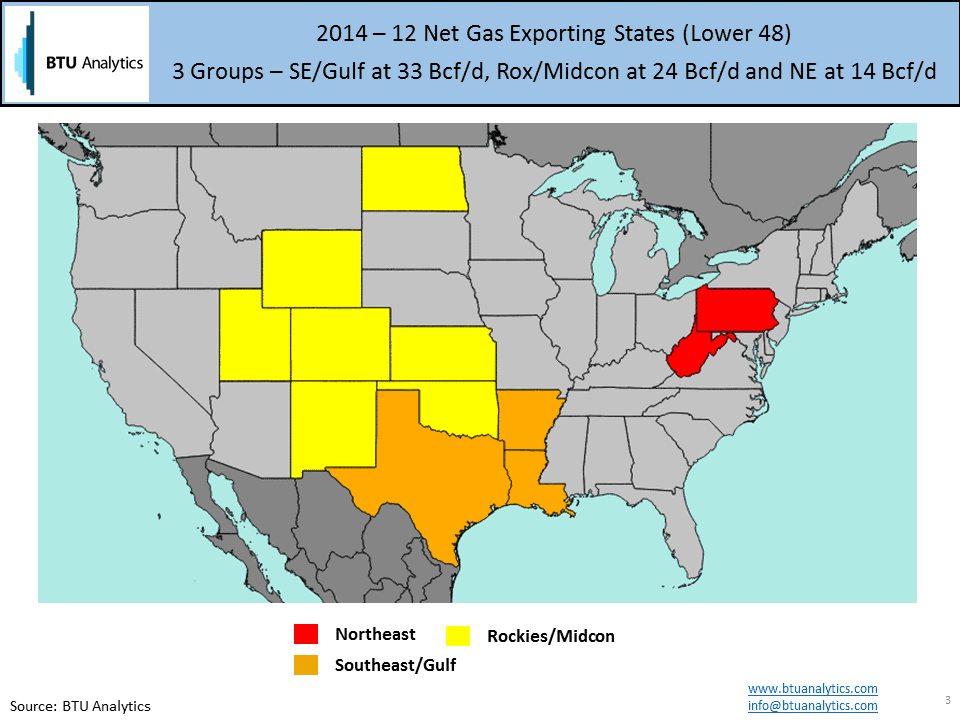

To narrow this down further, I wanted to look at net gas exporting states, where production is greater than that states demand. In 2014, there are 12 net natural gas exporting states which you can see below. I broke the 12 states into three producing groups which are Southeast/Gulf which produces 33 Bcf/d in total, the Rockies/Midcon at 24 Bcf/d and the Northeast at 14 Bcf/d. See map below.

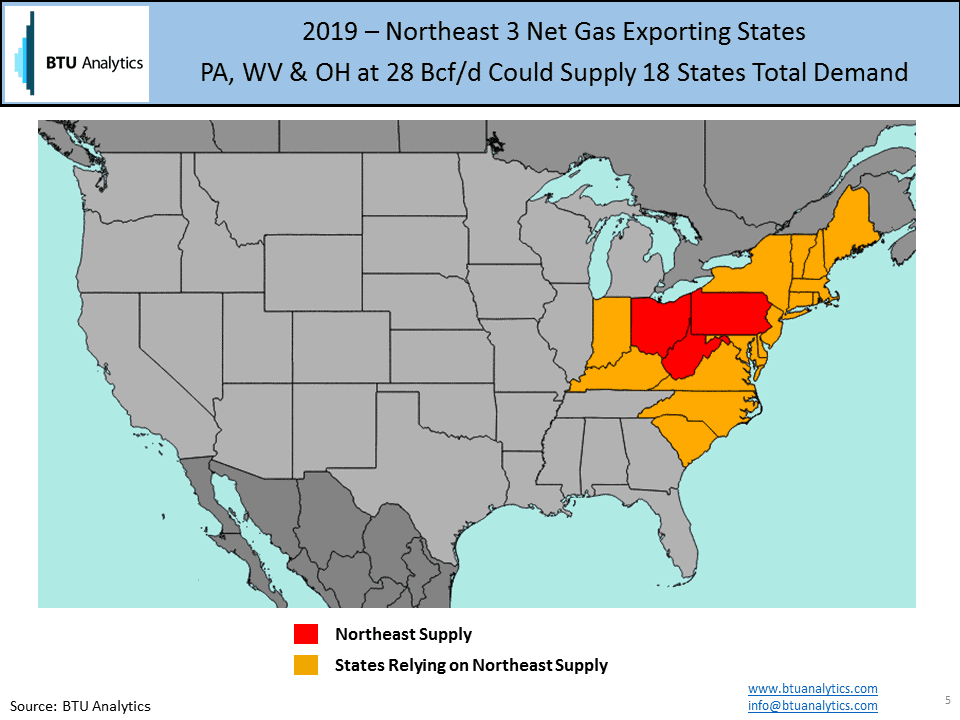

Using the BTU Analytics production model, I then used our 2019 production numbers for these states and extrapolated EIA 2008-2014 demand growth out to 2019. There are still 12 net natural gas exporting states in 2019, however we dropped Kansas due to production declines and added Ohio driven by Utica shale growth. Also note that the total production numbers change with the Southeast/Gulf jumping to 40 Bcf/d in total, the Rockies/Midcon staying flat at 24 Bcf/d and the Northeast doubling to an impressive 28 Bcf/d driven by Marcellus and Utica shale growth. See map below.

So how is the gas market going to handle all of this production growth? Fortunately, in the Southeast there is growing industrial and power demand as well as LNG export projects to soak up this growth – our market study Battle for Henry Hub details Louisiana natural gas balances through 2020. In the Northeast however, limited demand growth means continued growth in the Marcellus and Utica has to come at the expense of pipeline flows from the Southeast/Gulf, Rockies, Midcon and Canada. With the Northeast production growing to 28 Bcf/d, it can meet the entire demand of 18 Northeast states. This is a simplification of the gas market but serves the purpose to show the magnitude of Northeast production growth. See map below.

So back to where does your gas come from – well if you live in the eastern half of the country, the answer will soon be for many of you gas sourced from Pennsylvania, Ohio and West Virginia. For Virginia, North Carolina and South Carolina in particular, this is a huge change as these states have relied on decades worth of Southeast/Gulf supply flowing north via the Transco pipeline. Northeast production growth combined with pipeline expansion/reversal projects will soon mean Virginia, North Carolina and South Carolina will start seeing more and more Marcellus and Utica sourced gas from the Northeast.

For a deeper look at US natural gas pipeline flow dynamics, request an overview of our recent market analysis – The Battle for Henry Hub.