In the business of energy market fundamental analysis, you are always tasked with telling people what is going to happen next and why. Inevitably, sometimes you are right and sometimes you are wrong. When you are right for the right reasons one feels vindicated. When you are wrong, it is unpleasant but you study up on what you missed and why and keep moving. At BTU Analytics we are always reviewing our previous and current price forecasts, production outlooks for natural gas and oil, and pipeline capacity constraint predictions to see how our forecasts performed against reality. Across all of the consulting and analytical reports that BTU Analytics conducts, one of the most comprehensive and broad reaching pieces of analysis under taken each year is our annual What Lies Ahead Conference. In today’s commentary, we will look at our best energy market predictions from our February 2017 What Lies Ahead Conference as we prepare for the What Lies Ahead 2018 conference.

At the What Lies Ahead 2017 conference, we covered several major topics and themes such as:

- Is North American oil driving the bus or along for the ride with OPEC?

- Do Permian breakevens matter in a capital constrained market?

- Marcellus pipes on time or pipeline purgatory?

- Is Henry Hub starved for gas or a wash with supply?

- What opportunities exist for investment in North American energy markets?

So what calls did BTU Analytics make in February 2017 that were spot on?

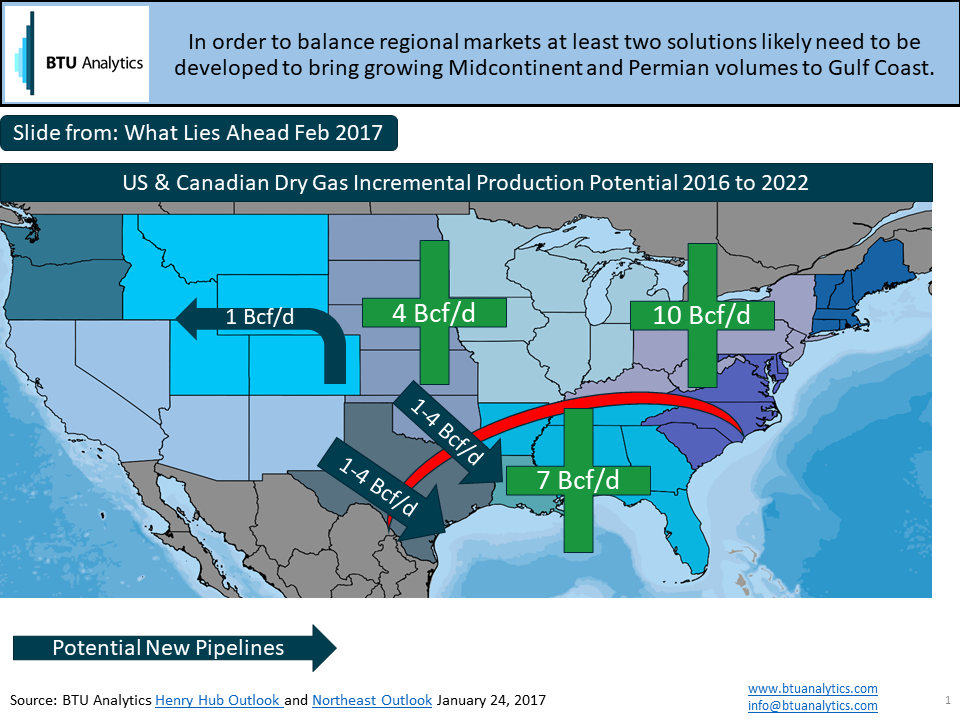

Above is a slide that highlights BTU Analytics’ regional natural gas supply, demand, and pipe capacity modeling from the investment opportunities session. The slide shows where incremental additional pipeline capacity development was needed based on the models at the time. As shown, incremental projects were highlighted to the southeast out of Oklahoma, eastbound out of the Permian and north and west out of the DJ. These very same dynamics have also contributed to weak supply area natural gas basis across the Permian, Mid-continent, and Rockies in the back half of 2017 which was predicted at the conference in February 2017.

The following pipeline project announcements were made after the conference validating themes in this slide and from the conference:

- Cheniere announces key commercial agreements for Midship Pipeline

- Enable Midstream to build CaSE pipeline project out of Oklahoma

- Kinder Morgan Gulf Coast Express gas pipeline out of the Permian

- Tallgrass Energy announces Cheyenne Connector Project

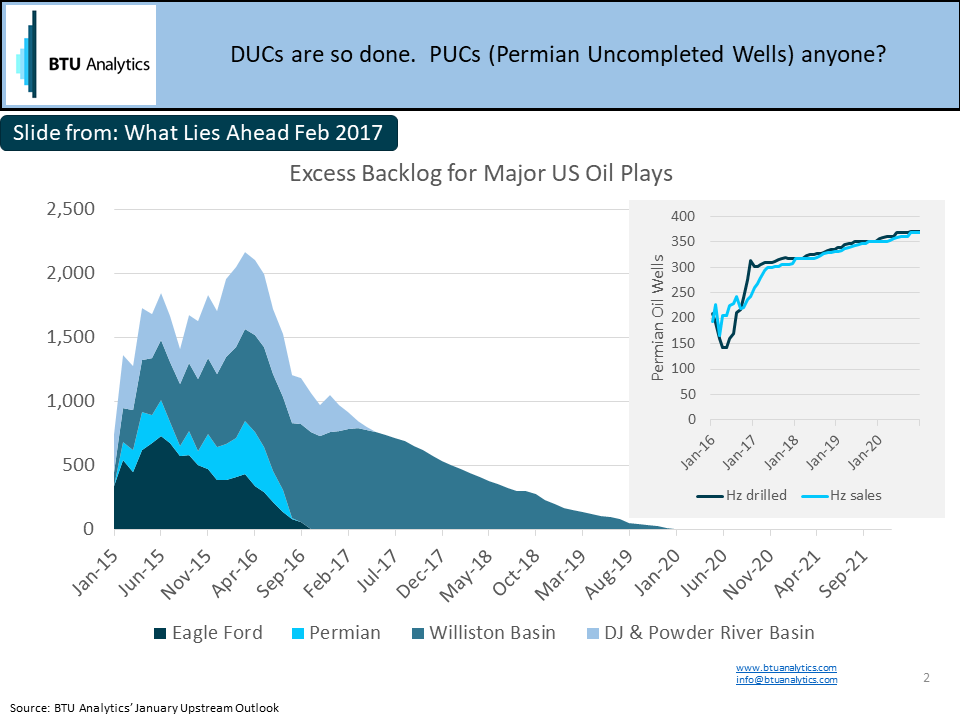

As shown above, we also highlighted our concerns, that had been previously discussed in our Upstream Outlook subscription, about the pace of development in the Permian and the ability for completions crews to keep pace. We spoke to the end of DUCs but raised concerns about PUCs (Permian Uncompleted Wells) and showed BTU Analytics’ Upstream Outlook forecast of horizontal wells drilled out-pacing horizontal wells to sales (accumulation of DUCs or in this case PUCS). PUCs came to fruition in 2017 and BTU covered this topic in July 2017 in our energy market commentary: Permian DUCs on the Rise.

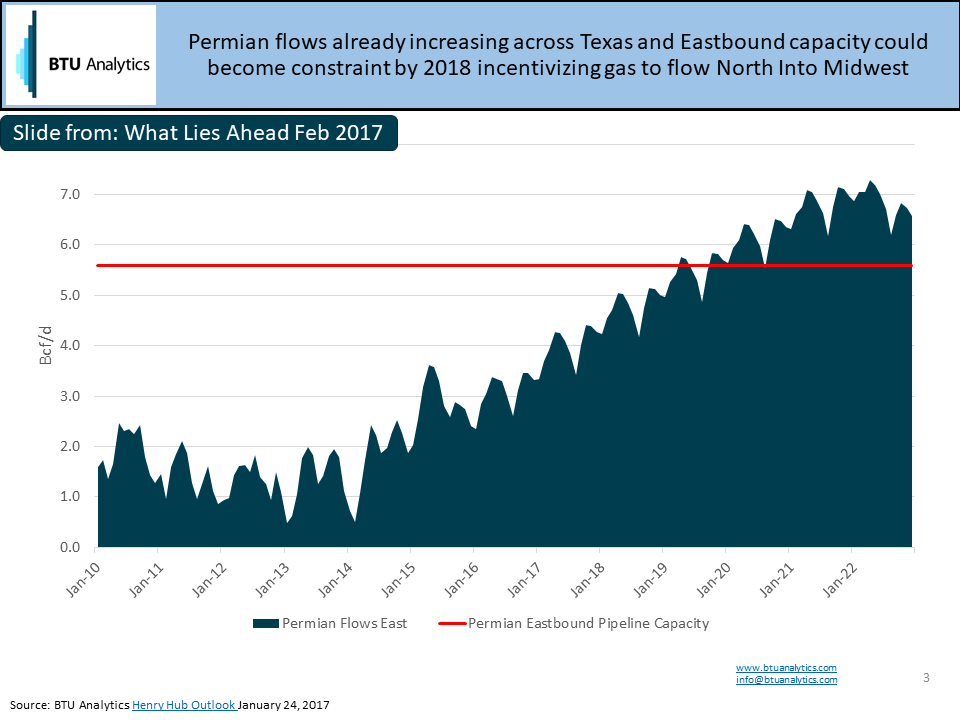

Another topic covered during the conference highlighted our concerns that natural gas pipeline capacity out of the Permian could limit oil production growth. The slide above, from the 2017 conference, highlights BTU Analytics’ estimate of gas flowing east across intrastate pipelines in Texas becoming congested leading to basis pressure in the West and potentially production shut-ins if new pipeline capacity was not developed by 2019. The Wall Street Journal covered this topic extensively in November 2017.

The agenda for What Lies Ahead 2018 is equally as comprehensive and will provide ample opportunities for attendees to learn about BTU Analytics’ outlook for 2018 and beyond – click here to view agenda or register for the What Lies Ahead 2018 on February 22, 2018, in downtown Houston.

Also, RW Baird is hosting a conference call (Register here) on Wednesday, November 29 featuring BTU Analytics’ Senior Energy Analyst Erika Coombs who will be covering our recent NGL study – “Hidden in Plain Sight – How the industry’s models broke and obscured true ethane supply“.