Natural gas prices at the AECO price point in Western Canada remained on a roller coaster in April. Outright prices at AECO spiked to $4.30/MMBtu at the beginning of March then plummeted $0.19/MMBtu on April 5th. Then price began to recover, reaching $1.34/MMBtu on the 17th, but then plunged back below $0.50/MMBtu. Ongoing maintenance through the summer on Westcoast Pipeline, which suffered an explosion in October, GTN, and the TransCanada Mainline indicate prices will likely remain depressed. After nearly three years of AECO pricing averaging below $2.00/MMBtu, drilling activity is showing signs that enough is enough. Could this slowdown finally help boost AECO prices?

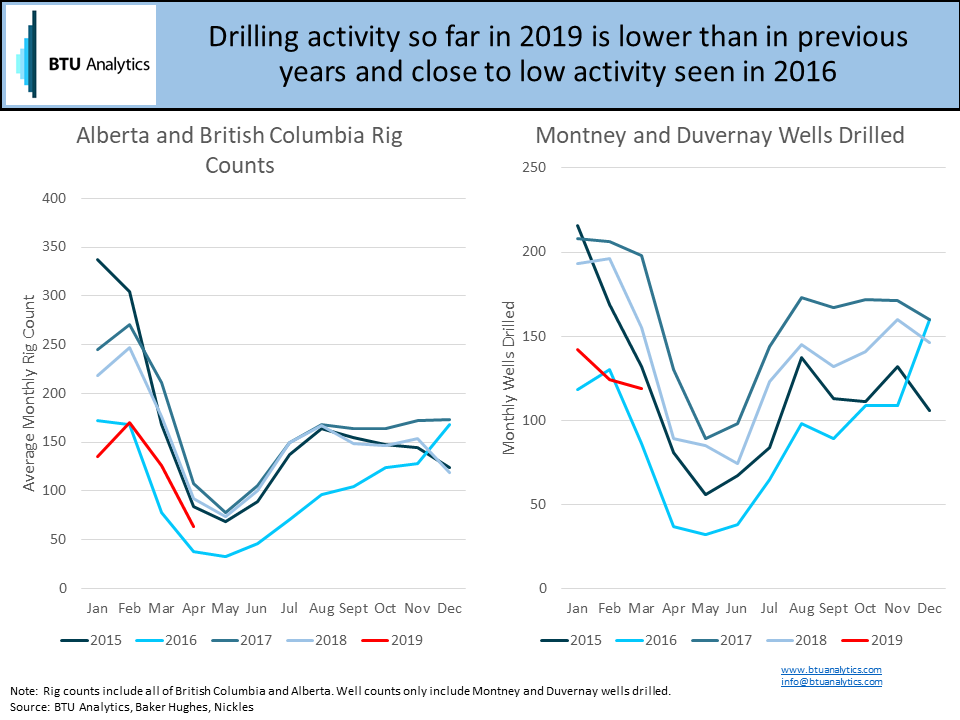

It’s the end of April, and spring break-up is in full swing in Western Canada. Spring break-up begins when frost begins to melt and makes the ground soft and muddy. Road bans are put in place for heavy machinery, preventing rigs from moving and causing activity to fall. So far in 2019, the rig count in Alberta and British Columbia has dropped from a 2019 high of 183 rigs at the end of January to 60 rigs last week, according to Baker Hughes data. However, even before spring break-up, activity in Western Canada had dropped well below prior year levels. Across Alberta and British Columbia, rig counts in January 2019 were 38% below January 2018 levels and 45% below January 2017 levels. The Montney and Duvernay account for approximately 60% of the drilling activity in Alberta and British Columbia. In the Montney and Duvernay, the number of wells drilled in January 2019 was 26% below 2018 levels and 32% below January 2017 levels. Drilling declines in the Montney and Duvernay have been less severe than the drop in rig counts due to gains in drilling times.

Spring break-up typically ends around June when the road bans are lifted, and rigs and completion crews can move around again. As a result, production typically declines from April through June. The increased slowdown and potentially steeper drops in production could support AECO prices by adding less supply to the NOVA system during the summer of 2019, particularly if producers defer summer completion operations in response to weak prices.

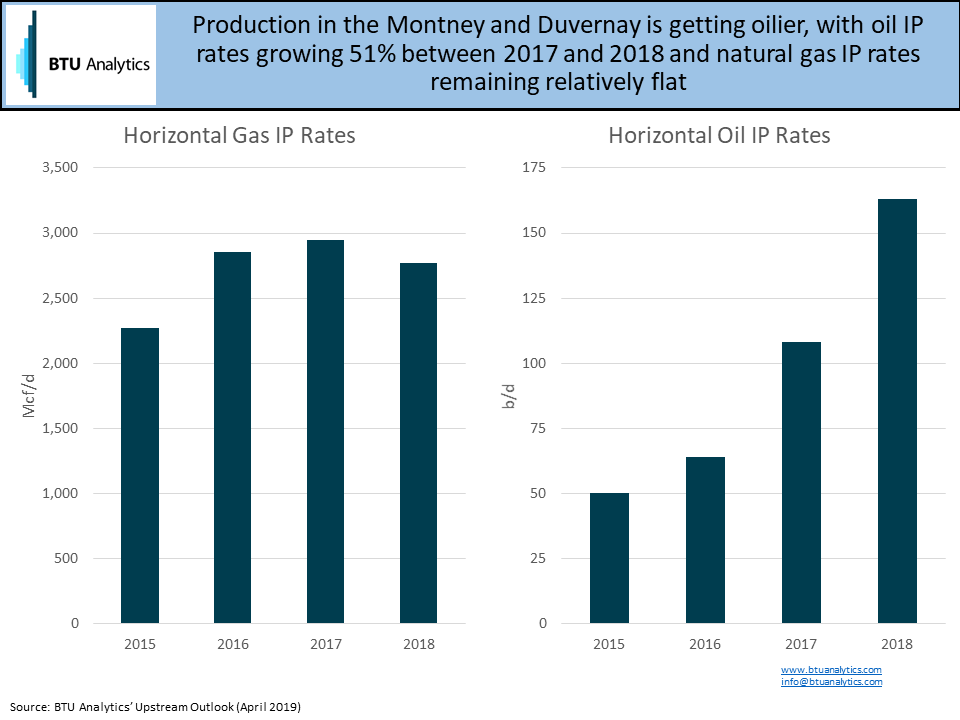

Like many plays in the US, operators in the Montney and Duvernay continue shifting activity to more liquids rich acreage. However, in the case of the Montney and Duvernay, the shift has yet to significantly reduce gas productivity. The charts below show average oil and gas IP rates in the Montney and Duvernay since 2015. Initial oil production rates grew 51% from 2017 to 2018. Over the same time frame, natural gas initial production rates dropped by 6%.

While the decline is relatively modest, new wells should produce lower natural gas volumes compared to previous years. With weak natural gas prices, operators should continue to focus remaining activity on the oiliest acreage indicating further drops in productivity may be ahead. This, along with the decrease in drilling activity, should help decrease natural gas volumes entering the constrained NOVA system in 2019.

However, until the ongoing maintenance issues are resolved across the three main arteries out of Western Canada and expansions enter service in the fall on GTN and the TransCanada Mainline, AECO prices may continue to remain under pressure despite producer scale backs. To stay up to date on the latest outlook on pricing and flow dynamics in Western Canada, request a sample of BTU Analytics’ Gas Basis Outlook, which includes our AECO forecast as well as forecasts for other price points across North America. For more information on activity and production analysis for the Montney, Duvernay, and other US and Canadian plays request a sample of our Upstream Outlook report.