While production curtailments in the oil sands get the headlines, the Canadian natural gas market is also in flux amid the economic disruption wrought by COVID-19. Today’s energy market insights will compare recent Canadian market dynamics to 2019 and briefly consider implications to demand, production, exports, and storage.

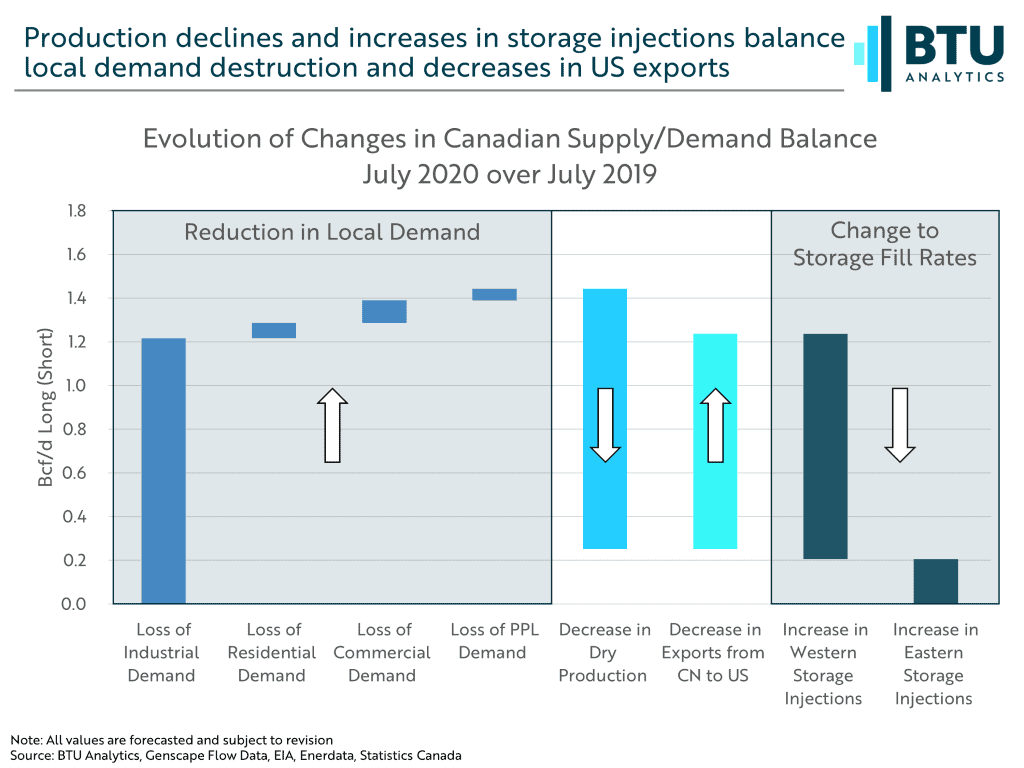

The chart below examines the expected changes to Canadian supply and demand from July 2019 to July 2020. An increase for any fundamental indicates the overall balance is being pushed long compared to the balance from the prior year, and a decrease indicates the balance is being pushed short. Despite all the factors in play at any given moment, any market must ultimately balance, and the Canadian gas market is no exception.

Curtailments of oil sands production combined with lockdowns have resulted in substantial reduction to natural gas demand in Alberta. Oil sands require large quantities of steam to facilitate the recovery of bitumen. The steam is typically generated by natural gas-fired power plants located on-site. When oil production from these sites is reduced, the call on natural gas for steam production is also reduced, resulting in a drop Canadian industrial demand. BTU Analytics estimates a loss of up to 1.2 Bcf/d of total Canadian power and industrial demand for July 2020, a significant portion of which can be attributed to oil sands demand destruction. In addition to the drop in industrial demand, residential and commercial demand is also expected to drop by about 0.3 Bcf/d . The total drop in demand for Canada is expected to average about 1.5 Bcf/d compared to July 2019.

On the upstream side, producers have already started to respond, with a drastic reduction in drilling activity in Alberta and British Columbia. Rig counts across these provinces are down 80% year-over-year, from an average of 74 in June 2019, to only 14 in June 2020. The drop in activity this summer will compound the fall in activity over the winter of 2019-2020. As a result, dry gas production is expected to fall nearly 1.2 Bcf/d from July 2019 to July 2020. This drop in production has partially offset the loss of demand in Canada leaving the market long about 0.3 Bcf/d relative to July 2019.

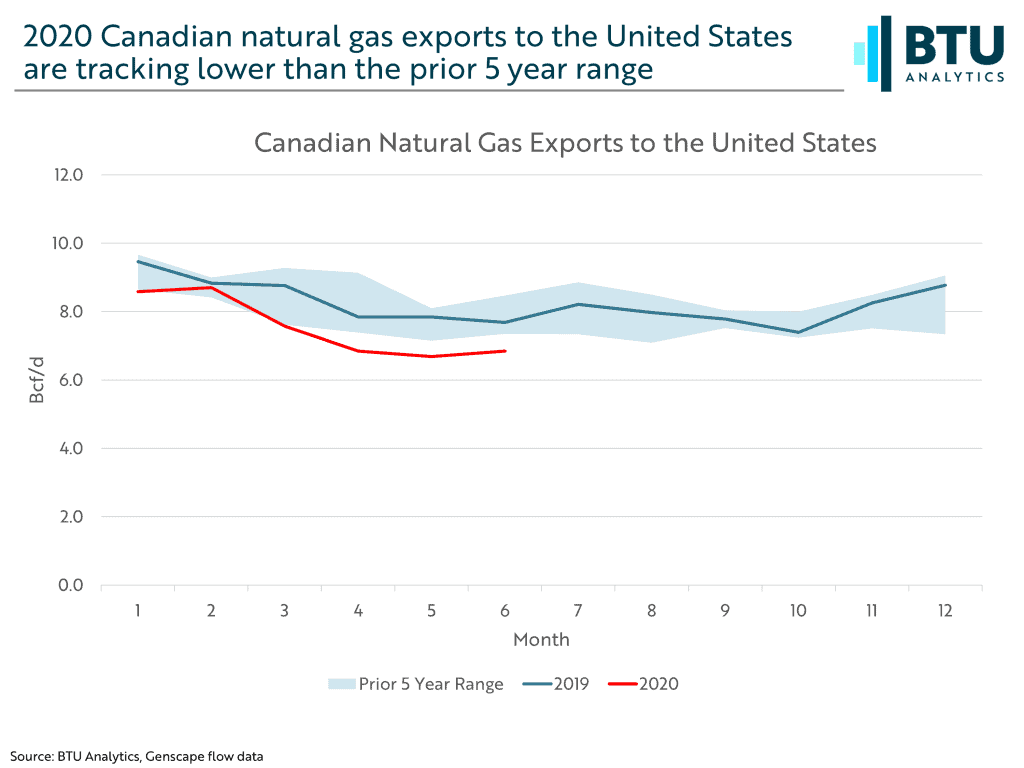

Unfortunately, the drop in domestic demand has not been the only loss in demand for Canadian production. Canadian exports to the US, highlighted in the chart below, have also been in decline. Canadian exports year to date are down 0.88 Bcf/d and expected to be about 1.0 Bcf/d below 2019 levels in July.

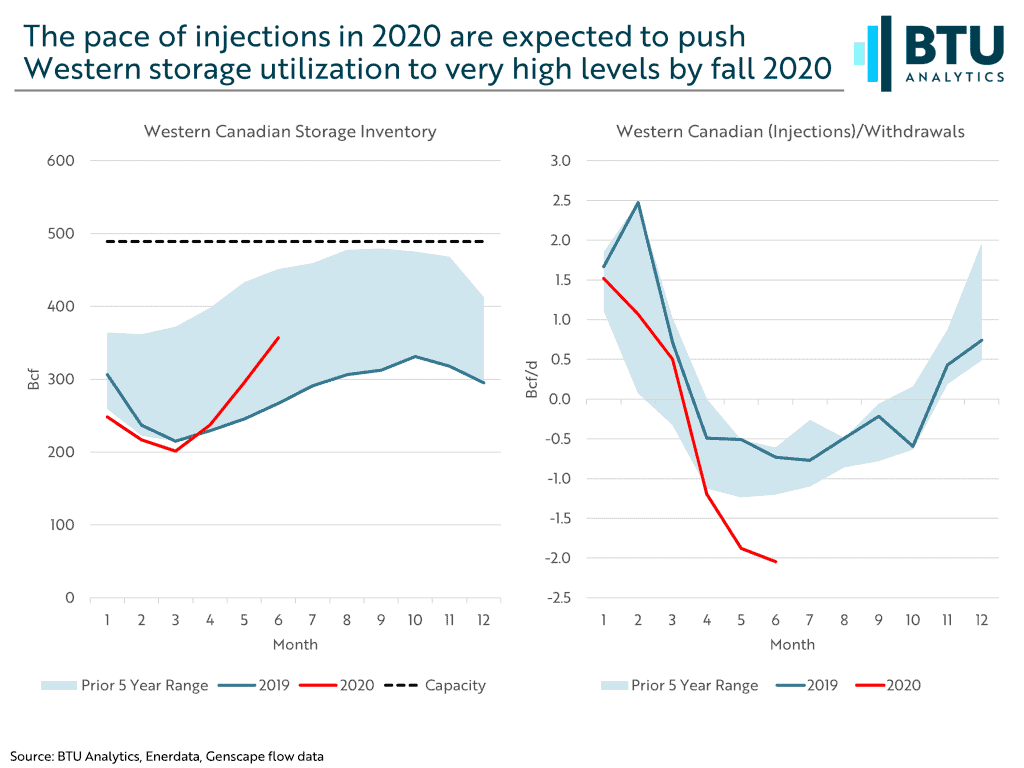

Fortunately for producers, new rules on TC Energy’s NOVA system enacted in late 2019 have increased system flexibility and improved access to storage. Enactment of TC Energy’s Temporary Service Protocol has helped reduce price volatility at AECO through the winter of 2019-2020 and basis continues to tighten into the summer of 2020, averaging only ($0.17) in June despite the loss in domestic and export demand. Record spring and summer injections have helped to reduce the compounded impacts of demand losses on basis prices, however the rapid pace of storage injections year-to-date could result in storage inventory reaching near maximum capacity by the end of the summer. The charts below show Western Canadian storage inventories and the current pace of injections and withdrawals compared to their prior 5 year ranges.

The Canadian gas market, much like the US market, remains on the precarious edge of running out of storage inventory by the end of the summer. All may not be lost though; production remains in decline this summer and Canadian oil sands demand should be rebounding as oil prices stabilize near $40/bbl. To gain a deeper understanding of BTU Analytics’ expectations for North American supply and demand balances, request a sample of our Henry Hub Outlook.