After a relatively calm beginning to the Winter ‘21/’22 heating season, sustained bitterly cold temperatures in New England led to prolonged blowout pricing conditions at Boston’s Algonquin City Gate throughout late 2021 and early 2022. Between December 18, 2021, and February 28, 2022, Algonquin CG saw an average outright price of $16.30/MMBtu and daily prices that surpassed $20/MMBtu 35 times. Today’s Energy Market Insight will look at the drivers of pricing volatility in the New England market.

This protracted period of elevated pricing resulted in large part from continued supply constraints caused by ongoing pipeline congestion issues. Simply put, all existing winter pipeline import capability into New England is now utilized at or near capacity. Notably, flows from Appalachia into New England on the Algonquin Pipeline averaged more than 1.8 Bcf/d in December 2021 through February 2022 – with resulting average utilizations of more than 99% of estimated capacity. However, another key contributor to the sustained blowout pricing is New England’s continued reliance on LNG imports to meet winter demands. Sharp increases in global LNG prices have made these resources increasingly difficult to obtain, leading to diminished supplies in Winter ‘21/’22 and likely foreshadowing ongoing problems in subsequent winters.

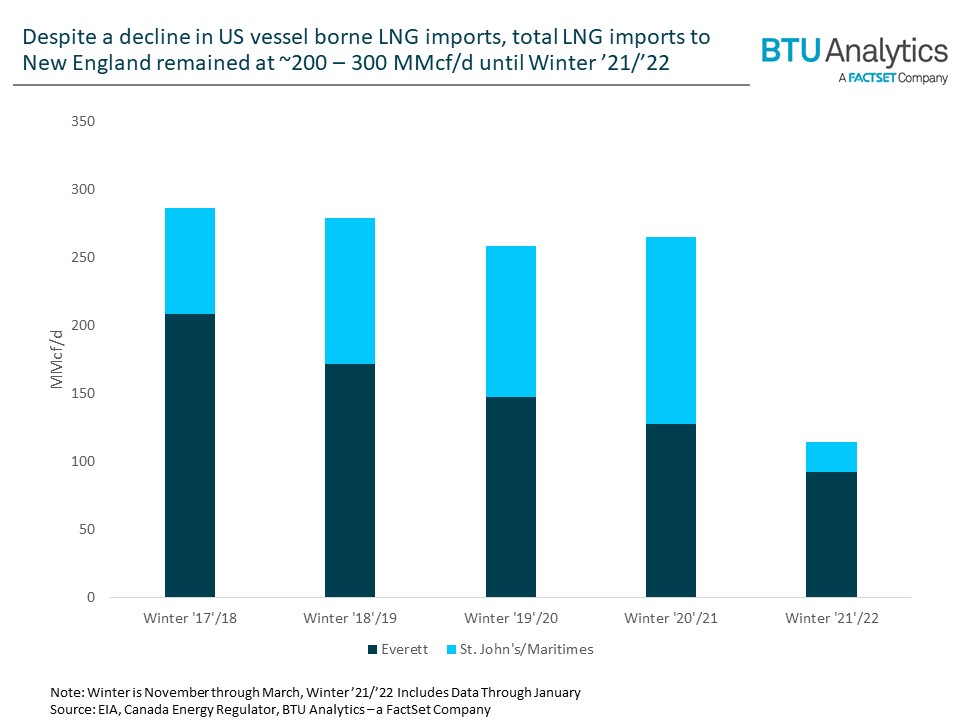

Regional LNG imports dropped significantly in Winter ‘21/’22 as Global LNG prices surged

After the suspension of operations at the Neptune Deep Water Port in 2013 and through 2021, vessel borne imports of LNG to New England were processed almost exclusively through the LNG facility located in Everett, MA, and were sourced almost exclusively from Trinidad and Tobago. The region can also import LNG received in Canada at the St. John’s, New Brunswick facility (formerly Canaport) via the Maritimes and New England pipeline. These imports are limited by the capacity of the pipeline – estimated at ~0.6 Bcf/d. While the Northeast Gateway facility also resumed operations in January 2022, the total US vessel borne volume – now split between NE Gateway and Everett – was unchanged from the amount imported in January 2021, 6.4 Bcf in both cases. While this is only one data point, it suggests that the LNG received at NE Gateway may be at the expense of Everett volumes rather than representing the beginning of increased imports to the region.

While vessel borne winter deliveries to the US have decreased substantially from 2017 – 2020, LNG deliveries to Canaport/St. John’s increased over the same period. With most of the gas delivered to the St. John’s facility ultimately moved to New England via the Maritimes Pipeline, the net result is that overall winter LNG deliveries to the region remained relatively steady at 200 MMcf/d – 300 MMcf/d prior to the Winter ‘21/’22.

However, Winter ‘21/’22 saw significantly reduced import volumes at both St. John’s and Everett. Further, the timing in this drop corresponds almost exactly with the surge in global LNG prices.

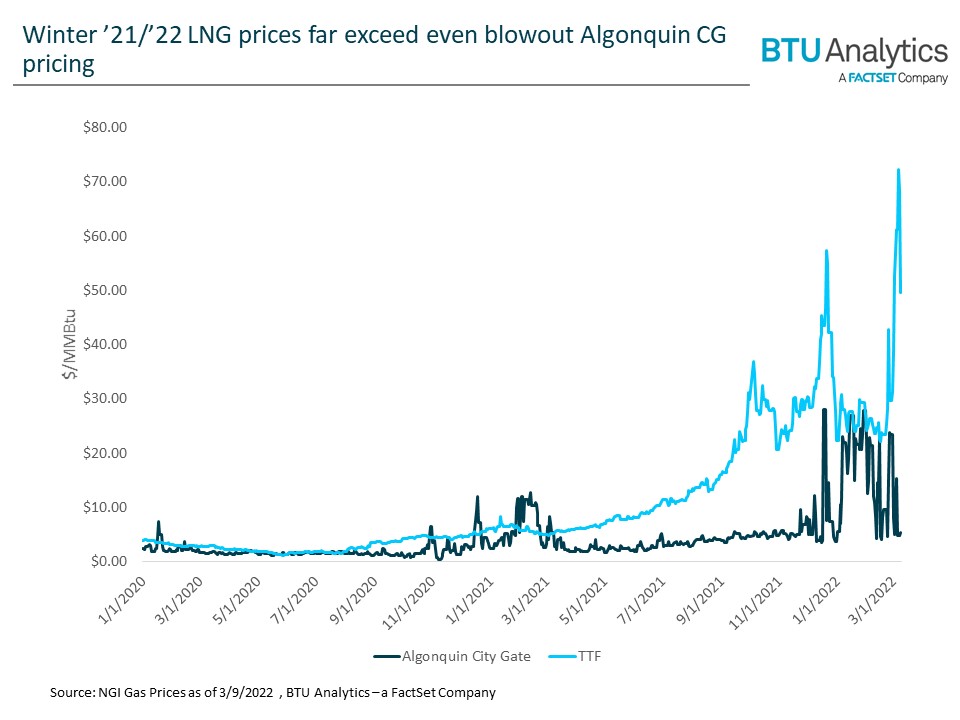

European natural gas prices, as gauged by the Netherlands’ TTF Index, are compared with Algonquin CG prices in the chart below.

Notably, European natural gas prices began to increase significantly in Summer ’21 – making the process of obtaining LNG volumes for Winter ‘21/’22 difficult both in New England and further afield. Further, during Winter ‘21/’22 LNG prices far exceeded even the highest Algonquin CG pricing – ensuring that LNG remained far out of reach as a cost-effective replacement resource.

Conclusion

With all pipeline import capacity fully utilized, traditional LNG supplies at historically low levels, and periodic spikes in demand due to long periods of extremely cold weather, Winter ‘21/’22 in New England saw a strong confluence of factors resulting in extended periods of blowout pricing. Further, this set of conditions seems likely to reappear in subsequent winters for several reasons. First, due to regulatory conditions in the region, additional pipeline import infrastructure is unlikely to be added, meaning that capacity will likely remain capped at current levels. Further, the geopolitical and logistical issues that led to the recent sharp increase in global LNG pricing seem unlikely to be resolved in the foreseeable future, and buyers in New England will have to compete for the same LNG cargoes as customers in Asia and Europe – making supplies both difficult to obtain and expensive. Finally, winter demand levels in the region are expected to remain at or near current levels for at least the next several years and decreases in the levels of gas required to serve demand are unlikely. Given the ongoing regional issues with both supply and demand, it seems likely that the periods of blowout pricing seen in New England this winter will become a regular occurrence.