When it comes to long-term forecasting, there are a multitude of questions that need to be answered. Previously, we have touched on the impacts of nuclear power plant retirements on natural gas power demand (something to be kept in mind when interpreting recent guidance from the Trump Administration) and we recently laid out the inventory and reserve depletion ramifications to long-term natural gas pricing. Today I want to address the question: with overall demand expected to grow, mainly due to increasing exports, from where will all the gas be sourced?

If you want more details than what I can cover in 500 words today, join us for our complimentary webinar next Thursday where we will discuss our views surrounding long-term supply, demand, and pricing dynamics in the natural gas market.

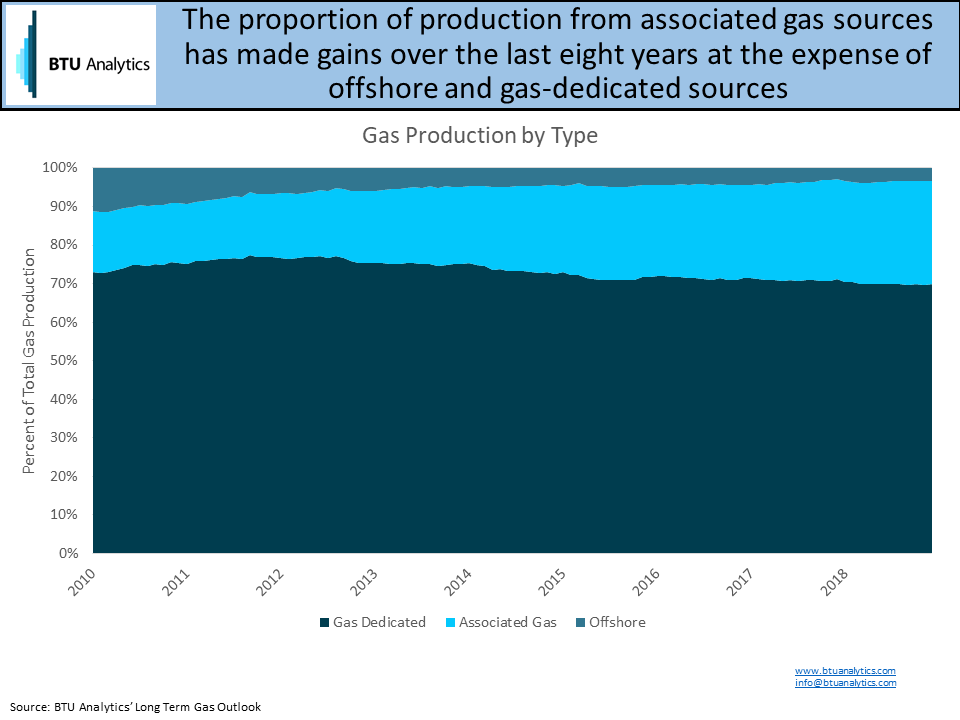

The first distinction we can make is between gas sourced from gas-dedicated plays and associated gas plays. Associated gas is driven by liquids and prices, while gas from gas-dedicated plays is driven by gas prices. Since liquids economics are typically more attractive than gas economics, gas from gas-dedicated plays, and natural gas pricing in general, are at the mercy of movements in liquids pricing. Put another way, the more associated gas in the market, the less gas needed from gas-dedicated plays. The less gas needed from gas-dedicated plays, the lower gas prices must be to balance the market. We can take that same logic and flip it, leading to the conclusion that less associated gas results in higher gas prices. I am employing the “all else being equal” condition here, but the relationship generally holds and is a major driver of pricing today and well into the future.

The graphic above shows that the proportion of gas coming from associated gas plays has steadily ticked up over the past few years from near 16% in 2010 to over 26% by 2018.

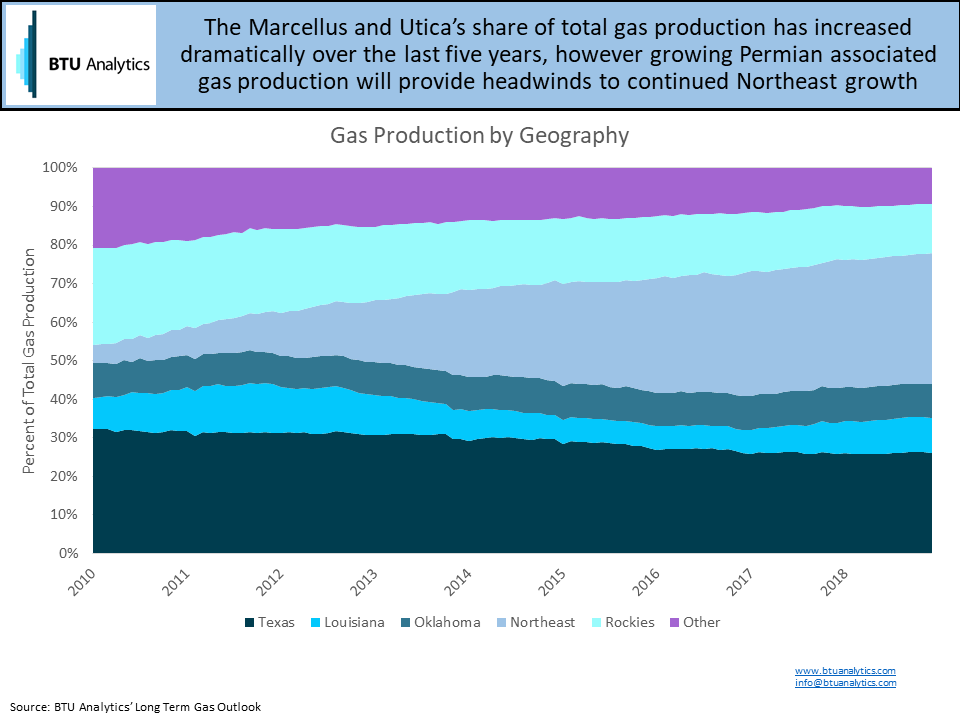

A second way we can break down where gas will come from is geographical. For our clients, this is an important distinction. Given limited capital, where can you invest to get the best bang for your buck? Our newest product dives into the just that. Our Long Term Gas Outlook shows how economics and pricing will dictate which plays will be advantaged over time in the long-run. The graphic below is a historical take on the breakdown by geography, which shows the Northeast’s recent rise in prominence.

It’s no surprise that going forward the Permian will play an increasingly larger role, but how much infrastructure investment will be needed for the play to see its potential? And how will the Permian’s growth continue to impact other plays around the US, such as the Marcellus and Utica? For details on this and a more in-depth conversation on the breakdown of supply, join in on our free webinar next week. We’ll have live Q&A and every participant will get a recording of the presentation (BTU clients will receive a copy of the presentation also) and a free sample of our latest report, the Long Term Gas Outlook.