The Asian LNG market has been a hot topic in recent months as a cold start to winter left many countries scrambling to secure additional LNG supplies leading to substantial increases in LNG pricing. Although JKM spot prices approaching $40/MMBtu stole much of the attention, Europe was also feeling the effects of a tight winter LNG market. Decreased European LNG imports have led to a significant pull-on gas storage inventories, leaving Europe primed to absorb additional LNG cargoes this summer. However, depending on the timing of the eventual completion of Nord Stream 2, US LNG upside could be limited due to Germany’s outsized influence on Europe’s diminished gas storage.

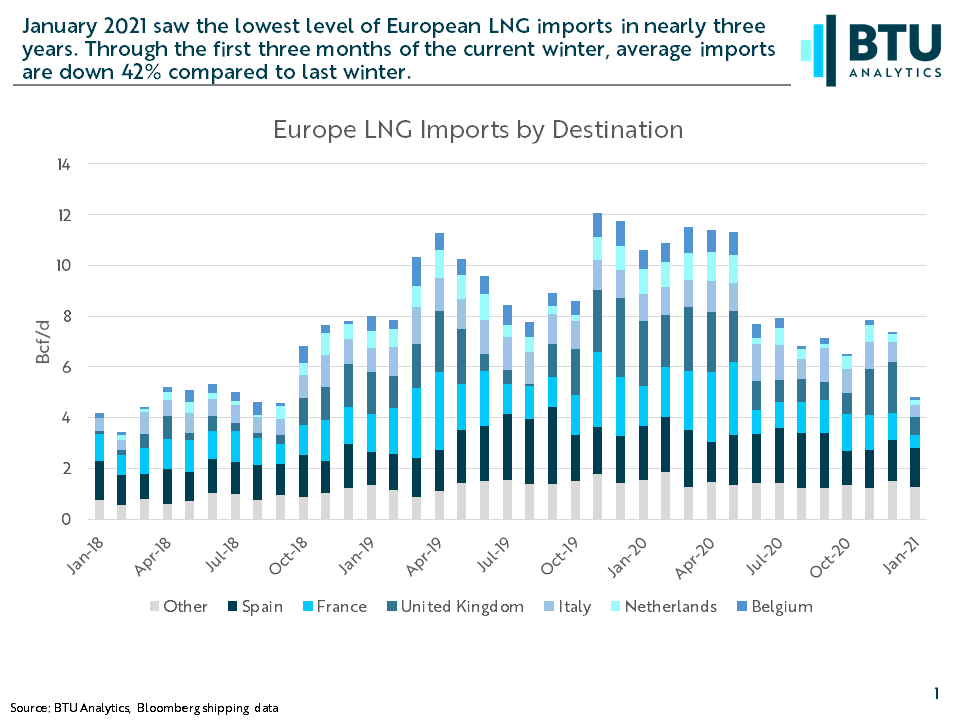

Despite having a relatively cold winter compared to last year, European LNG imports are down 42% through the first three months of winter. The fall has been capped by a January that saw European imports fall to just 6.2 Bcf/d, the lowest level in almost three years. These declines were driven by historically strong winter pricing in Asia that diverted cargoes away from Europe. At the country level, these declines were absorbed almost entirely by Europe’s largest importers. Decreased imports from Europe’s top six importers, shown below, account for 95% of the season over season decline in LNG.

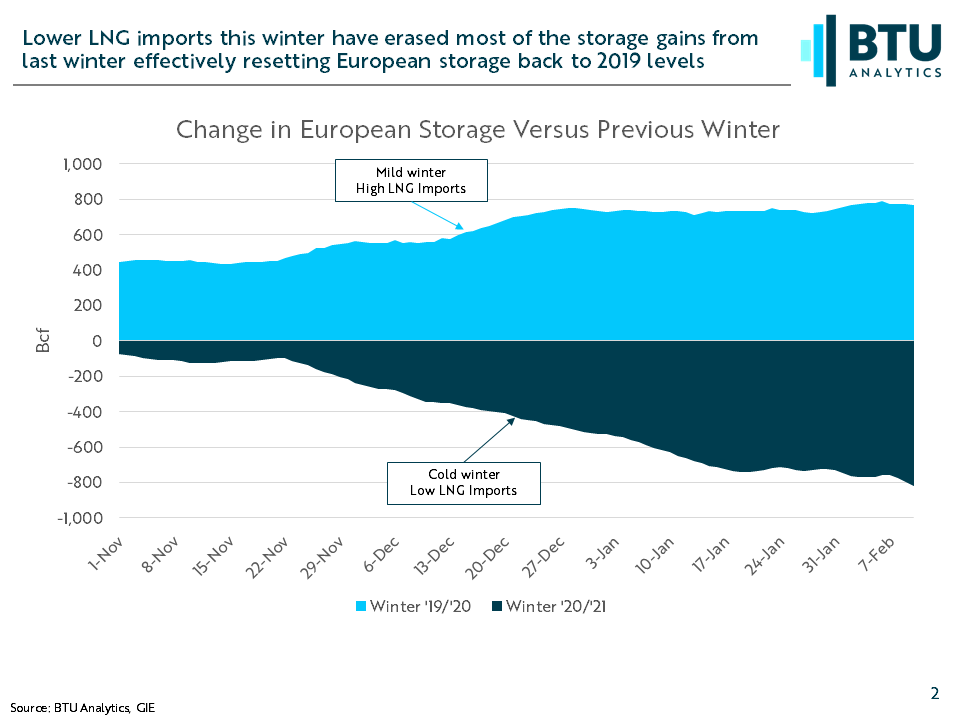

While LNG imports have fallen for most of continental Europe, the decline was driven by the high pricing in Asia, not diminished demand. As a result, this winter has seen a heavy draw on gas storage inventories. As of February 10th, total European gas storage sits 819 Bcf below the level at the same point last year. As illustrated below, the decline has effectively reversed the gains in storage from the mild winter of ‘19/’20, leaving 2021 25 Bcf below the same point in 2019.

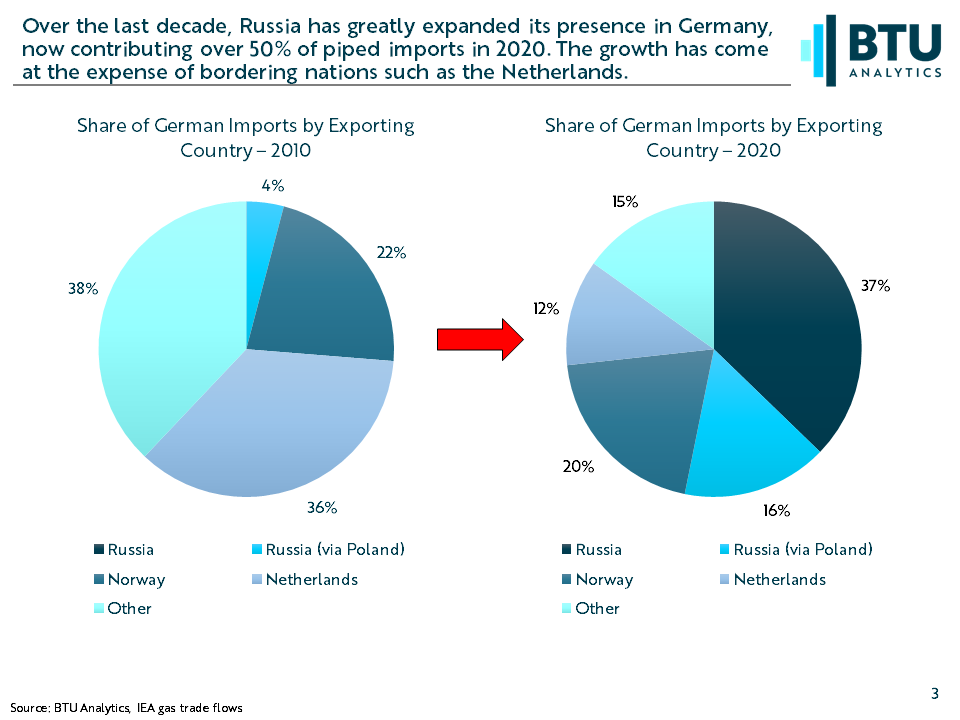

Unsurprisingly, many of the largest LNG importers in Europe have seen storage fall as winter imports have declined. France and the Netherlands have both seen storage fall over 25% year over year after seeing LNG imports fall by over 55% compared to last winter. However, the most significant fall in storage this winter has occurred in Germany. German storage currently sits 317 Bcf lower than at the same point last year, nearly a 50% decline relative to 2020. Unlike other major EU countries, Germany has no LNG imports, instead importing 95% of its natural gas via pipeline with an increasingly greater percentage coming from Russia. In 2019 and 2020, Germany’s imports from Russia have increased rapidly, mostly at the expense of the Netherlands. Russia now supplies over 50% of Germany’s piped imports via the existing Nord Stream pipeline, and the Yamal-Europe pipeline that runs through Poland.

The importance of German storage to the overall balance of Europe is a key reason why the imminent completion of Nord Stream 2 poses a significant risk to US LNG exports moving forward. Not only is Germany the entrance point for Nord Stream 2 into Europe, it also has no competition from foreign LNG. While Nord Stream 2 delays could allow for increased LNG imports this summer, the long-term impact of increased piped gas into Germany could limit upside in the future. BTU Analytics tracks US LNG exports to Europe, and the eventual impact of the startup of Nord Stream 2, in our monthly Henry Hub Outlook report. In addition, BTU Analytics recently released a client-only webinar discussing the 2021 outlook for the US gas market and the role that US LNG exports will play over the coming months.