Back in 2008, Appalachian production was only 2 Bcf/d and on a typical day the Northeast relied on inbound flows of approximately 15 Bcf/d on long-haul pipes from Canada, the Midcontinent, the Southeast and LNG. At that time, Columbia Gas (TCO) and Dominion (DTI) pipelines played an important role in the Northeast market as two intertwined pipelines that took 2 Bcf/d of Appalachian production and gas from long-haul pipes and distributed that gas to LDCs and storage operators (depending on the season) on their systems. As a result, Dominion South and TCO Pool prices historically traded closely together. Recently though, like everything in the Northeast gas market, things are changing.

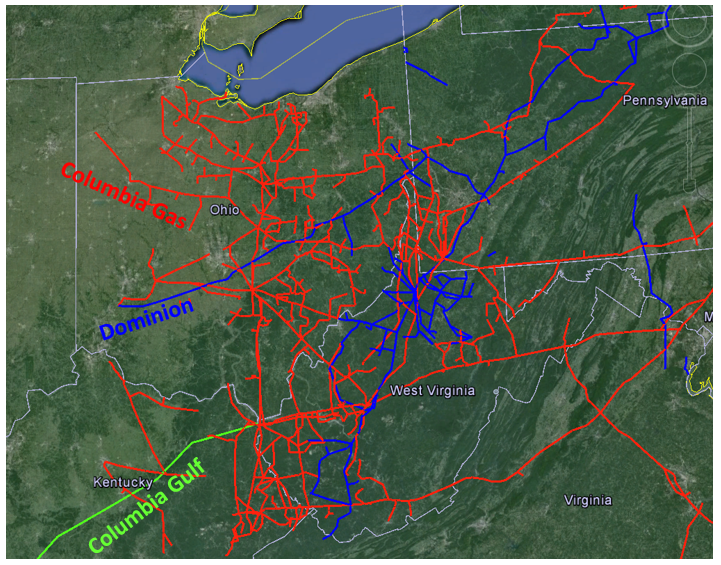

Map Source: EIA, BTU Analytics, and Google Earth

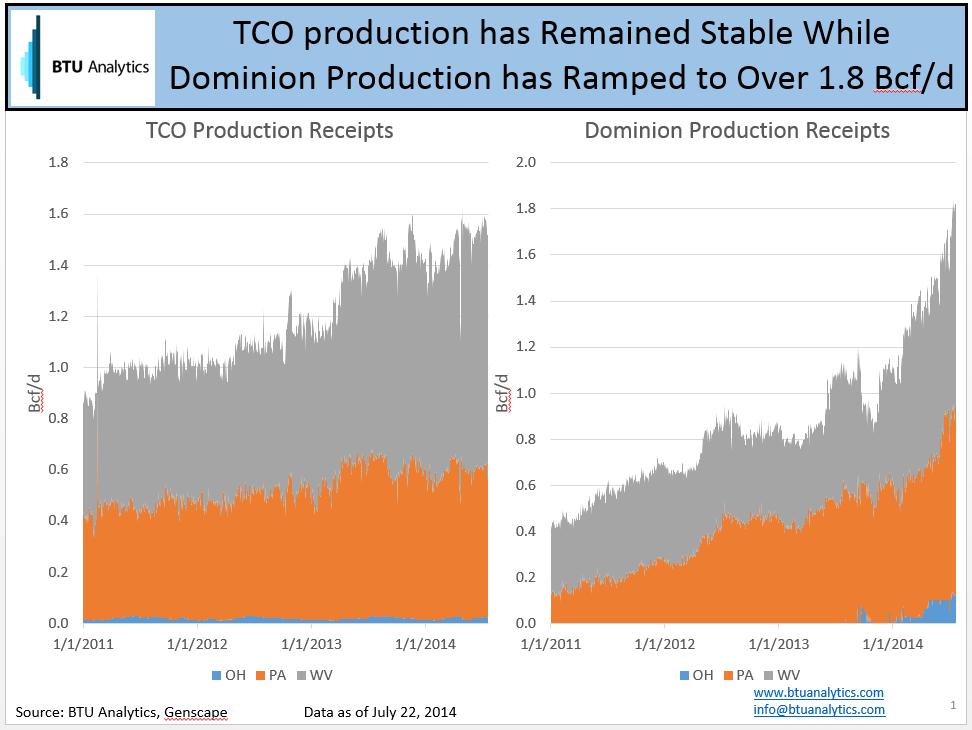

Today, Marcellus & Utica production has grown to over 16.2 Bcf/d, according to Genscape production receipts on interstate pipelines. Growth, however, has not been distributed evenly and is impacting basis differentials even inside the Northeast Market.

If we look at production receipts on TCO and DTI since 2011, we can start to understand why spreads are driving higher. Up until January 2014, production growth on both pipes was at relatively similar rates. The huge jump in production on DTI since January 2014 to present (from approximately 1 Bcf/d to 1.8 Bcf/d) is creating a situation where producers on Dominion in West Virginia, Pennsylvania, and Ohio are forced to discount gas aggressively, well below Henry Hub, as a result of limited pipeline takeaway options from DTI. Meanwhile, TCO production receipts in 2014 have been stable with growth only really occurring in West Virginia. Dominion has historically moved production gas and interconnects from other interstate pipelines like REX, TETCO, & Tennessee north and into the storage hub at Leidy, Pennsylvania. TCO meanwhile has primarily sourced gas from its sister pipeline Columbia Gulf (CGT) bringing in volumes from the Southeast.

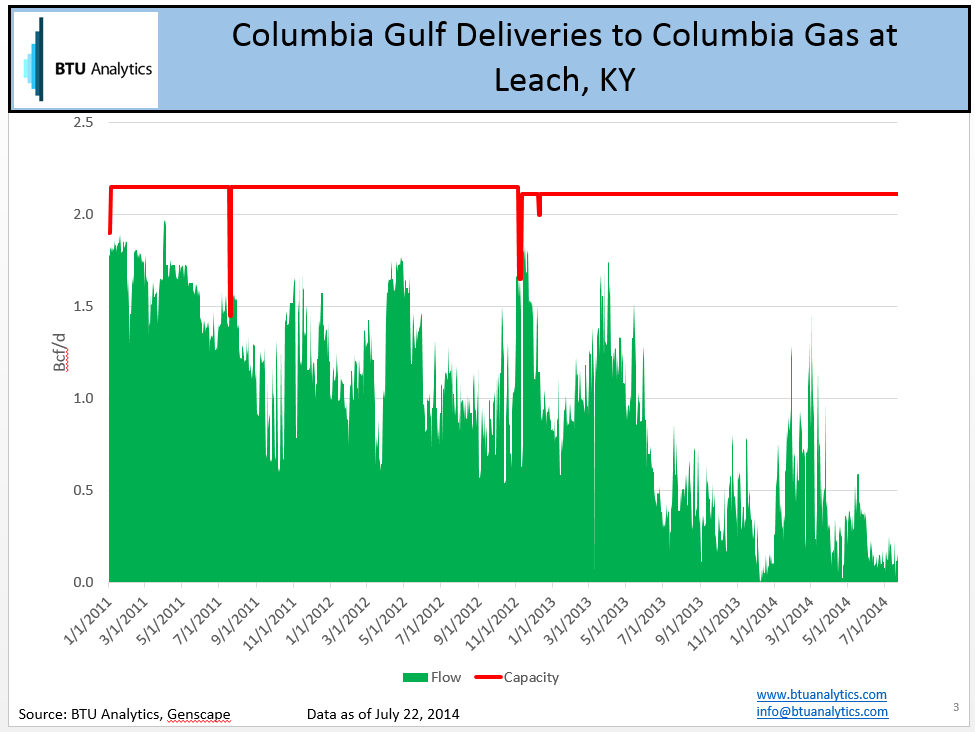

Production growth reaching the TCO system has had a natural outlet to displace inbound flows from the Gulf and have maintained a premium relative to other Northeast supply points. In recent months because of the high rates of growth occurring on DTI, Tennessee, Transco, and TETCO the spread between TCO Pool and Dominion South has diverged to over $1.50/MMBtu.

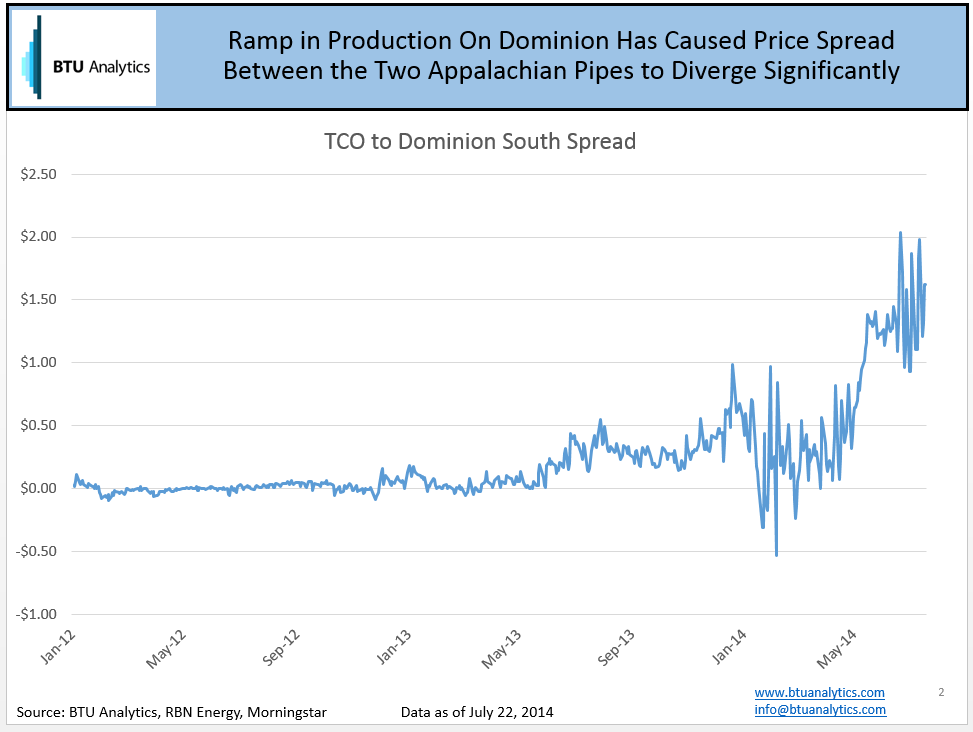

Are $1.50 pipeline spreads between two Northeast supply points sustainable? We think not. As new waves of pipeline infrastructure begin to drain supply out of Ohio expect further price changes to occur.