Since the passage of the Inflation Reduction Act (IRA) earlier this year, most of the focus has been on the bill’s impact on renewables, electrification, and the eventual energy transition. While those will undoubtedly have an impact on the US natural gas market, a more immediate impact could be felt from the expansion of the section 45Q tax credit, particularly as the US enters a period of pipeline infrastructure buildout to meet new LNG demand along the US Gulf Coast. BTU Analytics previously discussed the potential impact of an expanded 45Q tax credit on EOR. In today’s Energy Market Insight, BTU Analytics explores how new projects are taking advantage of the IRA and the potential impacts it could have on the ability to de-bottleneck Haynesville takeaway capacity.

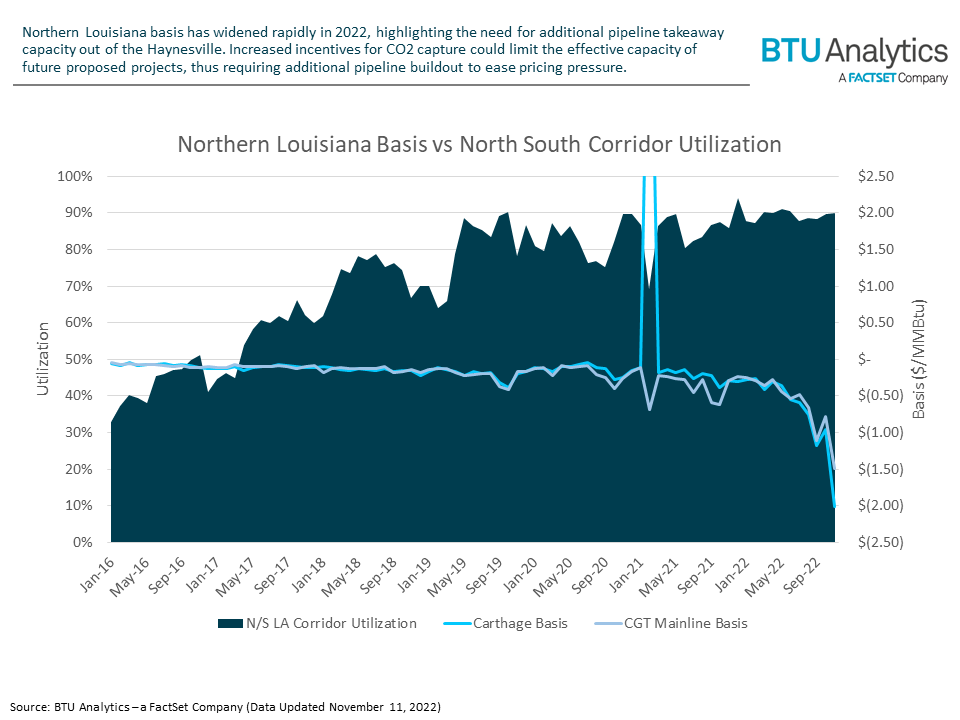

BTU Analytics has long highlighted the North to South Louisiana corridor as a region ripe for new pipeline projects given the level of drilling activity, high dry gas content, and proximity to the Gulf Coast. Over the last few years, this corridor has come under stress as evidenced by increasingly weak basis pricing in Northern Louisiana. Through the first two weeks of November, basis at Carthage and CGT Mainline is averaging $(2.01)/MMBtu and $(1.49)/MMBtu, respectively. This represents the widest monthly average since 2009. Multiple pipeline projects are expected to relieve this pressure over the next five years, beginning with Energy Transfer’s Gulf Run (1.7 Bcf/d) in 1Q23. However, new incentives to increase CO2 capture could have a material impact on new gas takeaway capacity.

In their third-quarter earnings, Williams (NYSE: WMB) directly cited the IRA as a factor in moving forward with the Louisiana Energy Gateway (LEG) pipeline project. Specifically, the proposed 1.8 Bcf/d pipeline will also be accompanied by a CO2 capture and sequestration project. While there are already multiple pipelines that run from North to South Louisiana, LEG will be unique in that the treatment facilities that strip out CO2 from the gas stream will be located at the outlet of the pipeline rather than be embedded in the gathering systems. Under this new setup, CO2 will be captured at the end of the pipeline and sequestered rather than vented at upstream treatment facilities.

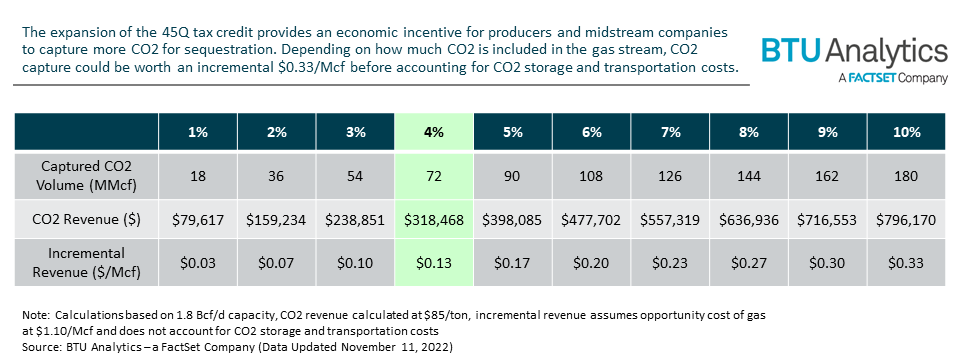

One of the key factors driving the capture of CO2 is the expanded tax credit under section 45Q. Instead of venting the CO2, a process that is extremely harmful to the environment, producers and midstream companies can now derive an economic benefit by capturing CO2 from the gas stream and sequestering it underground. Depending on how much CO2 is included in the gas stream, BTU Analytics estimates that the capture of CO2 could be worth as much as $0.33/Mcf before accounting for CO2 transportation and storage costs. While current estimates of CO2 content in the Haynesville sit around 3–5%, other plays with higher CO2 content could see even more uplift from carbon capture.

Additionally, while the expanded 45Q tax credit is a likely driving force behind the increasing interest in CO2 capture, there are multiple ancillary benefits to the new system layout. For example, adding a treatment facility to the end of the pipeline allows the upstream portion of the pipe to be classified as a gathering system rather than an intrastate or interstate pipeline. This differentiation allows a project to avoid FERC oversight and any regulatory hurdles that typically arise in the FERC approval process (gathering systems still have regulatory requirements but they are not as stringent as the federal requirements). Also, capturing CO2, rather than venting it, allows both producers and midstream companies to boost their ESG credentials. This is becoming increasingly important as investors ramp up pressure on upstream operators and US LNG companies jockey to provide the lowest carbon-intensity LNG cargoes.

However, these benefits come at a cost. For every incremental volume of CO2 moved through the pipeline, an equivalent amount of methane cannot be transported. In isolation, 4% of a 1.8 Bcf/d pipeline is only 72 MMcf/d of lost volume. However, if other proposed projects also adopt this formula, the lost capacity could begin to stack up in a hurry. Indeed, M6 Midstream’s proposed NG3 project (1.7 Bcf/d) will also reportedly include a carbon capture component. With these projects slated to come online as soon as 2024, BTU Analytics will be monitoring how the evolving CO2 market impacts the US natural gas market in our Gas Basis Outlook report. Request a sample here by including “Gas Basis Outlook” in the “Tell us more…” section or by emailing btuanalytics@factset.com.