I don’t spend much time on Twitter, but a trending topic on the social network caught my eye last week: #NEDisDEAD. NED of course refers to Tennessee Gas Pipeline’s Northeast Energy Direct project and the DEAD to Kinder Morgan’s decision last week to shutter the project. On top of that, we heard the news late last Friday that the NY Department of Environmental Conservation denied Constitution’s stream crossing permit. Limited takeaway capacity constrains the Marcellus and Utica’s ability to grow production, so obviously any cancellation or delay in projects would materially impact our production outlook, right? Not quite. At BTU we conducted extensive analysis on not only NED and Constitution, but all major green field projects and existing pipeline reversal projects out of the Northeast. Therefore, looking at NED, when KMI announced the project’s suspension we weren’t very surprised and in fact, our production outlook for the Marcellus and Utica in regards to NED’s cancellation remains unchanged.

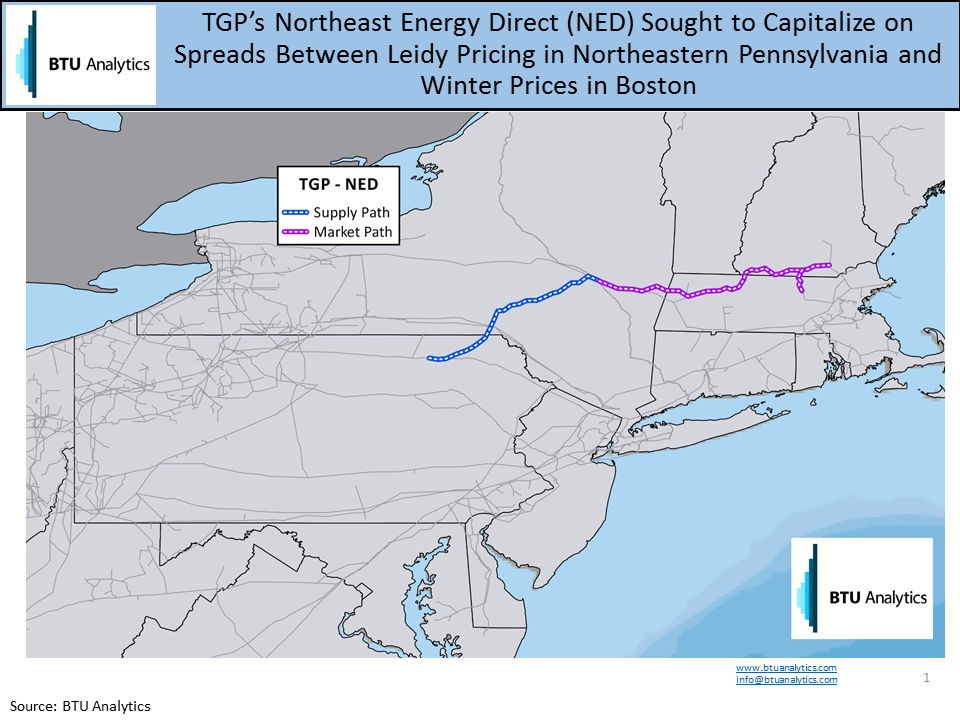

Since the start, NED hit market headwinds in its goal to capitalize on spreads between depressed Marcellus pricing and Boston citygate pricing, which has historically been prone to blow outs during the coldest parts of the winter. Initially slated to come online with a capacity of over 2 Bcf/d, NED was repeatedly downgraded until its most recent capacity of 1.3 Bcf/d. However, due to the high cost of the project and competition from similar Algonquin pipeline projects, even at that reduced capacity we estimate that NED achieved only about 60% shipper commitments.

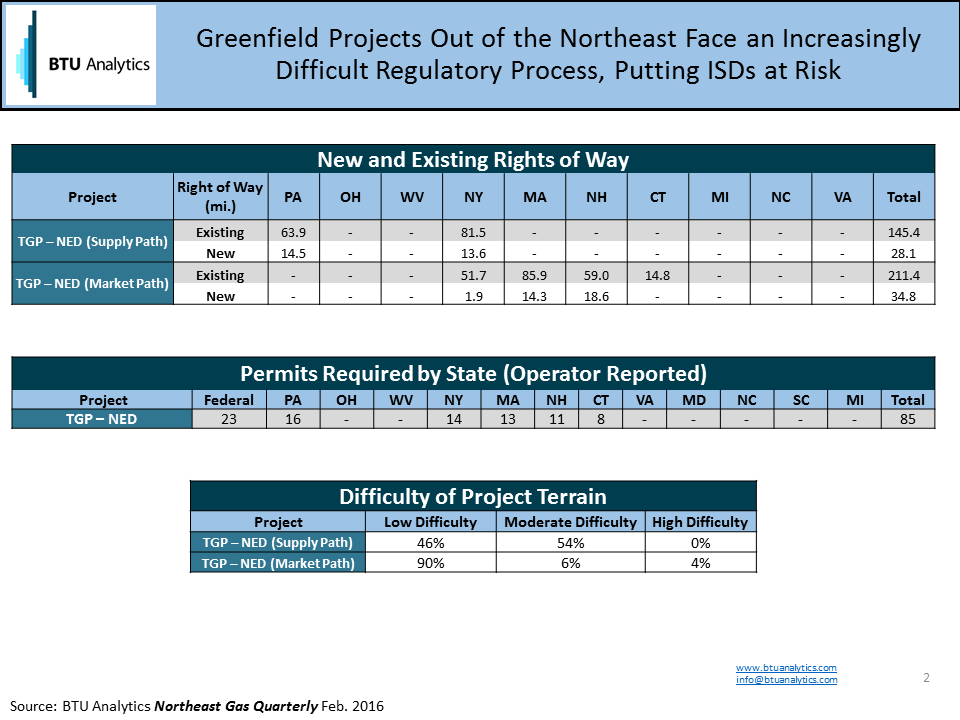

Beyond challenges getting demand side entities to commit to capacity, NED faced high hurdles on the regulatory front. Because of the importance of takeaway projects out of the Northeast and their impacts on production, in Fall 2015 we dug through individual projects’ federal applications, as well as Federal Energy Regulatory Commission (FERC) rulings to get a sense of the risks facing each of these projects. Below shows a snapshot of the analysis we look at when determining a project’s delay risk; specifically focusing in on TGP’s NED project.

New versus existing right-of-way gives a glimpse into how much negotiation a pipeline operator will have to do with individual land owners, as new right-of-ways require more negotiations in addition to land surveying. The number of permits required in each state, coupled with how stringent each of those states can be during the permitting process, show the obstacles faced with state regulators. NED illustrates the difficulty of building into New England which would have required 85 permits (as opposed to the Atlantic Coast Pipeline, which requires about 50 permits) before construction could commence. Beyond regulatory risks, sheer construction challenges must also be taken into account. In the table above, this is measured by the susceptibility to landslides of the terrain that a project must cross.

Taking all of these risks into account, BTU Analytics concluded that the challenges faced by NED were too much for an on-time in-service date (ISD). In fact, out of all the green-field projects we examined, NED received the longest delay. BTU’s delayed NED ISD was so far out, we expect open capacity out of the Northeast to exist, so the era of Northeast growth constrained by takeaway capacity will be over, leaving demand dictating Marcellus and Utica growth. For this reason Kinder Morgan’s announcement does not materially impact our Northeast forecast.

The NED and Constitution announcements have bolstered pipeline opponents in the region. While the NED cancellation does not impact our Marcellus gas production forecast, a delay of Constitution from Fall 2017 to Fall 2018 will impact our forecast. Now which Marcellus/Utica gas pipeline will be the next focal point for opponents? For more on the impacts of possible infrastructure delays, request a sample of BTU Analytics’ Northeast Gas Quarterly. If you would like a sample of BTU’s comprehensive list of Marcellus and Utica infrastructure projects, including capacities, receipt and delivery markets, and both official and BTU-risked in-service dates, request one here.