North American natural gas and LNG export bulls should be excited about the future. Today’s Energy Market Commentary will review trends in global energy consumption and the potential impacts of 7.7 billion people on global natural gas demand. Specifically, we will compare North American energy consumption to China and India, seeing as these countries represent 2.8 billion people (1.41 and 1.36 billion people respectively). As both economies continued to develop, the stage is being set for a bullish global gas demand story.

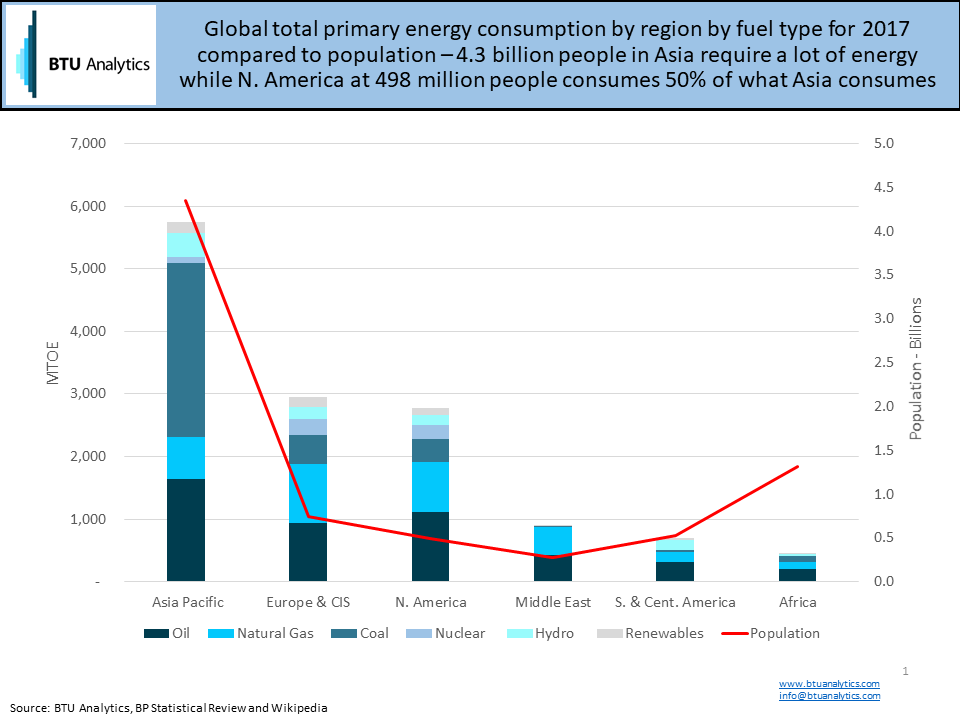

As shown below, the 4.3 billion people in Asia utilized almost 6,000 MTOE of energy in 2017. Conversely, in North America, 498 million people use nearly 3,000 MTOE of energy annually. Despite over 8 times as many people, Asia today consumes only double the total energy of North America.

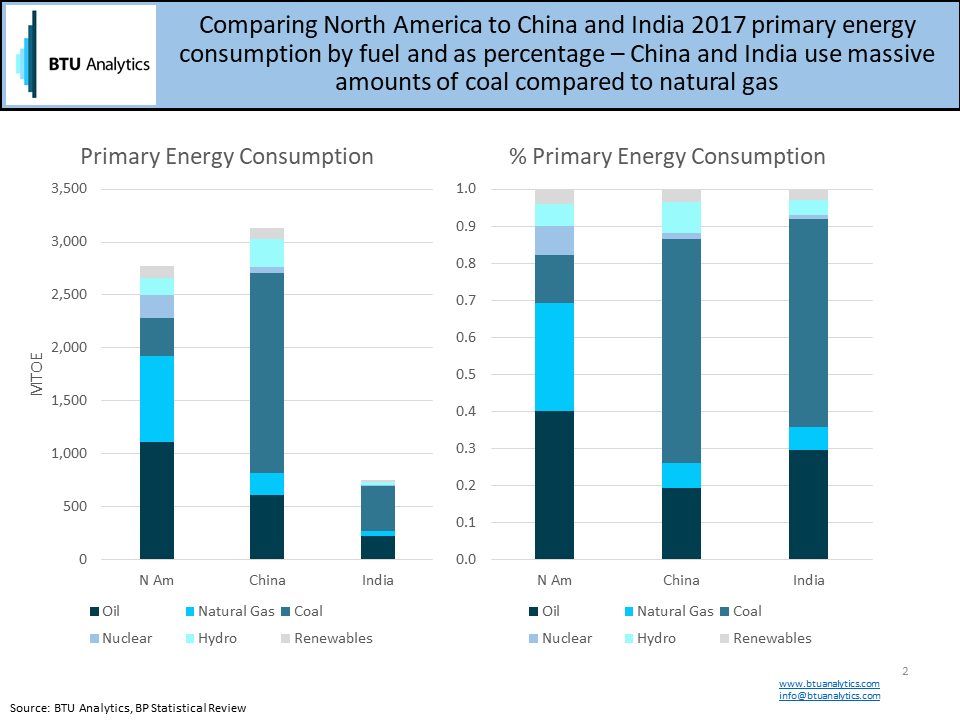

The chart below compares North American energy consumption to China and India. The chart highlights the heavy reliance by China and India on coal. Coal accounts for 60% and 56% of total energy use respectively. North America uses a more broad distribution of fuels at 40% oil, 29% natural gas, and 13% coal. Today, the two Asian economies and the North America have vastly different distributions of heavy industry, manufacturing, and services. However, as the Chinese and Indian economies mature and standards of living increase, then total energy demand will likely greatly increase. Additionally, if China and India want to either decarbonize their economies or improve air quality then the fuel distribution mix is likely to change substantially over time.

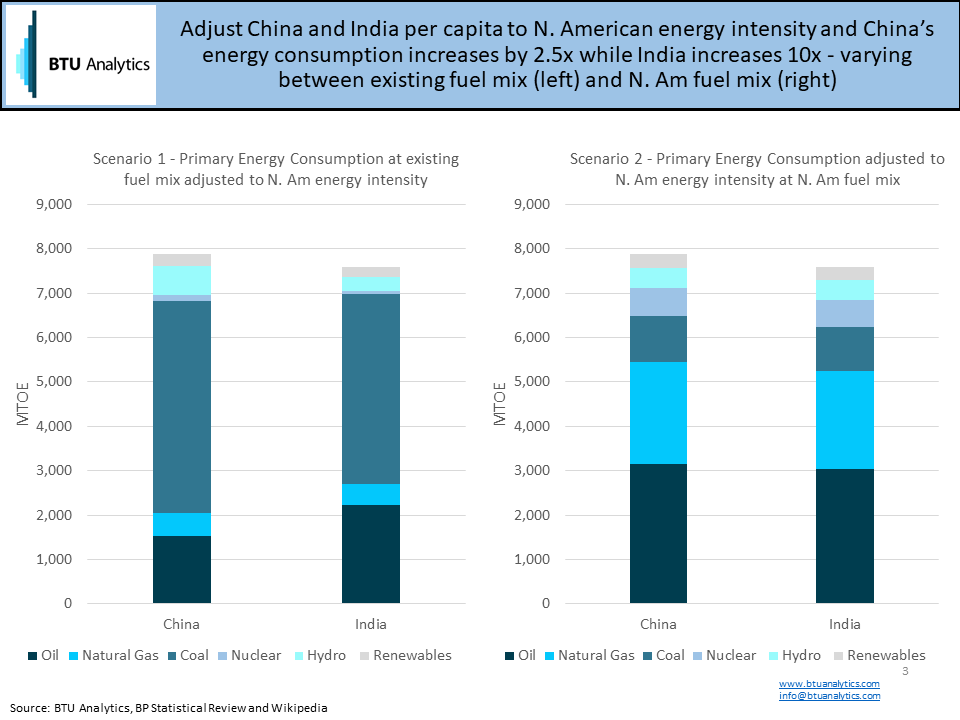

The below chart highlights two potential scenarios for future demand in China and India using North America as a proxy. In scenario 1, Chinese and Indian consumption is adjusted to consume energy at the same rate on per capita basis as North America. In the left chart below, China’s energy consumption would increase 2.5 times, while India would increase nearly 10 times. The biggest impact though would be to the consumption of coal if China and India do not change their fuel mix. In Scenario 2 below, Chinese and Indian energy demand is adjusted to the same fuel mix as North America. This scenario could result if China and India move towards decarbonization without leapfrogging natural gas to renewable generation sources. As a result, oil and natural gas consumption leap higher while coal consumption declines in China and remains relatively flat in India to 2017 levels.

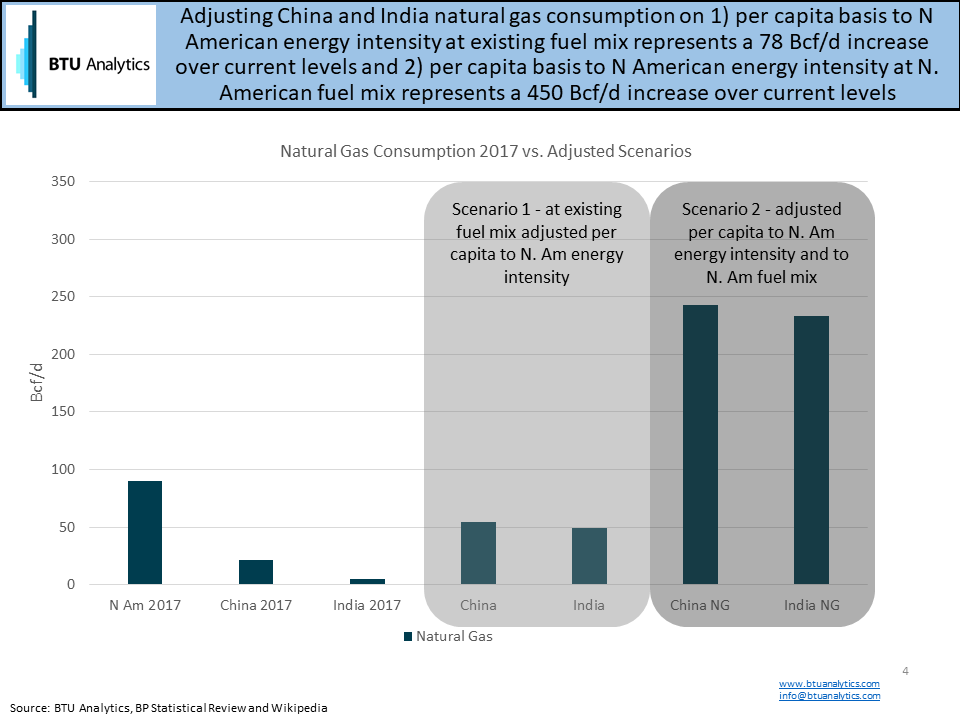

Under either scenario, gas consumption increases dramatically. The chart below converts the natural gas consumption outlined above from MTOE to Bcf/d. In 2017, the North American gas market at ~90 Bcf/d dwarfs China and India at 22 Bcf/d and 5 Bcf/d respectively. However, if Indian and Chinese consumption were to mirror the energy intensity of North America, they would require an incremental 78 Bcf/d of natural gas. In scenario 2, a ‘decarbonized’ China and India would require a staggering incremental 450 Bcf/d of natural gas to consume energy at the same per capita rate as North America and at the same fuel distribution mix.

All economies go through energy transitions over time in an ever evolving dynamic moving towards higher quality and lower carbon fuels. What are the takeaways from these scenarios? The main point is the potential demand for natural gas is immense as highlighted by just looking at China and India. Note, this analysis left out another 1.6 billion people in the rest of Asia and another 1.3 billion people in Africa (a total of 2.9 billion people) who all have growing energy needs as well.

What does this potentially mean for North American LNG exports over the next decade? Considering the scenarios above, incremental global gas and LNG demand should remain robust even if we assume significant competition from renewables and pipeline gas development in Asia. In 2017, global LNG trade represented approximately 38 Bcf/d. North America LNG exports will exit 2019 with approximately 10 Bcf/d of capacity. Can strong Asian LNG demand require a double of North American LNG export capacity to 20 Bcf/d from ‘Wave 2′ LNG exports? With three North American LNG export FIDs in the last 6 months announced, follow BTU Analytics’ view on further ‘Wave 2’ LNG export project development by requesting more information about the Henry Hub Outlook.