While much of the US industry is focused on growing crude production and the constraints, we are beginning to field questions on supply sources likely to be tapped when the second wave of LNG comes to fruition. One often overlooked area that factors predominately into our long-term outlook is the contribution of the dry Eagle Ford. Today’s commentary checks in with a region that has fallen out of favor, to get an understanding of resource potential that is likely to be called upon should US LNG exports meet the bullish expectation of some in the market.

This topic came to light as we were examining GPM (gallons per Mcf) trends in the gas stream across the country. Gas-focused plays can produce both wet (high GPM) and dry (low GPM) gas. Oil-focused basins produce an associated gas stream full of NGLs (high GPM). BTU Analytics’ proprietary wellhead level GPM and NGL composition production model allows our analysts to uncover trends in composition and recovery changes that can highlight future opportunities.

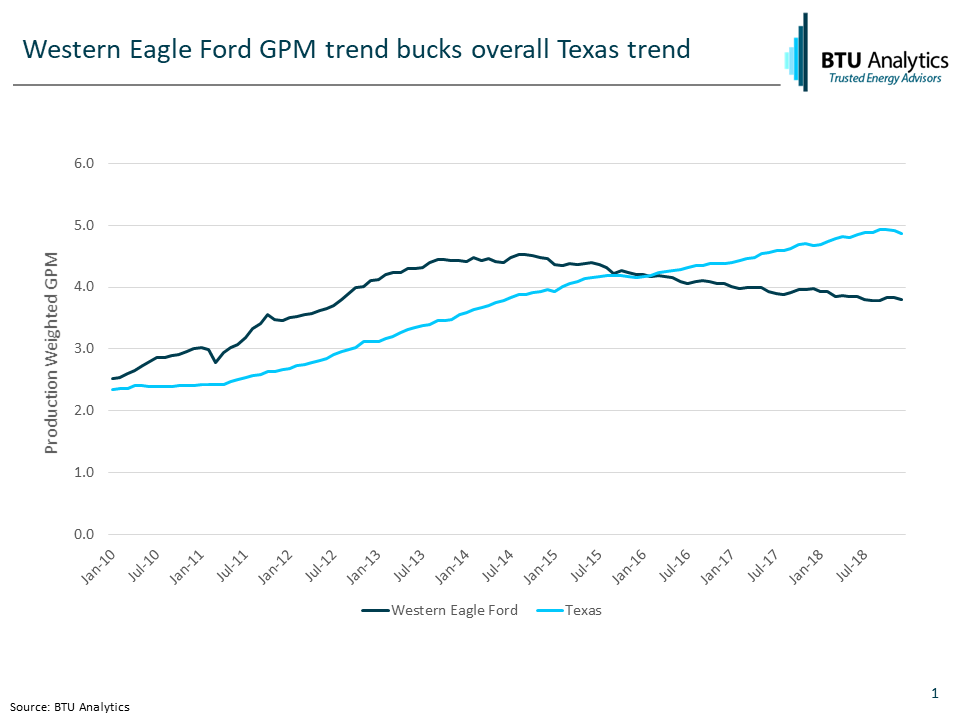

The chart above shows the production weighted average natural gas liquids content measured in GPM for Texas, which has been steadily growing from 2.3 in 2010 to 4.9 by the end of 2018. The Western Eagle Ford follows the trend through 2014 and has a higher GPM than the Texas average through 2015 when the GPM in the Western Eagle Ford falls.

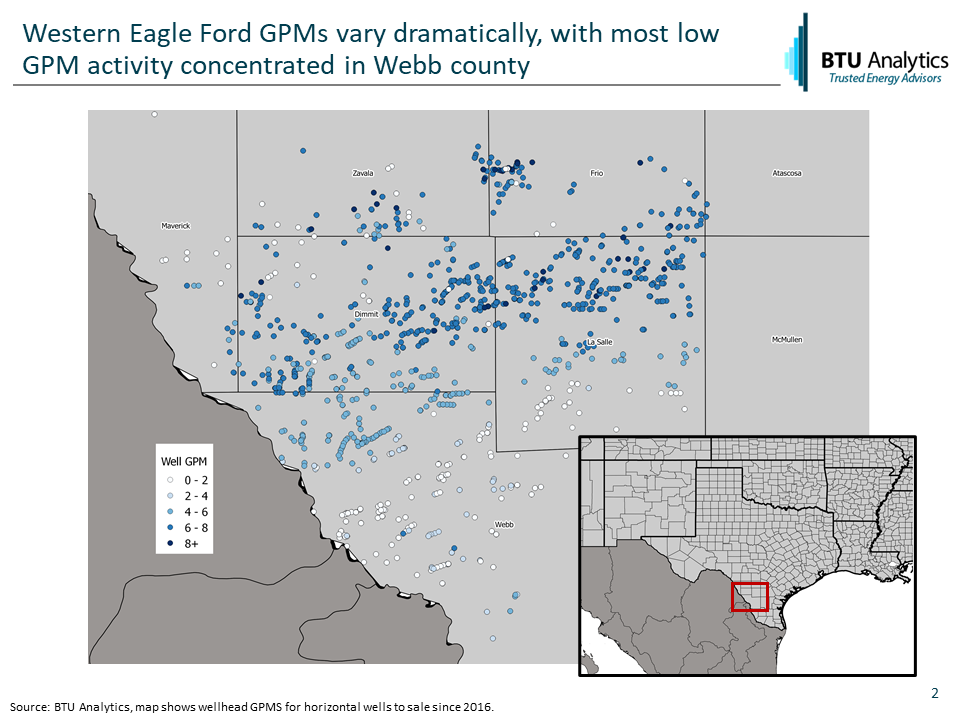

Falling GPM levels in the Western Eagle Ford signal that the overall balance of oil-directed drilling versus gas-directed drilling is possibly shifting. Viewing the data on a map shows that much of the activity in central Dimmit and northern La Salle counties has a wellhead GPM in the 6-8 range. Southern Webb and La Salle county have 0-2 GPM gas while northern Webb and southern Dimmit county have gas in the 4-6 GPM range. With the production weighted GPM falling, a greater proportion of the region’s gas is coming from wells with a natural gas liquid content under 4 GPM.

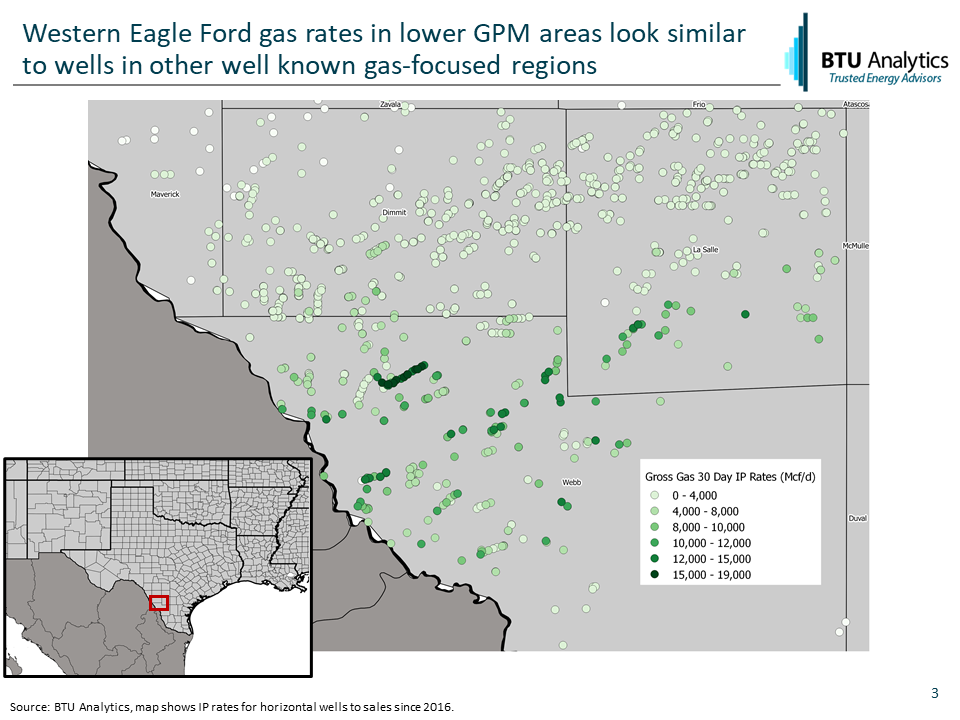

Zooming in on the lower GPM areas, we can see hotspots where wells with IP rates in excess of 12 MMcf/d have been turned to sales.

While producers might not discuss their dry Eagle Ford results much these days, well results to-date do remind us that gas resources are abundant in areas besides the Haynesville or Appalachia. As a point of reference, the average IP rate in the Haynesville is approximately 15 MMcf/d. While the average IP rates in SW Appalachia are between 8 and 13 MMcf/d.

Wave 2 of LNG will likely bring gas resources back into the market’s focus soon and supplying wave 2 of US LNG exports will be more complicated than the market expects. For BTU’s views on the complications and opportunities, request more information on our natural gas suite of products, including the Upstream Outlook, Gas Basis Outlook and Henry Hub Outlook.