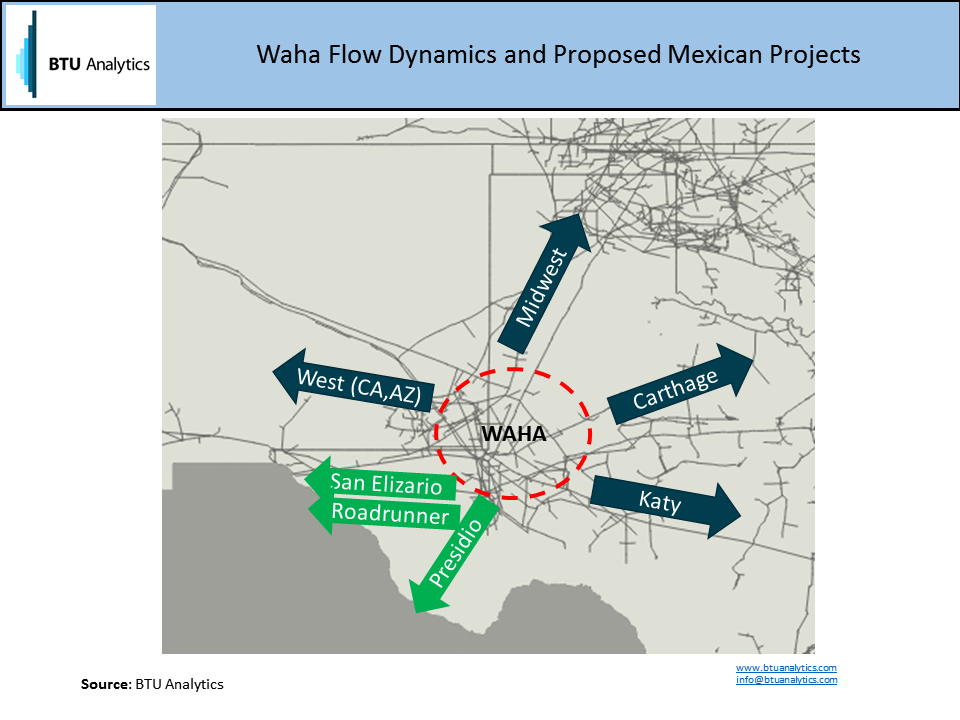

Mexico is undergoing a strategic shift in its primary fuel source for power generation from fuel oil to natural gas. In order to meet its 2028 goals, the Comision Federal de Electricidad (CFE) is developing significant infrastructure projects. For natural gas, this translates into 35 GW of new natural gas fired generation compared to 21 GW of existing capacity in 2014. In order to supply this new generation capacity, the CFE plans to add at least 7.7 Bcf/d of new natural gas infrastructure capacity by 2028 including, 3 Bcf/d of projects from the Waha market that are already under development. The Waha market is located in Southwest Texas and Southeast New Mexico, near the Mexican border, and distributes Permian Basin gas to the West, the Midwest, and East Texas gas markets. It currently provides access to Arizona and California markets via El Paso and Transwestern pipelines, the Midwest market via NNG and NGPL, and also connects West with East Texas via intrastate pipelines to Carthage Hub in Northeast Texas (e.g. Atmos) and Katy Hub in Southeast Texas (e.g. Oasis).

The Presidio and San Elizario pipelines, expected to be in service in 1Q2017, will add takeaway capacity from Waha to the Mexican border where they will connect to new pipelines in Mexico under development by IENova. On the US side, the winning bidders of both projects were the consortium formed by Carso Energy, Energy Transfer Partners and MasTec, Inc. On July 30th, ONEOK announced CFE as the anchor shipper for its WesTex expansion project, the Roadrunner Gas Transmission pipeline, which will also move gas from Waha to a new interconnect on the US/MX border near San Elizario, TX.

The proposed pipelines shouldn’t have a problem finding supply as the Permian currently produces 5 Bcf/d of natural gas and is expected to grow to 5.7 Bcf/d by 2020 (BTU’s July Upstream Outlook). Even though all gas from Waha currently has a home in a downstream market, there is potential for Waha gas to be displaced on pipelines currently targeting the Midwest (NNG and NGPL) as pipeline reversals and expansions from the Marcellus and Utica target the Midwest markets (for more on Northeast Dynamics see BTU Analytics, A Firm Dilemma) .

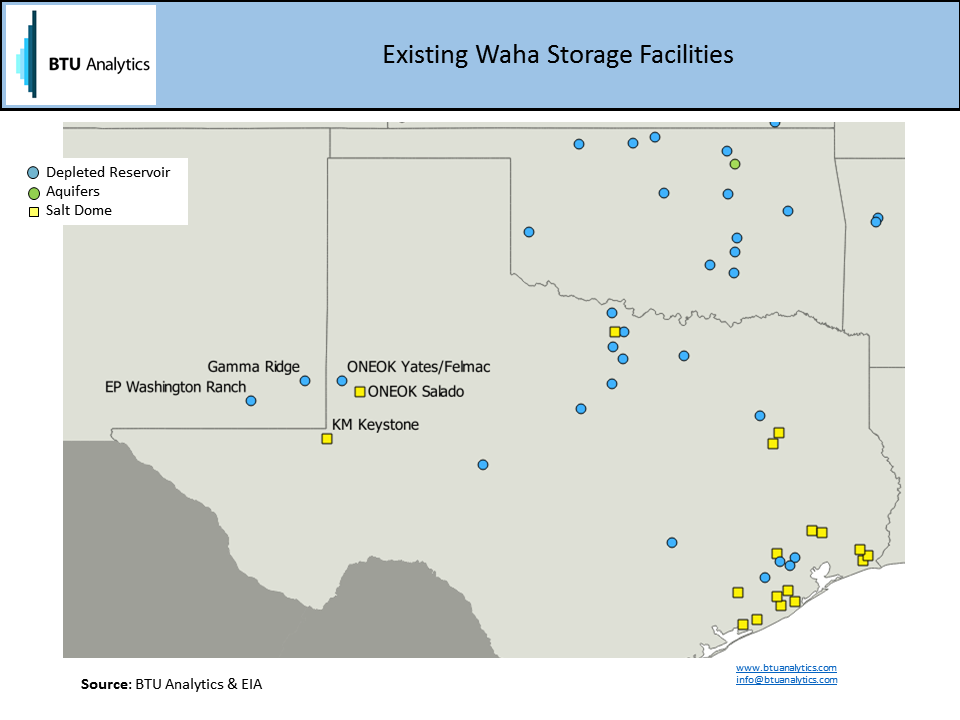

With plenty of local production and new pipeline capacity to serve new power generation, the market component that seems to be missing at Waha is flexible storage. Power load on natural gas pipelines can be highly seasonal (summer versus winter), and even hourly load fluctuations can be quite dramatic as temperatures rise increasing air conditioning loads. In order to meet these daily fluctuations in load, natural gas pipelines rely on both depleted reservoir and salt dome storage.

While the Waha market has 61.6 Bcf of depleted reservoir storage with 0.53 Bcf/d of deliverability, natural gas storage salt dome facilities are not really available near Waha. In the state of Texas, 27% of the working gas capacity and 59% of the deliverability is provided by salt dome storage caverns, but most of these facilities are located on the East side of the state along the Gulf coast. Only two small salt domes are located in the Waha area and currently meet the existing demand needs of the market. KM Keystone Gas Storage has a 6.4 Bcf of working gas capacity and 0.4 Bcf/d of deliverability and connects to El Paso, Transwestern and NNG to provide support for the West market, which is expected to rely on Waha as a supply source. The other cavern is the ONEOK Texas Salado Salt Reservoir in Gaines County, TX, with 2 Bcf of working capacity and 0.2 Bcf of withdrawal capacity and mostly serves ONEOK’s intrastate pipeline systems.

Over the five year period between 2010 and 2014, Waha basis traded an average of $0.076/MMBtu below Henry Hub. In 2015 (settlements Jan-July, forwards Aug-Dec), basis is averaging over -$0.10 as produced gas is trapped due to limited infrastructure, but starting in 2017 the forward market is already reflecting the impact of the Mexican pipelines and is currently trading at an average of -$0.08 in 2017. In 2018 and beyond, basis is near flat at only $0.02-$0.03 below Henry and switches to a premium (positive) basis every August, the peak month for summer demand. BTU Analytics expects Waha basis to tighten even more as gas flows materialize from these projects and the actual needs of the Mexican power sector take shape.

While there may be plenty of natural gas storage capacity in the US in aggregate, specific locations may have a need for new storage as demand grows and flow patterns shift across North America. Could Waha be a potential location for new storage developments to help meet daily market demand in Mexico?