Ready or not, here it comes. Sub-$3 Henry Hub gas prices are here, and the culprit isn’t hard to identify. January gas storage withdrawals have severely underperformed, exemplified by a historic injection, leading to a relative glut of natural gas in the U.S. market. As a result, the outlook for U.S. gas pricing has progressively weakened as winter has gone on. With robust associated gas production growth driven by supportive oil prices in 2023 and limited upside for U.S. demand, a cold end to the winter may be the only thing preventing a free fall at Henry Hub.

BTU Analytics has been calling for a precipitous decline in gas prices since last summer. While Lower 48 gas storage spent most of the summer at a significant deficit to the five-year average, gas fundamentals pointed to an eventual storage surplus entering 2023, depending on the weather. As we wrote in the October edition of the Henry Hub Outlook, “If production growth continues as expected, seasonally mild temperatures at the start of winter could place increased downward pressure on Henry Hub pricing.” Today’s storage report for the week ending January 20th showed U.S. gas inventories now sitting at 2.73 Tcf, a 128 Bcf surplus to the five-year average. Unsurprisingly, gas markets have reacted negatively to three consecutive weeks of bearish storage reports. The forward curve is now averaging $3.22/MMBtu for Summer 2023, with months at the front of the strip settling as low as $2.92/MMBtu on January 25th.

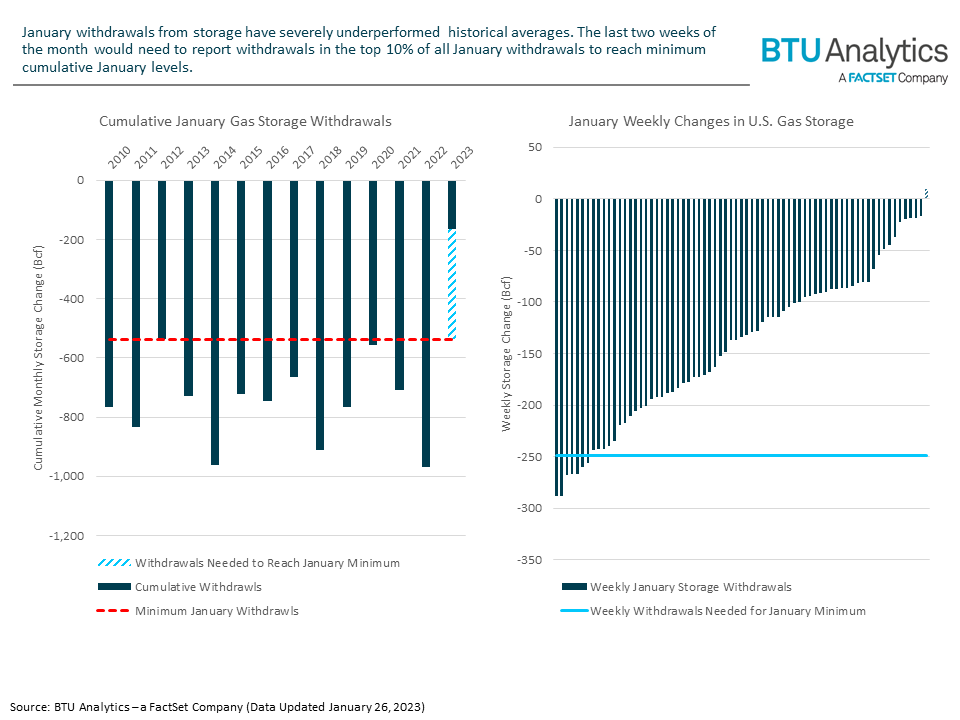

These recent shifts in the forward curve show the market beginning to respond to weakened gas fundamentals. However, the recent drop in pricing is still not reflective of just how disastrous January has been for storage levels. The smallest January withdrawal since 2012 totaled 536 Bcf, making the January-to-date withdrawals of 165 Bcf only 30% of the previous low. In fact, the last time the market recorded a below-normal January withdrawal was the 558 Bcf withdrawal in January 2020, when Henry Hub averaged $2.01/MMBtu. Just getting back to minimum January storage withdrawal levels would require an average weekly withdrawal of approximately 249 Bcf, which would be in the top 10% of withdrawals over the last decade. Should the market be unable to meet the required withdrawals to reach a normal January level, the January 2020 exit suggests prices could fall even further.

So, can a cold February make up the difference? In short, it’s unlikely. Storage is expected to exit January with over 200 Bcf of additional gas in storage compared to end-of-2022 expectations. With February withdrawals averaging 572 Bcf over the last 12 years, making up the January deficit will require total February withdrawals of over 775 Bcf. That mark has been eclipsed just once in the last 12 years: in 2021 because of Winter Storm Uri. While it’s never wise to count out extreme weather events disrupting the U.S. gas market, a potential winter storm could be the only thing keeping the bottom from dropping out of Henry Hub. For more analysis on U.S. gas storage and its impact on Henry Hub pricing, request a sample of BTU Analytics’ Henry Hub Outlook report.