Players in the Marcellus and Utica have been eagerly waiting years for the time when new takeaway out of the basin would come into service and, hopefully, relieve price weakness. Well, that time is finally upon us. Energy Transfer’s Rover is in-service (mostly) and a spate of other projects, such as NEXUS, Mountain Valley Pipeline, and Atlantic Coast Pipeline is well under construction. However, the next project slated to come into service will be Williams’ Atlantic Sunrise, with Williams recently reaffirming an August start-up. So, what can we learn about drilling activity and new production for Rover that we can apply to the coming Atlantic Sunrise?

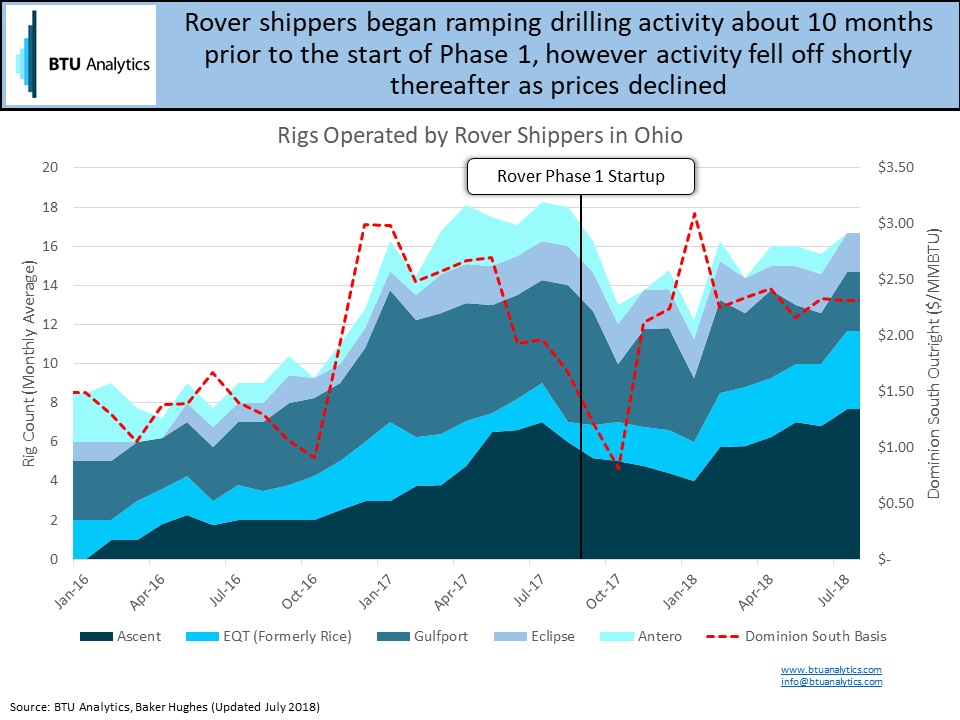

Let’s start by looking at the run-up in drilling activity prior to Rover coming online. While Rover’s construction was hindered by regulatory challenges and multiple delays, there is value in understanding how project shippers responded as the project progressed. The graphic below shows how shippers ramped drilling activity in the run-up to Rover’s anticipated in-service date. Of the all the shippers, Ascent, who holds the most capacity on the project picked up activity the most in the first half of the year, added about 3 rigs.

Shippers on Rover began ramping up drilling activity about 10 months prior to the anticipated summer 2017 in-service date, which is somewhat in-line with the average 2017 spud-to-sales time in the region of about eight months. Following the ramp up, however, drilling activity began to fall as Dominion South prices declined with weak shoulder season demand. We also have to keep in mind that some of this ramp is possibly attributable to other projects coming online since Rover’s shippers are subscribed to multiple projects in the region.

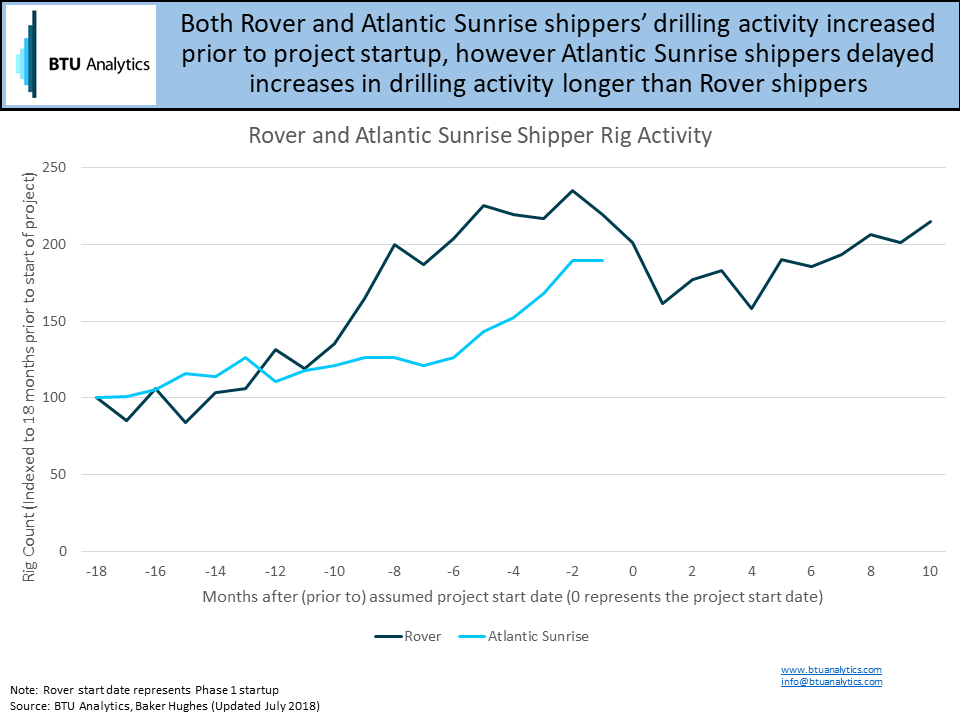

Have Atlantic Sunrise shippers been following a similar activity trajectory? Turns out they have. Atlantic Sunrise’s shippers are more consolidated with only three major shippers (Cabot, Chief, and Seneca), however, they have shown similar trends to Rover’s shippers in the ramp up of activity. The next graphic shows rig activity levels for each project (indexed to 100) 18 months prior to the start of the project. The x-axis of the graphic shows the number of months before or after the project enters service. Negative numbers are months prior to the start of service, positive numbers represent the number of months after the start of service, and zero represents the month the project started service.

So, like Rover shippers, Atlantic Sunrise shippers have also ramped up their drilling activity. The ramp up in earnest began slightly later than Rover’s and to a lesser degree, which makes sense when considering Atlantic Sunrise’s capacity is less than half that of Rover’s, and well productivity differs between Southwest Appalachia for Rover and Northeast Pennsylvania for Atlantic Sunrise.

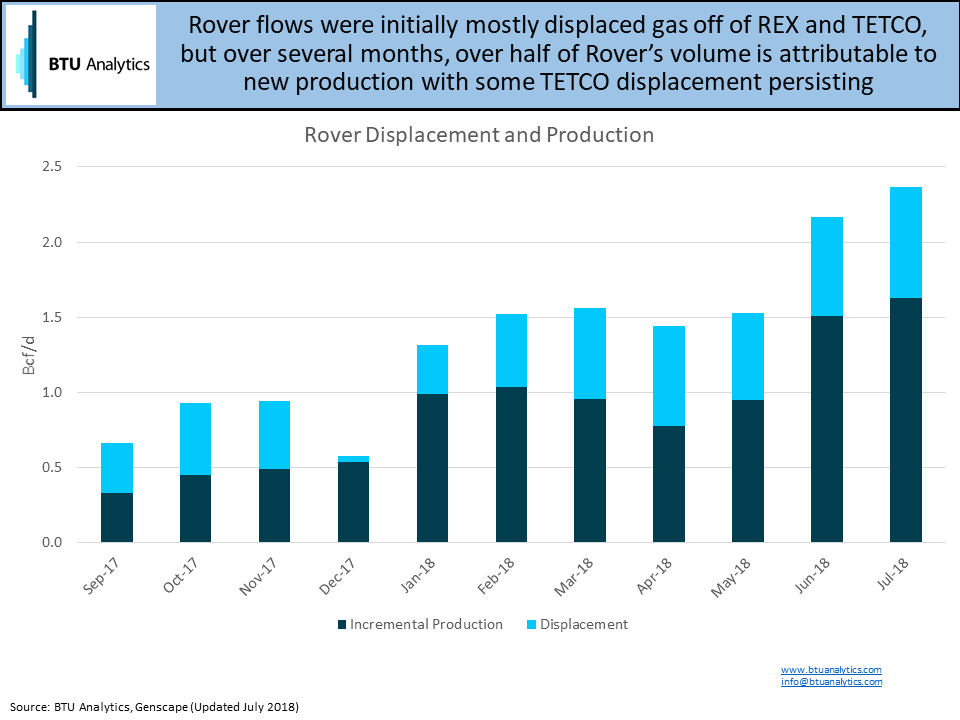

Drilling is one thing, but what about production from these new takeaway projects? Cabot, who holds 1 Bcf/d of commitments on Atlantic Sunrise, has openly stated they intend to fulfill their commitments initially with a combination of redirected volumes and new production, so we shouldn’t expect a one for one bump in new production with takeaway capacity coming online. This is a similar story to what we saw with Rover. In fact, about a third of the molecules on Rover today are being re-directed off of other pipes. This graphic breaks down the source of flows we have observed on Rover.

How much new production can we expect to see attributable to Atlantic Sunrise coming online? And, possibly more importantly, how will regional prices react with new takeaway coming online? See our upcoming edition of the Northeast Gas Outlook for BTU Analytics’ forecasts of capacity, production, prices, and more.