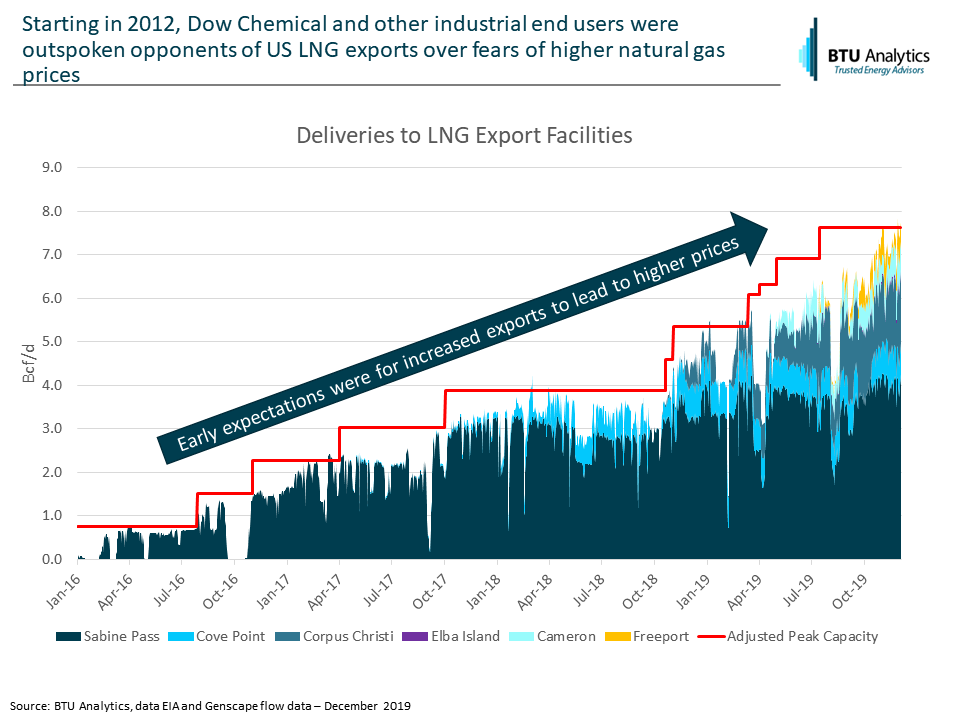

As the shale gas revolution ramped up from 2008 to 2012, the US LNG industry quickly pivoted flipping import terminals to planned export terminals. By 2012, US natural gas end users started to become organized. End users voiced opposition to growing LNG export volumes over fears that increased US demand would lead to higher Henry Hub natural gas prices. Dow Chemical was one of the more vocal opponents to the LNG export permitting process. While US LNG export volumes are reaching all time record levels in 2019(as shown below), so far, the premise that increased LNG exports would drive US natural gas prices higher has been unfounded. The question going forward is, with current low levels of natural gas prices and E&P capital discipline leading to rig cuts, will prices be forced to move higher in 2020 and beyond?

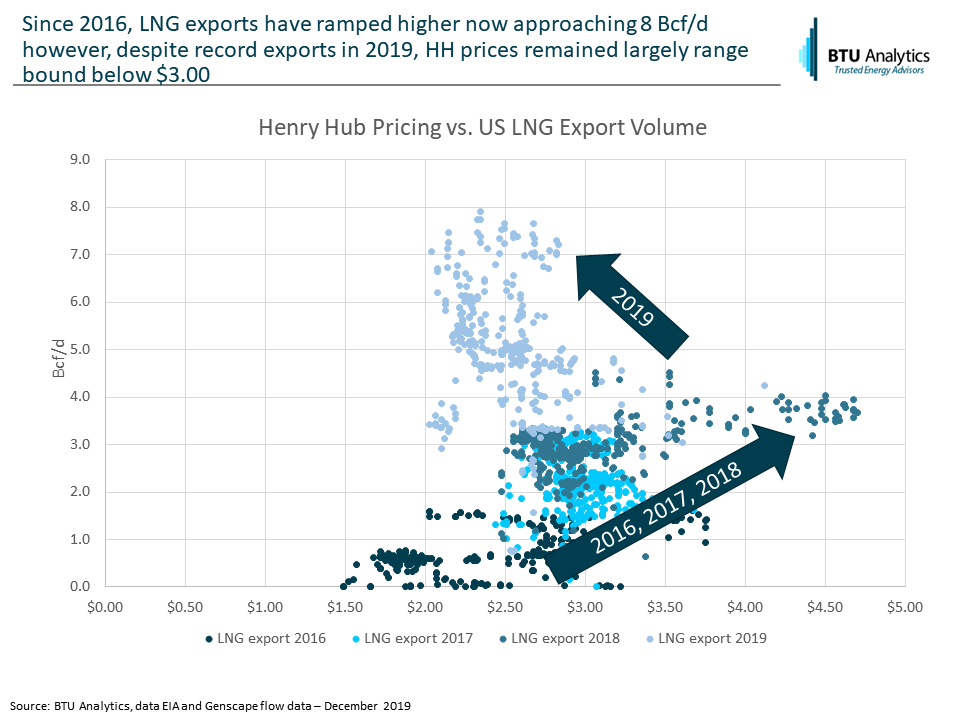

Plotting daily Henry Hub pricing against deliveries to US LNG export terminals shows several trends. First, in 2016, 2017, and 2018, in general, as LNG export volumes increased, prices did move slightly higher approaching $4.50 plus on some peak winter days. When end users voiced concerns about LNG export, this was the trend that was feared; as exports grow, prices will increase. However, in 2019 exports moved from 3.5 Bcf/d to almost 8.0 Bcf/d but Henry Hub pricing has remained range bound between $2.00 and $3.00 for the majority of the year as shown below. This phenomena is the exact opposite of the end users fears from 2012.

There are many dynamics that helped achieve this trend in 2019. These include surging dry gas production from Appalachia and Haynesville as well as associated production growth from the Permian, Oklahoma, Eagle Ford, DJ, PRB and Bakken. In addition, the impact of new pipeline capacity coming into service increased supply available to demand and included the following pipelines: Atlantic Sunrise, Rover, Nexus, and Gulf Coast Express.

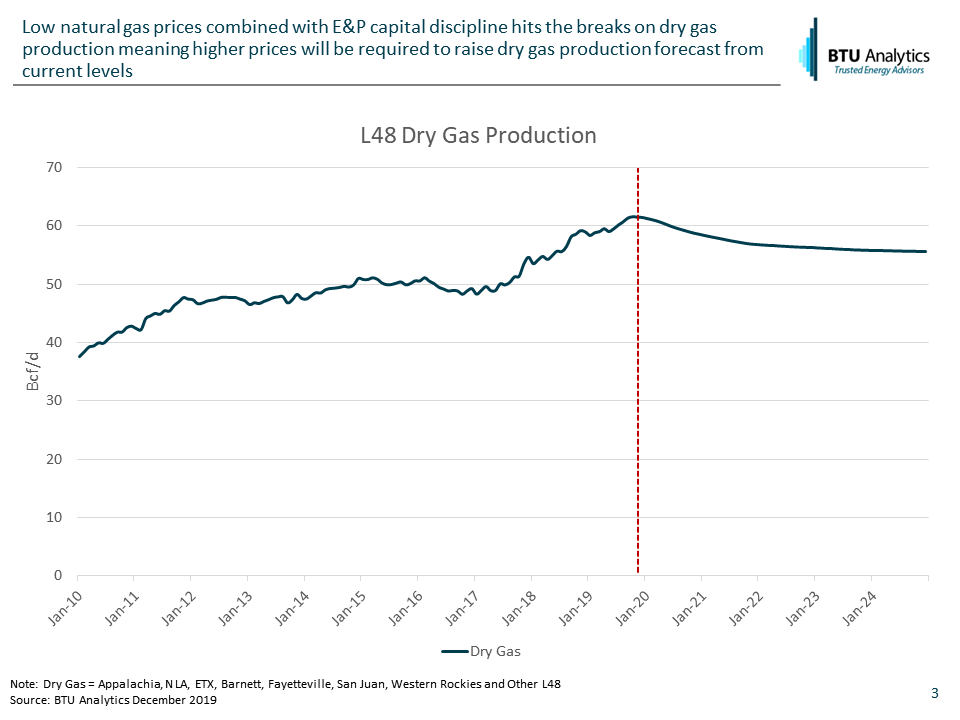

Looking forward for gas, will Henry Hub prices rocket higher as production falls? Wall Street fatigue with E&Ps is palpable at this point. The message of ‘capital discipline’ is being adhered to as best it can by E&Ps. Deliver free cash flow, sell non-core assets and use proceeds to reduce debt, increase the dividend and conduct share buybacks. Many gas E&Ps are cutting guidance and looking at going into maintenance mode. Consequently, with each week, the rig count has declined through fall 2019. The forward outlook for dry gas production from gas focused plays shows declining production at current rig counts. Should oil prices falter or Permian pipelines delay further, natural gas pricing in the forward market would need to move higher to bring more production into the market. Considering hedging and operational momentum, the end users’ fear of higher gas prices due to LNG is likely not a threat in 2020, but by 2021 the dynamic may finally shift. To follow gas market supply and demand balances, request more information on the BTU Analytics’ Henry Hub Outlook.