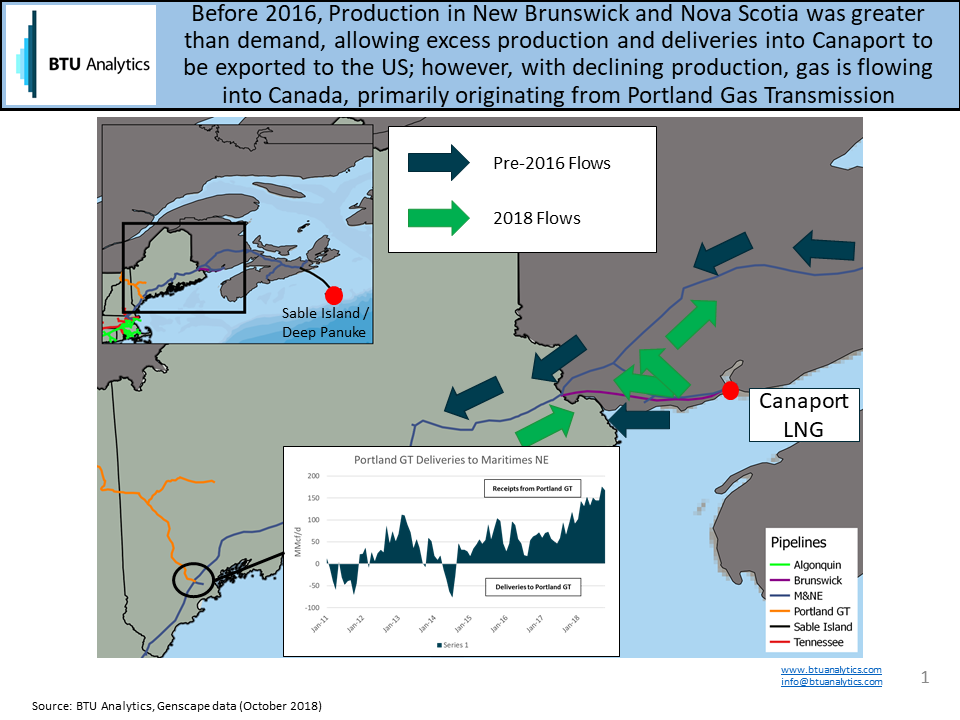

With already low natural gas inventories in the eastern US, any incremental pull on limited supply along the East Coast could cause additional price volatility this winter. In the eastern Canadian provinces of New Brunswick (NB) and Nova Scotia (NS), which are connected to New England by Maritimes and Northeast Pipeline, production has been declining with Encana permanently shutting down production at Deep Panuke and continued declines at Sable Island. While BTU Analytics estimates that total NB and NS average annual demand is only around 130 MMcf/d, there could be meaningful impacts for New England pricing this winter as existing bottlenecks are stressed harder.

At the US / Canada border, Maritimes & Northeast connects with Brunswick pipeline, which delivers gas from the Canaport LNG import terminal in Canada to the border. Historically, production in NB and NS was greater than local demand, so excess production plus Canaport LNG deliveries were transported into the US to serve New England. However, as production and Canaport LNG deliveries have declined, flows at the border have now flipped, with gas moving into Canada from the US, and some Canaport volumes are staying in Canada to serve local demand.

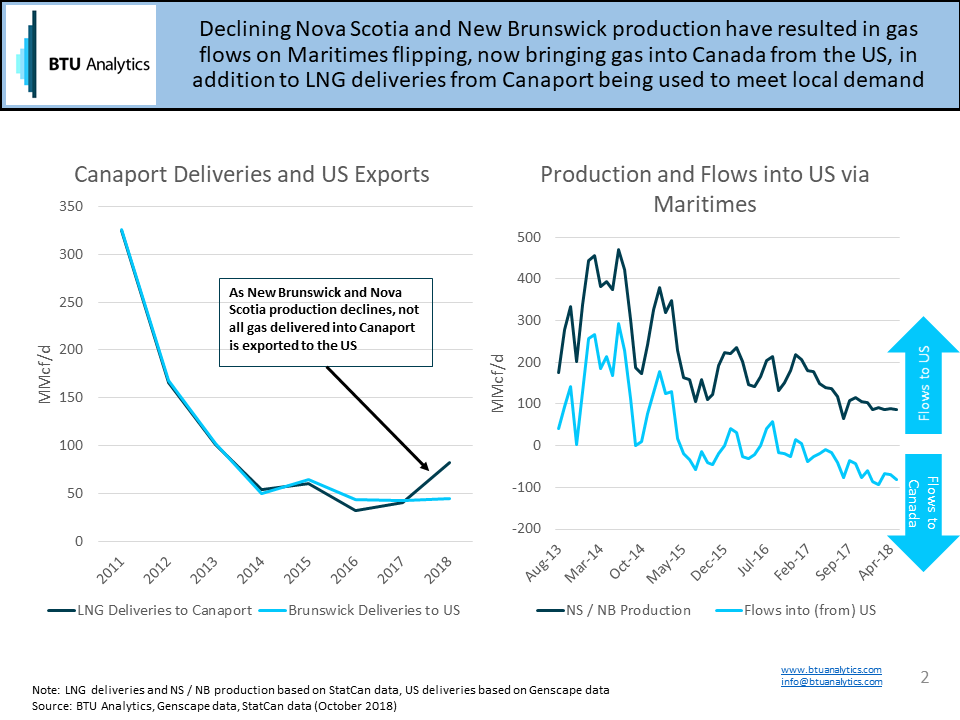

So far in 2018, deliveries to Canaport are nearly double 2017 volumes while exports to the US are flat, implying that more gas is staying in Canada to serve local demand (chart on left below). However, even with the incremental supply from higher LNG deliveries in 2018, production declines have resulted in more gas moving into Canada from the US (chart on right below), facilitated by increased deliveries from Portland Gas Transmission (chart on map above). Total NS and NB production was around 87 MMcf/d in May, with 81 MMcf/d coming from Sable Island. Like Deep Panuke, Sable Island production is also moving towards abandonment as ExxonMobil commenced plugging and abandonment activities for 21 production wells in 2017, and preparatory activities to abandon all offshore platforms are underway. Further production declines would likely result in greater price volatility for this and future winters as scarcity pricing and fuel switching economics could come into play more often in New England.

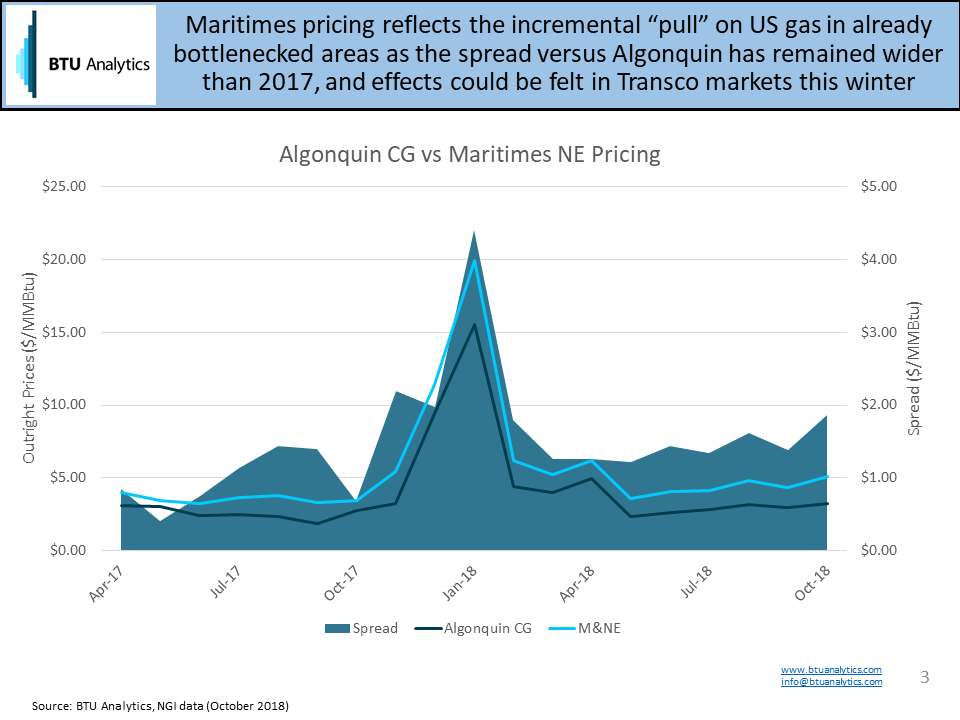

We are watching these dynamics because Maritimes delivers gas to Algonquin and Tennessee in Massachusetts, especially during peak winter months. From December 2017 through February 2018, total deliveries from Maritimes to those two pipes was around 120 MMcf/d. When Sable Island production declines further, absent additional LNG deliveries, Maritimes prices would have to incentivize gas away from Algonquin markets where prices breached $100/MMBtu during the ‘Bomb Cyclone’ in January 2018. Sable Island’s current production of about 80 MMcf/d is equal to 67% of gas delivered into Massachusetts during peak winter months last year, so the declines could be material for pricing. So far in 2018, the spread between Maritimes and Algonquin has outpaced 2017 levels even with increased gas from Portland Gas Transmission, likely reflecting the additional pull on New England gas.

The ripple effect for hubs “at the end of the pipe” could be that other bottlenecked markets, such as Transco Z6 NY, Transco Z6 Non-NY, and Iroquois Z2, enter a cascading price competition for limited volume. Hubs with limited optionality and infrastructure bottlenecks could reach scarcity pricing more often, resulting in volatile prices and subsequent winters. Beyond these dynamics, prices will also be influenced by the pace of production growth in Northeast Pennsylvania and the impact of Atlantic Sunrise. Stay abreast of our latest views on Appalachia and Northeast pricing dynamics with the Northeast Gas Outlook.