With 2019 in the rearview mirror, the natural gas industry turns its focus to 2020, where an abnormally warm winter has placed even more downward pressure on US gas prices. As Henry Hub prices drop below $2 this morning, the need for increased external demand for natural gas, be it through LNG exports or exports to Mexico, is even more clear. While exports to Mexico increased to over 5.5 Bcf/d in 2019, utilization of cross-border capacity remains low due to constraints further downstream. However, with uncertainty surrounding domestic gas production in Mexico, and key infrastructure set to come online this year, natural gas exports to Mexico could realize some upside in 2020.

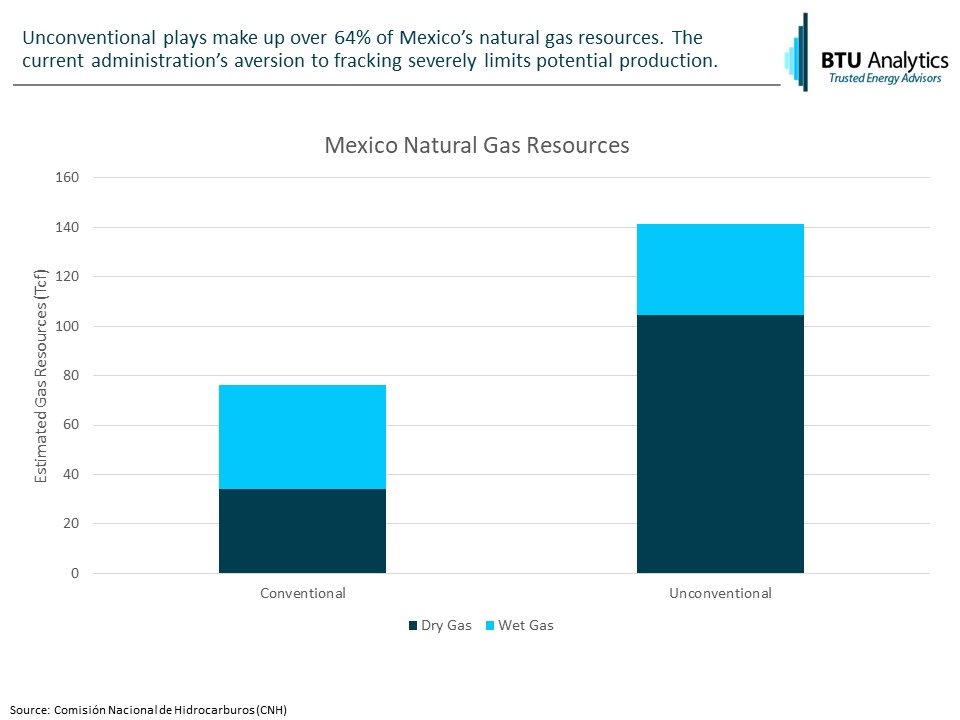

After being elected in 2018, the Lopez Obrador administration gave mixed signals about the path forward for the natural gas industry in Mexico. While the president has mandated that Pemex reverse the decline in domestic gas production, he is adamantly against using fracking to access Mexico’s unconventional resources. With an estimated 100 Tcf of dry gas trapped in unconventional plays, the administration’s aversion to fracking severely handicaps domestic production. In addition, Mexico suspended auctions for new oil and gas contracts, denying private capital and technical expertise a way to develop untapped resource potential. As a result, Mexico’s main hope for increased domestic production is likely tied to the development of the Ixachi field in Veracruz, Mexico. As part of the Pemex 2019-2023 business plan, Pemex has allocated more than $1 billion of capital expenditures to developing the field. By the end of 2020, Pemex expects production to reach 400 MMcf/d, a significant increase from current production of ~100 MMcf/d.

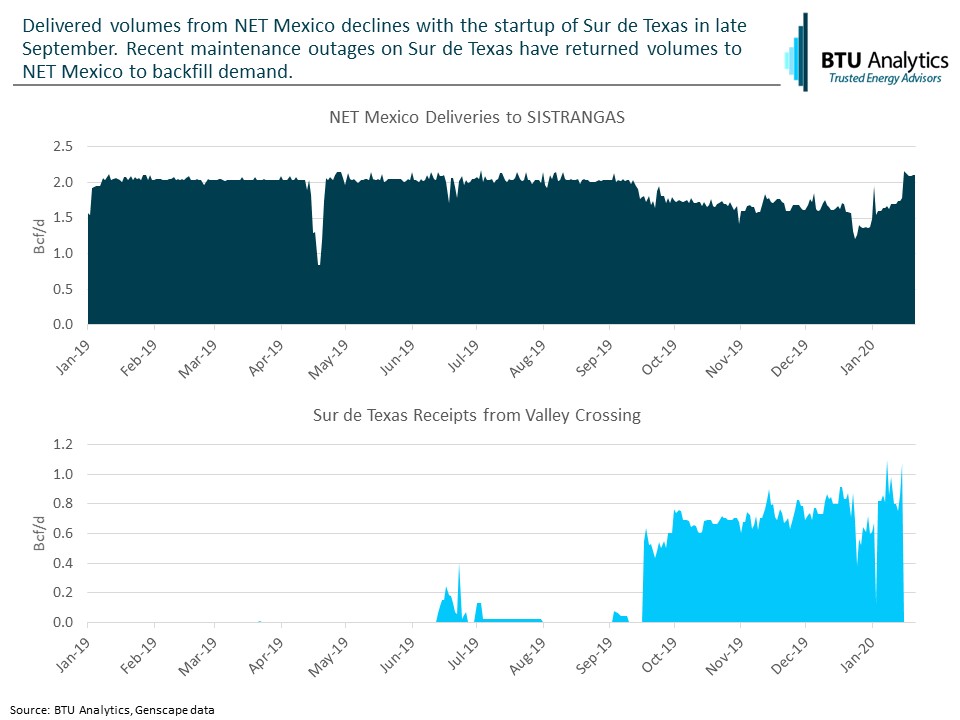

Even with a hypothetical increase in domestic production, Mexico will still rely heavily on pipeline imports from the US to meet growing demand. However, the ability for this demand to be met will depend on some key infrastructure projects entering service in 2020. Last year, the Sur de Texas pipeline out of South Texas entered service in September with flows quickly ramping up to 800 MMcf/d. However, after Sur de Texas entered service in September, flows on the NET Mexico pipeline declined by ~300 MMcf/d as limited demand in Northeast Mexico was met with gas from the new pipeline. If new infrastructure can allow Sur de Texas to move volumes further south, volumes on NET Mexico could return and backfill the remaining demand.

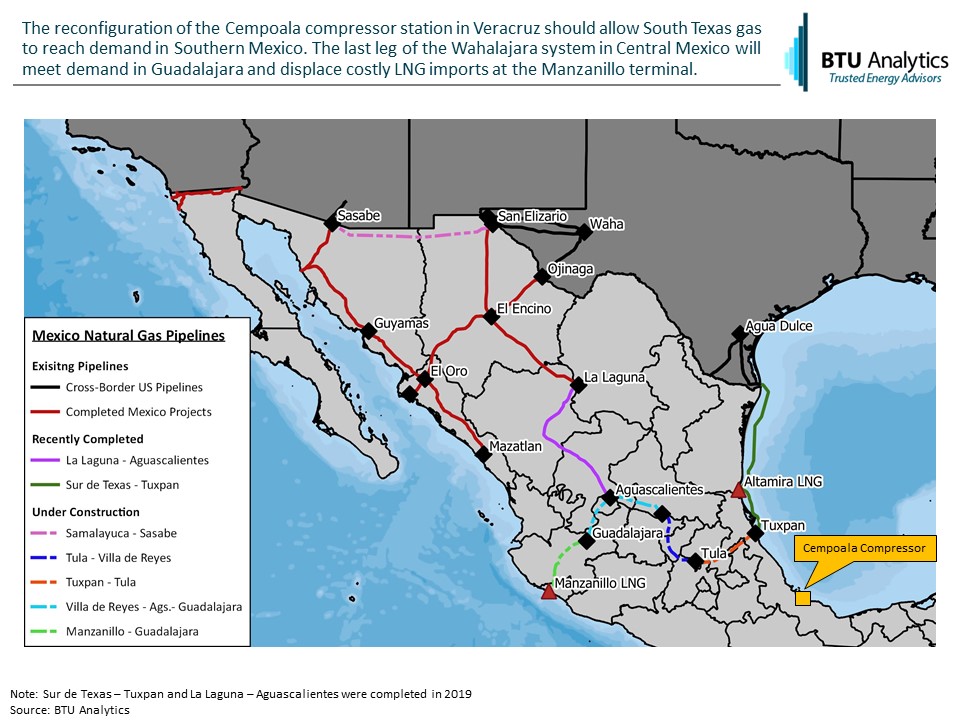

Although the Tuxpan – Tula and Tula – Villa de Reyes projects remain delayed, the reconfiguration of the Cempoala compressor station would allow increased incremental volumes out of South Texas. Once completed, the compressor station will allow natural gas to move down the Gulf Coast to meet demand in the Yucatan peninsula, via a planned interconnection with the Mayakan pipeline, where inadequate gas supply has caused rolling blackouts in the region. The compressor station will also allow gas from Sur de Texas to flow on the Monte Grande interconnect and connect with the SISTRANGAS national pipeline system.

Out of West Texas, the final leg of Fermaca’s “Wahalajara” system is due to be completed in the first quarter of 2020 when the Villa de Reyes – Aguascalientes – Guadalajara pipeline enters service. As we detailed last April, this pipeline will connect with the recently completed La Laguna – Aguascalientes pipeline to potentially provide relief for stranded Permian gas. The project will not only allow more gas to meet demand in Guadalajara but also allow for the reversal of the Manzanillo – Guadalajara pipeline which could displace costly LNG imports to the Manzanillo terminal.

While BTU Analytics continues to be conservative in our forecast for Mexican exports, there is significant upside potential once Mexico’s natural gas infrastructure is in place. However, as we’ve seen with past projects, successful integration of infrastructure can be an elusive target south of the border. For more on Mexican exports and their impact on the US natural gas market, check out our Henry Hub Outlook.