Anticipation for Cheniere’s 1.44 Bcf/d Midship pipeline is building as the project plans to begin service later this year. Buoyed by oil prices, natural gas production in the SCOOP and STACK plays continued to increase in 2018. As a result, Oklahoma producers are counting on Midship’s capacity to ease pipeline constraints. However, downstream of Midship, spare capacity on MEP and Gulf Crossing has diminished. The start of Midship will no longer guarantee smooth sailing for SCOOP and STACK producers.

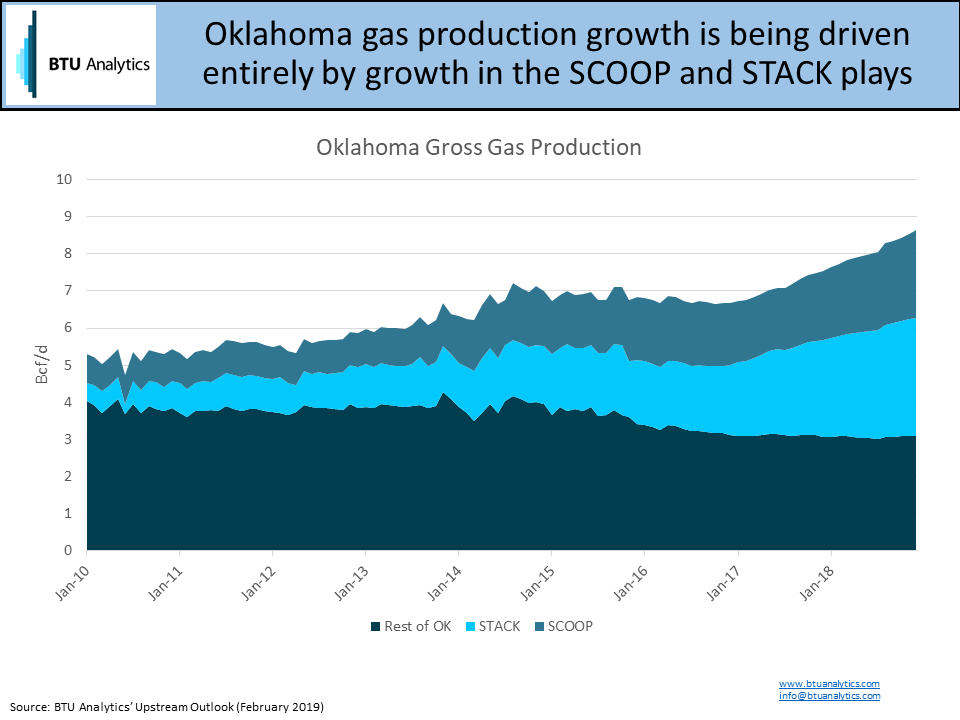

Oklahoma gross gas production at the end of 2018 climbed to 8.6 Bcf/d, up 1.1 Bcf/d year-over-year. Of that, over 60% came from SCOOP and STACK production areas. BTU Analytics expects this trend to continue. Future growth will come exclusively from the SCOOP and STACK while the rest of Oklahoma declines.

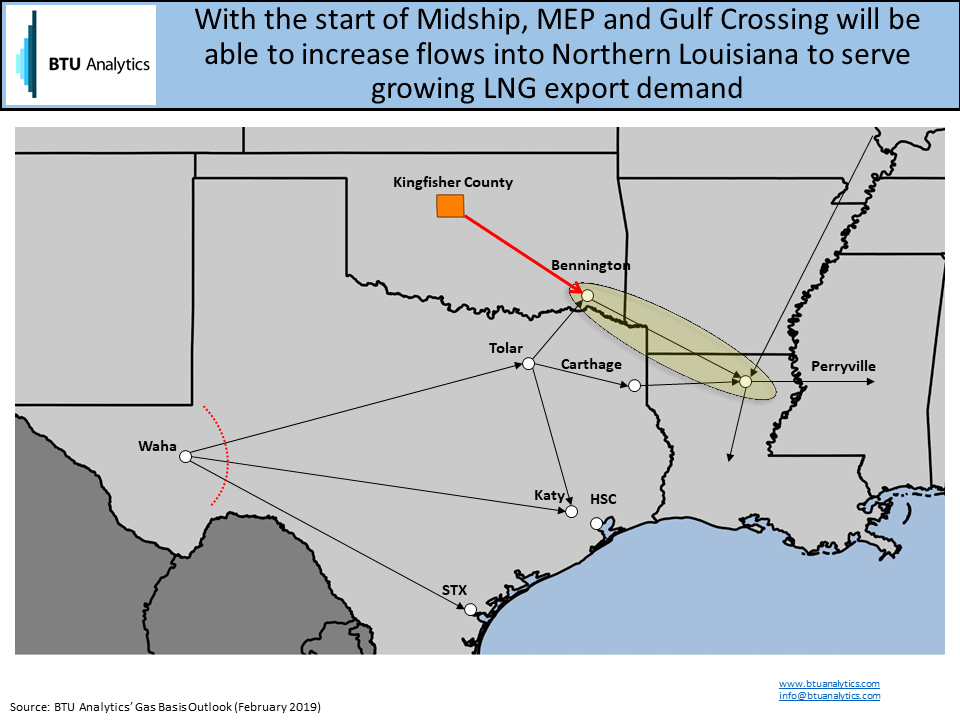

Midship Pipeline originates in Kingfisher County, Oklahoma, in the core of the STACK. At full capacity, Midship Pipeline transports up to 1.44 Bcf/d of gas south and east to Bennington, Oklahoma. At Bennington, Midship Pipeline interconnects with MEP and Gulf Crossing. Both pipelines then facilitate delivery to Southeast and Gulf Coast markets. Midship will alleviate some of the west to east constraints within Oklahoma. However, Midship pipeline may just push bottlenecks further downstream.

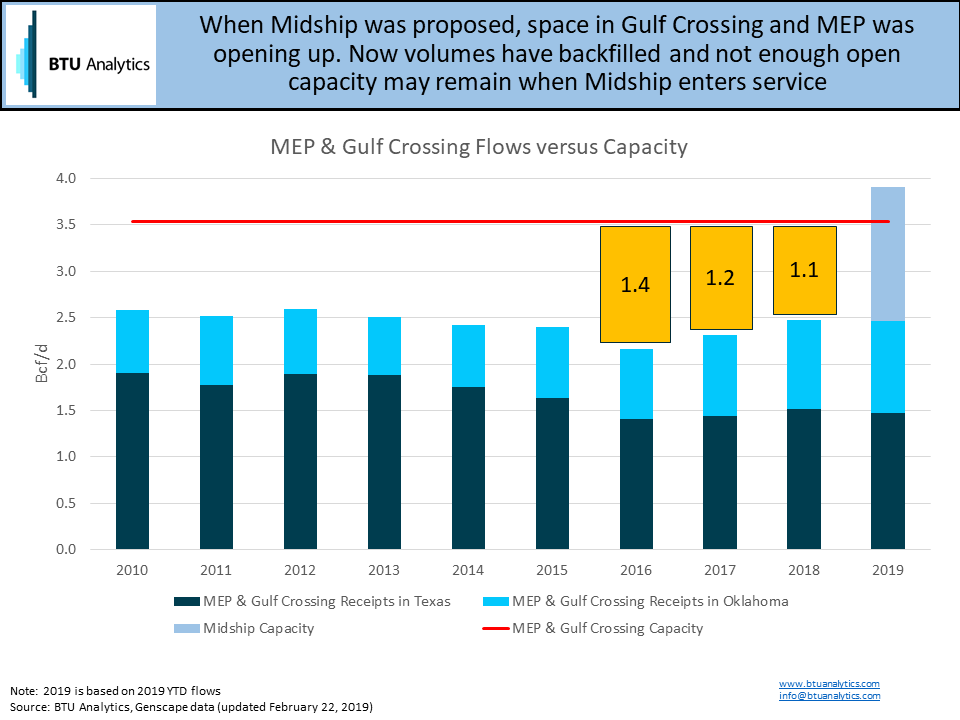

With ramping LNG exports and the potential of wave 2 LNG export terminal FIDs in 2019 on the horizon, demand for Oklahoma gas is expected to remain strong in the near future. Proposals for gas pipelines from Oklahoma to the Gulf have been in the works since at least 2014. Midship Pipeline was announced in early 2017 with 1.44 Bcf/d of capacity. In 2016, open capacity from Bennington to Perryville on MEP and Gulf Crossing totaled over 1.4 Bcf/d. However, since then, receipts on MEP and Gulf Crossing have grown, limiting the availability of capacity at Bennington. The reduction in space sets up a downstream bottleneck. In order to flow at maximum capacity, displacement of existing volumes will have to occur. In 2018, average receipts on MEP and Gulf Crossing totaled 2.5 Bcf/d, as illustrated in the chart below. The increase in volumes leaves just over 1.1 Bcf/d of open capacity on the two pipelines. As a result, Midship would not be able to deliver the full 1.44 Bcf/d of Midship capacity at the end of 2018.

This potential pipeline bottleneck may force displacement of existing flows. MEP & Gulf Crossing source volumes in Oklahoma that could be rerouted to Midship off of existing pipelines. However, if SCOOP and STACK continue to grow, volume must be displaced from receipts in East Texas. Texas receipts have grown as a result of growing Permian volumes displacing Barnett supplies to Gulf Crossing.

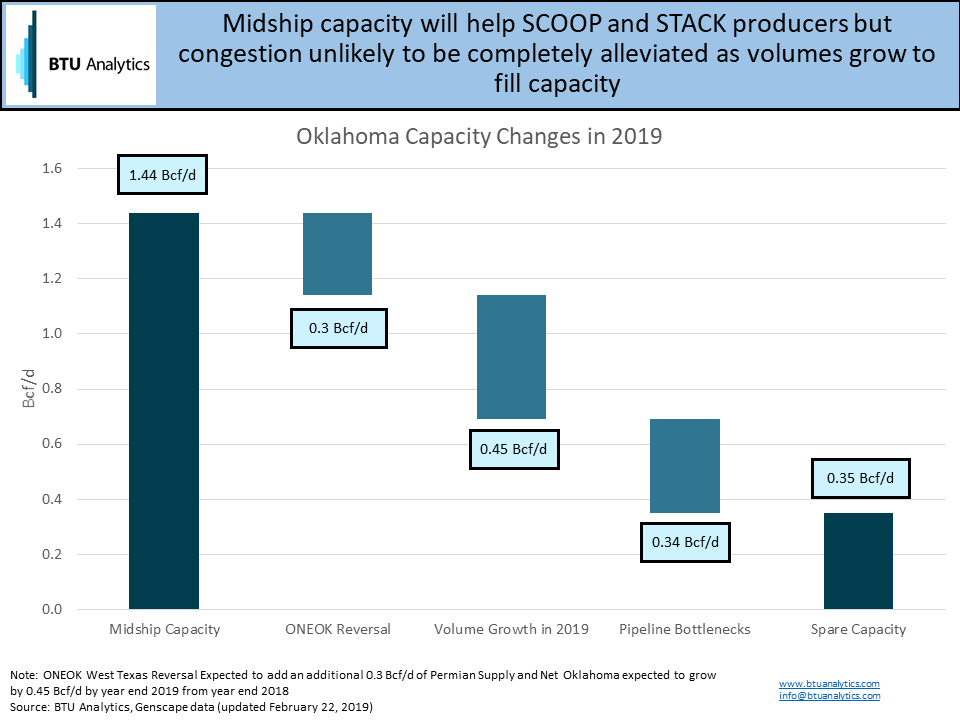

BTU Analytics forecasts an increase of 0.45 Bcf/d in Oklahoma gross gas production by year end 2019 vs year end 2018. Additionally, ONEOK’s reversal of the WesTex line in 2018 has resulted in flows of 0.15 Bcf/d of Permian gas into western Oklahoma. The line is expected to add an additional 0.3 Bcf/d of Permian supply to Oklahoma by the end of 2019. Growth in supply from the Permian and Oklahoma in 2019 will leave Midship with about 0.35 Bcf/d of new spare capacity for SCOOP & STACK producers.

If drilling activity ramps up or Appalachian supply pressures divert gas from the Midwest, then the spare capacity will be quickly utilized. Therefore, expectations should be tempered on how much congestion will be alleviated by Midship Pipeline. For more on evolving gas market bottlenecks and basis impacts request a sample of our new Gas Basis Outlook service