The past month has been eerily quiet for news on Mountain Valley Pipeline and Atlantic Coast Pipeline. Earnings season yielded only slight transparency into the progress on the two major pipeline projects out of the Northeast. First, EQM (NYSE: EQM) announced a late 2019 start-up of Mountain Valley is now unlikely and a possible reroute of the pipeline may be necessary. Additionally, Dominion (NYSE: D) announced they expect to restart partial construction on Atlantic Coast Pipeline in the third quarter of 2019. Today’s Energy Market Commentary will focus on the updates provided by each company and two possible rerouting options for Mountain Valley pipeline.

Both Mountain Valley Pipeline and Atlantic Coast Pipeline currently lack authorization to cross the Appalachian Trail. The lack of authorization has prompted Mountain Valley to explore rerouting options and Atlantic Coast Pipeline is awaiting progress in the courts. The restart of partial construction on Atlantic coast pipeline assumes a favorable ruling in the 4th Circuit Court of Appeals on their incidental take permit for endangered species. The graphic below from Dominion Energy’s Q1 2019 earnings call presentation provides a summary of the timeline.

In December, the 4th Circuit Court of Appeals argued that the Forest Service “abdicated its responsibility” to protect national forests in authorizing Atlantic Coast Pipeline to construct on Forest Service land and across the Appalachian Trail. Dominion expects to file an appeal of the 4th Circuit’s ruling to the Supreme Court this quarter. Full construction on Atlantic Coast is not expected to resume until a positive order is received from the Supreme Court (Dominion expects this in 2Q 2020).

Additionally, EQM says that “for all practical purposes” the 4th Circuit’s decision on Appalachian Trail crossing authorizations for both Mountain Valley and Atlantic Coast are ultimately intertwined and finds it unlikely that “the Forest Service would issue a permit without a resolution to the Appalachian Trail”. Additionally, EQM stated they are searching for solutions to cross the trail on either non-Forest Service land or private land. Also, EQM indicated a reroute is the last resort for Mountain Valley Pipeline. But what could the monetary impact be if EQM must follow the path of last resort, and reroutes the pipeline to cross the Appalachian Trail on private land?

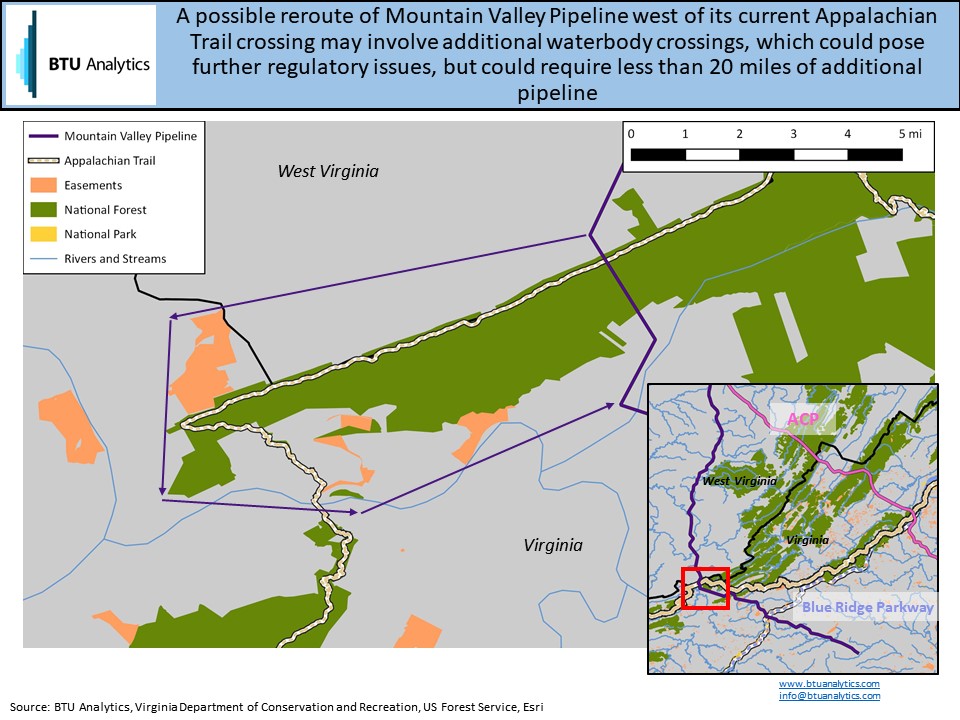

The maps in this Energy Market Commentary use geographic data from the Virginia Department of Conservation and Recreation and the United States Forest Service to show land ownership across the state of Virginia. It is possible that these maps are not entirely comprehensive. For this illustrative commentary, we assume that any land with no marked owner is private land. Using a visual analysis of these maps, we can approximate where EQM could reroute Mountain Valley, how long the reroute may be, and how much the reroute could potentially add to the project budget. The analysis assumes this potential reroutes are not already factored into the project budget.

Based on our visual analysis, Mountain Valley could reroute to the west of its current route across the Appalachian Trail. A western route would avoid crossing conservation easements and Forest Service land. Using our maps (and only straight lines), this reroute would add approximately 19 miles of pipeline. Based on Mountain Valley’s cost per mile of $15.1 million (covered in previous Energy Market Commentary posts here and here), a western reroute could add over $285 million to the project’s cost. This would bring the project’s total cost to $4.85 billion. The actual cost per mile of this reroute could vary significantly from this estimate based on final engineering plans and route selection. Though this reroute would avoid conservation easements and Forest Service land, it would add additional waterbody crossings based on our geographic data. Additionally, Mountain Valley still lacks a Nationwide 12 Permit from the Army Corps of Engineers, which authorizes waterbody crossings.

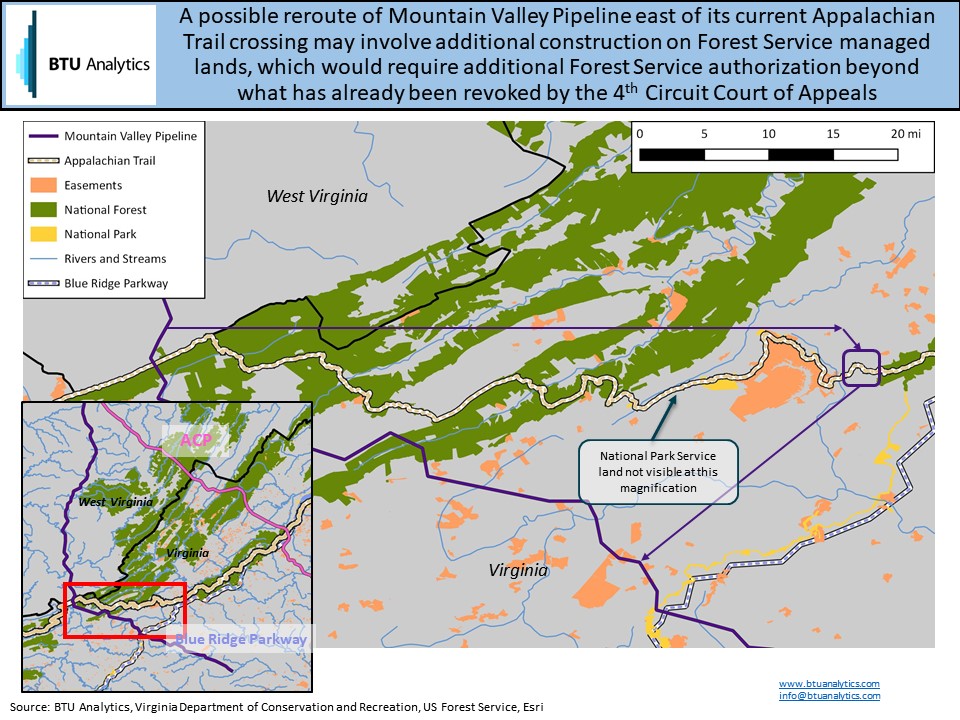

Additionally, a potential reroute to the east of the current Appalachian Trail crossing route appears to exist. However, this route crosses significant swaths of Forest Service land and involves additional water body crossings. We assume Mountain Valley would be unable to obtain authorization to construct on land protected by conservation easements. Thus, Mountain Valley Pipeline would route the pipeline to avoid conservation easements. Under the purple rectangle on the far right of the map below, there are a few sections of land that, according to our geographic data, are privately owned. These small sections could provide a route for Mountain Valley to cross the Appalachian Trail on private land although the overall route would necessitate additional construction on Forest Service land. This route, according to our visual analysis, would add approximately 72 miles of pipeline. Utilizing the project’s cost of $15.1 million per mile, an eastern reroute could add over $1 billion to the project’s cost. Resulting in the total project cost exceeding $5.6 billion.

Given the additional Forest Service crossings, water body crossings, and significant cost increase of an eastern reroute, it is more likely that Mountain Valley would choose a western reroute of the project. The reroutes are only necessary to complete the pipeline should Mountain Valley Pipeline need to avoid its current crossing location of the Appalachian Trail. Dominion expects to receive a positive ruling from the Supreme Court on their Appalachian Trail crossing in 2Q 2020. This would set precedent for Mountain Valley for a successful authorization of their Appalachian Trail crossing as well. Until progress on the regulatory process occurs on both projects, additional delays may be likely. BTU Analytics provides our view on the risk to in-service dates for natural gas infrastructure in the Northeast and beyond, as well as the potential impact of new pipeline projects on basis pricing in our Gas Basis Outlook.