Winter is coming. Not the one from the end of Game of Thrones, but one that will play a key role in the outlook for the US gas market in 2021. While US storage is projected to exceed 4 Tcf by the end of this summer, declining gas production and rebounding demand could leave the market short in 2021. Depending on how heating demand and LNG exports materialize, US storage could be severely diminished by the end of the winter, leading to an upside for Henry Hub pricing.

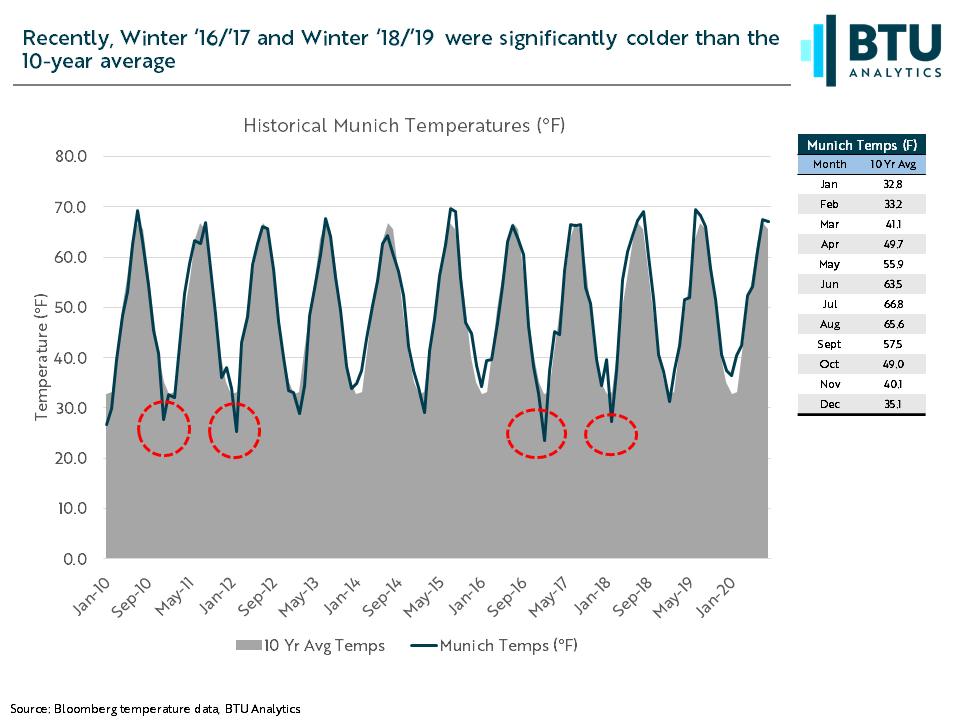

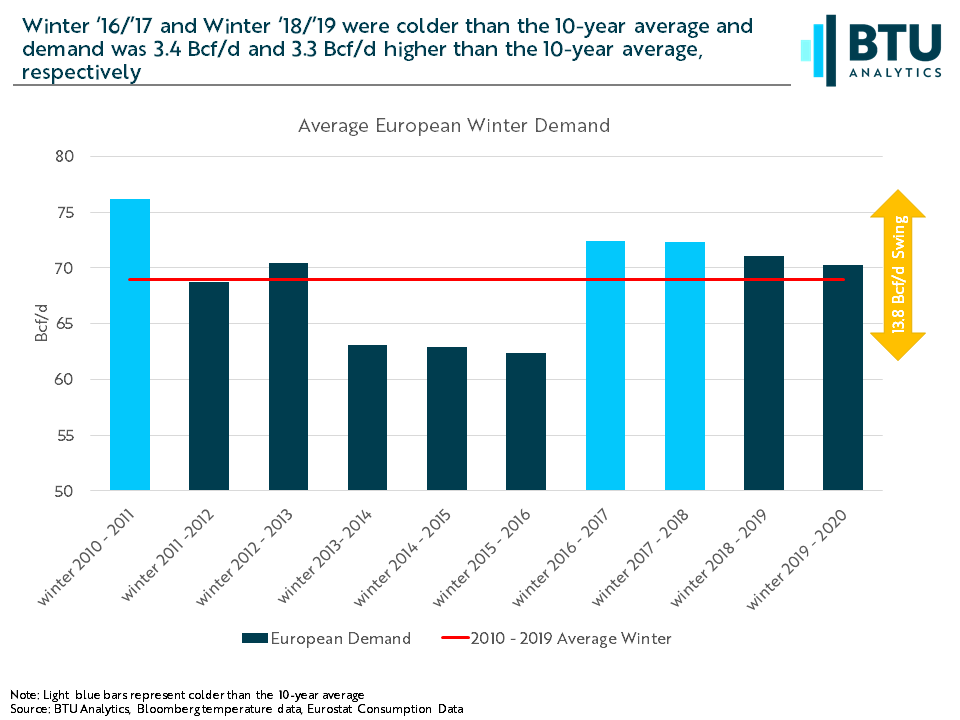

One of the key drivers for US LNG this winter will be the level of LNG exports that can be absorbed by Europe. While COVID-19 related disruptions remain a concern, the driving factor for European winter demand will be the weather. As it does in the US, winter demand in Europe shows a strong correlation with winter temperatures. Using Munich, Germany, as a proxy for continental Europe, the winters of 2016 and 2017 saw temperatures drop well below the 10-year average. This was reflected in European winter demand with 2016 and 2017 demand averaging 3.3 Bcf/d higher than the 10-year average. This is reflected in the charts below.

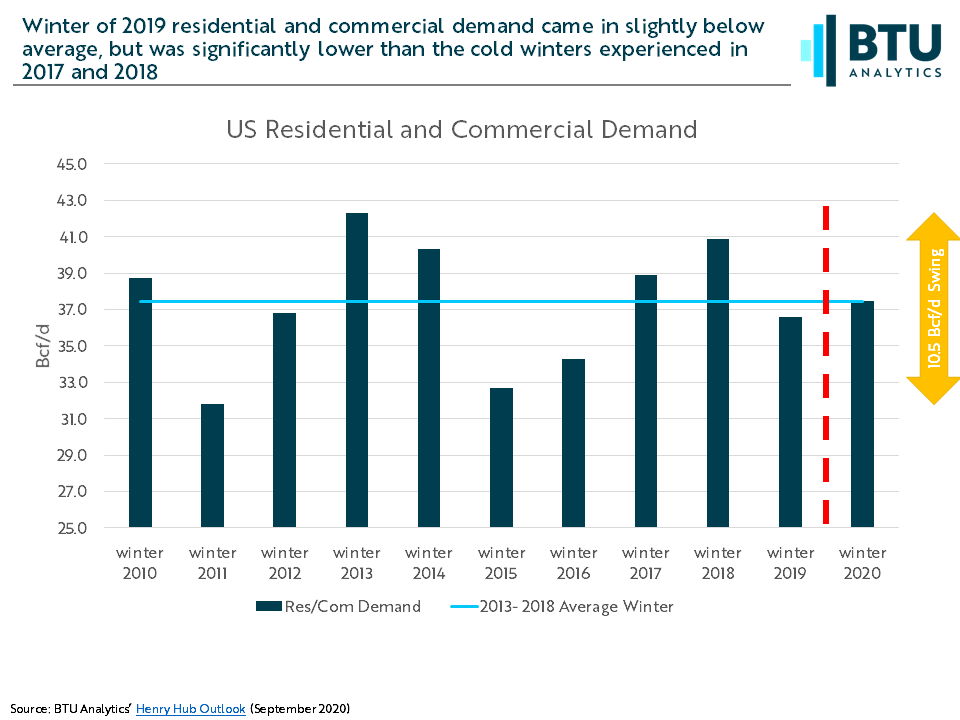

However, while LNG exports will be a focus for many this winter, US residential heating demand will be far more impactful on the end of winter storage numbers. Even under a best-case scenario, LNG would be unlikely to add more than 2 Bcf/d of demand above the levels reached last winter. On the other hand, cold winter like the US saw in winter of 2013 could add over 6 Bcf/d compared to winter 2019. Yet there is also a significant downside if the US experiences a warmer than average winter. Just in the last five years, the US has seen winter demand fall as low as 32.7 Bcf/d, 4 Bcf/d lower than 2019.

One benefit of diminished inventory levels would be higher gas prices incentivizing drilling in gas plays outside of the Haynesville and Marcellus/Utica. Over the past decade, winters that ended with storage below 2 Tcf saw the 12-month NYMEX strip average $0.81/MMBtu higher than winters that finished above that mark. While the current Henry Hub strip can’t support sustained drilling activity in ancillary gas plays, a cold winter combined with strong LNG exports could lend strength not just to cash markets but also to the forward market, providing hedging and growth opportunities for producers.

BTU Analytics examined the different end of winter storage scenarios in our latest Upstream Outlook providing a detailed analysis of storage, Henry Hub pricing, and its impact on US gas producers. BTU Analytics also provides monthly updates on US LNG, winter demand expectations, and Henry Hub pricing as part of our Henry Hub Outlook.