Given the state of natural gas supply in the US, a mild winter this year would have far reaching ramifications into the natural gas storage outlook over the next year. Unfortunately, weather has not quite cooperated and we are coming out of one of the warmest Decembers on record at the same time US production hit record levels. Since we are halfway through winter, what would it take for the market to get back on track and get back to 5-year average storage inventory by the end of the season?

Today, after 11 weeks of winter or about half of the season, storage inventories are sitting just over 3.14 Tcf. Not too far off from the five-year average of 3.09 Tcf. However, where we are today has been driven by a combination of factors: foremost US natural gas production has continued to climb hitting record levels in December (BTU estimates December 2019 dry production at 95.9 Bcf/d), meaning that demand must be more robust than in the past to see the same amount of storage withdrawals.

The more apparent reason, especially for anyone who has stepped outside over the past few weeks, is weather. New York and Chicago averaged 43 and 41 degrees Fahrenheit in the last week of December, respectively. While still chilly for many, those temperatures are a far cry from the respective average temperatures of 37 and 27.

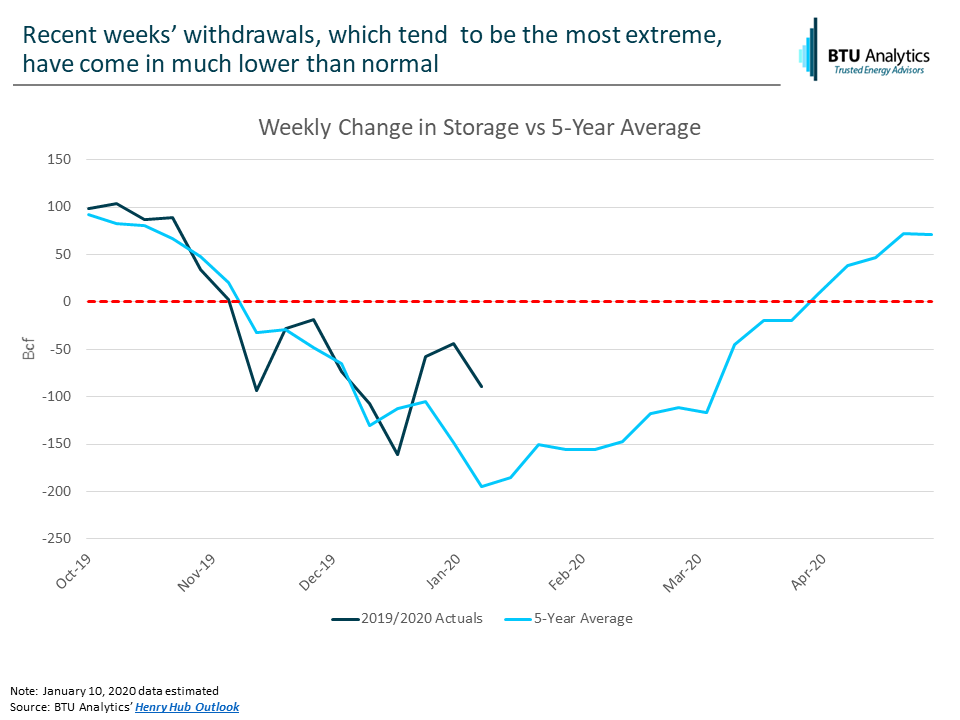

So, what does this mean for storage? The graphic below shows how storage withdrawals have fared this year against the five-year average. Withdrawals bounced around the five-year average for the first month or so of winter, however recent withdrawals, which tend to be the largest of the season, have been hammered by record production and warm weather.

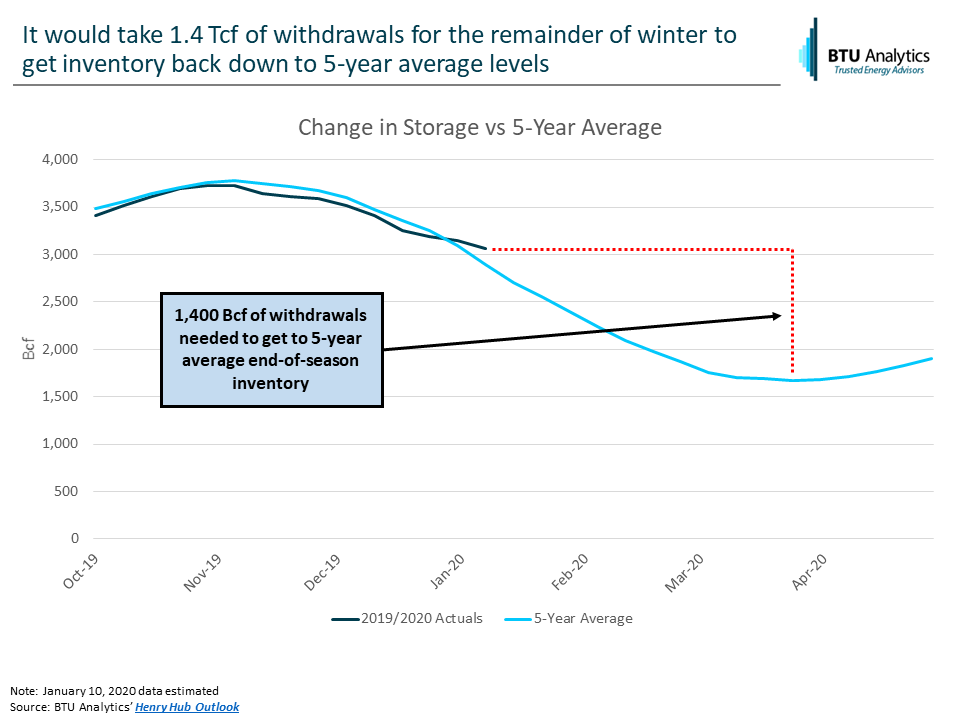

Looking forward to end-of-season inventory, what would it take for storage to get back on track? The graphic below shows total inventory today versus the typical 1.67 Tcf end-of-season inventory. If the market is to end the season at the five-year average, that would require an additional 1.4 Tcf of withdrawals in the remaining eleven or so weeks of winter.

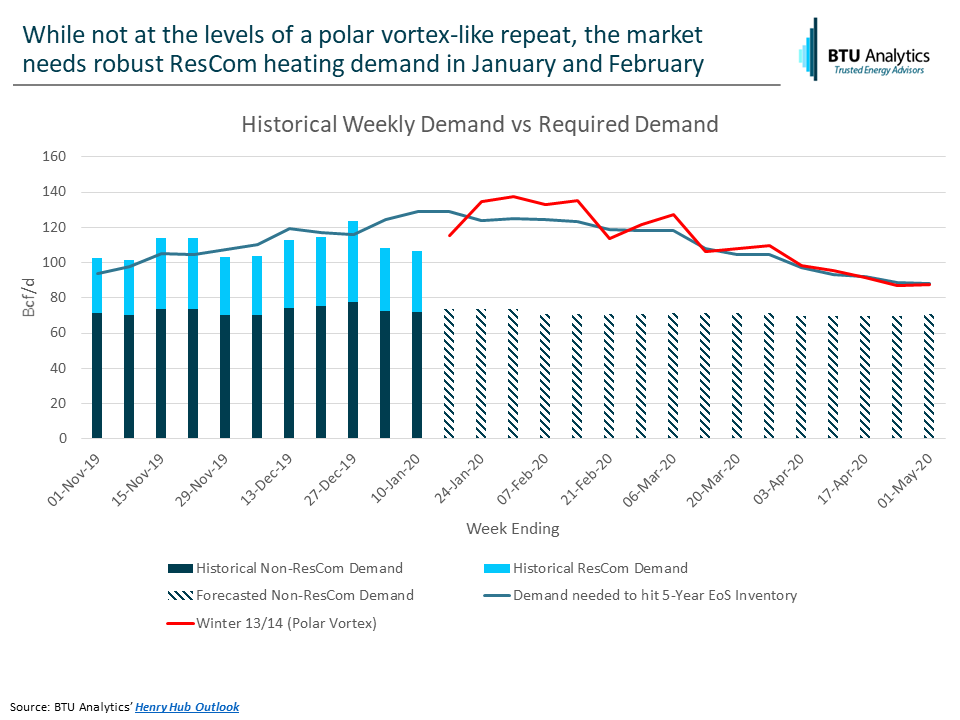

Is that a reasonable withdrawal for the rest of winter? To figure that out I layered in BTU Analytics’ supply outlook from our Upstream Outlook (which has production beginning to roll over this winter), then took our demand outlook from the Henry Hub Outlook for demand fundamentals that are not as sensitive to cold temperatures (I included power demand here). As with most winters, that leaves the swing demand in Residential and Commercial (ResCom) heating demand. The graphic below shows how demand this winter would have to shake out to get end the season at the five-year average.

For perspective, I added the demand we saw during one of the harshest winters in recent memory, winter 2013/2014 polar vortex. We’re not at the point yet when we would need a repeat of polar vortex-like temperatures. However, every day of tepid demand that passes the above solution becomes more extreme.

While how winter plays out is obviously on many peoples’ minds, the ramifications will be felt far into 2020. Every day that passes it becomes more likely we will not see inventory levels get back down to the 5-year average, so what will that mean for pricing? Will Henry continue to remain in the low $2.00 this summer or will new LNG demand lift prices? See our Henry Hub Outlook for BTU’s natural gas storage outlook and NYMEX view and the Gas Basis Outlook for the regional drivers and implications to basis pricing around the country.