As many of our followers know, BTU Analytics has been analyzing Northeast supply and transport balances for a long while. In 2015, as low commodity prices have forced more capital constraints on market participants, we wrote about some of these challenges in our natural gas market report released in August called ‘A Firm Dilemma’. Currently, many Appalachian-focused E&Ps are releasing slides in their investor decks detailing their firm transportation (FT) portfolios. As a result, we decided it would be good opportunity to review the history of basis spreads and the evolution of different phases of Northeast pipeline development and the various costs to reach downstream markets in context of producers’ reported costs to market.

The phases of development can be broken down into three distinct time periods:

- 2008-2010 Displacement (whether physical or nominated backhaul) on major trunk-lines that created new null points (bi-directional flow) on pipelines like Tennessee Gas Pipeline, Transco and TETCO inside the Northeast region

- 2011-2014 Direct Long Haul Reversals on traditional long-haul pipelines (CGT, TGP, Transco, TETCO) that historically served Northeast demand to take gas back to the Gulf

- 2015-2018 Greenfield and Indirect Reversals of long-haul pipelines adjacent to the Northeast – REX to NGPL, REX to ANR, REX to TGT, Atlantic Coast Pipeline, Mountain Valley Pipeline, Rover to Trunkline, Nexus to Dawn, Constitution, Northeast Energy Direct

For many E&Ps, decisions around FT depend on their operations team’s ability to balance and understand the deltas between their costs, risk appetite, and where fundamentals and spreads will be in the future.

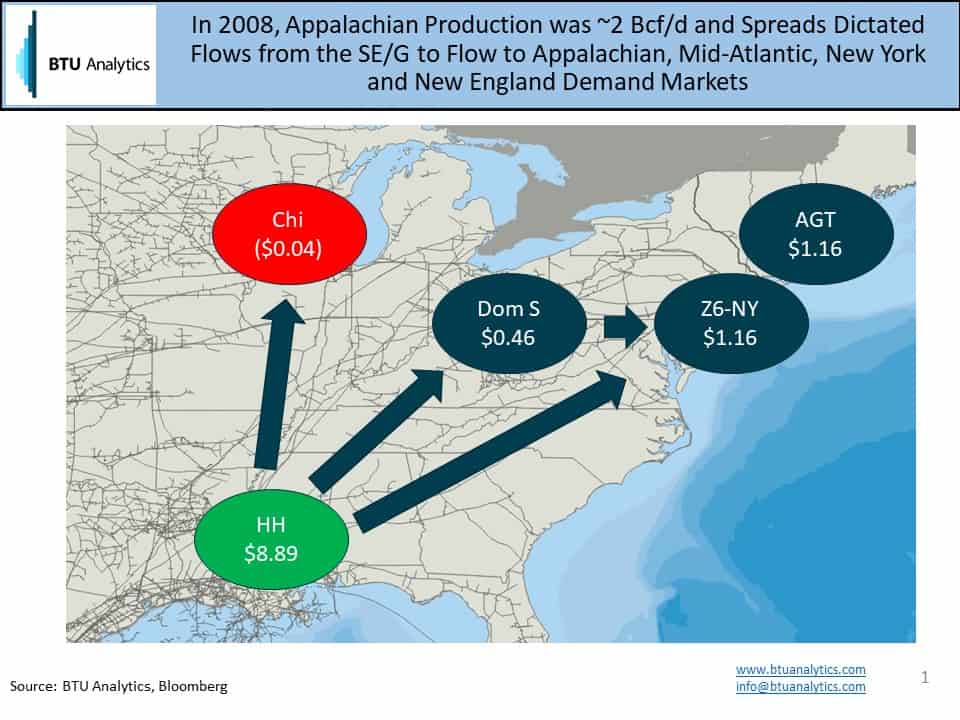

In 2008, average natural gas spreads followed decades old gas pipeline flow patterns of moving gas from the Southeast to the Northeast. Producers began flocking from the midstream-constrained and discounted markets of the Rockies, Oklahoma, and Texas to the “Premium Northeast” where they could sell gas on a spot basis into the Dominion South market for a $0.46/MMbtu premium to Henry Hub.

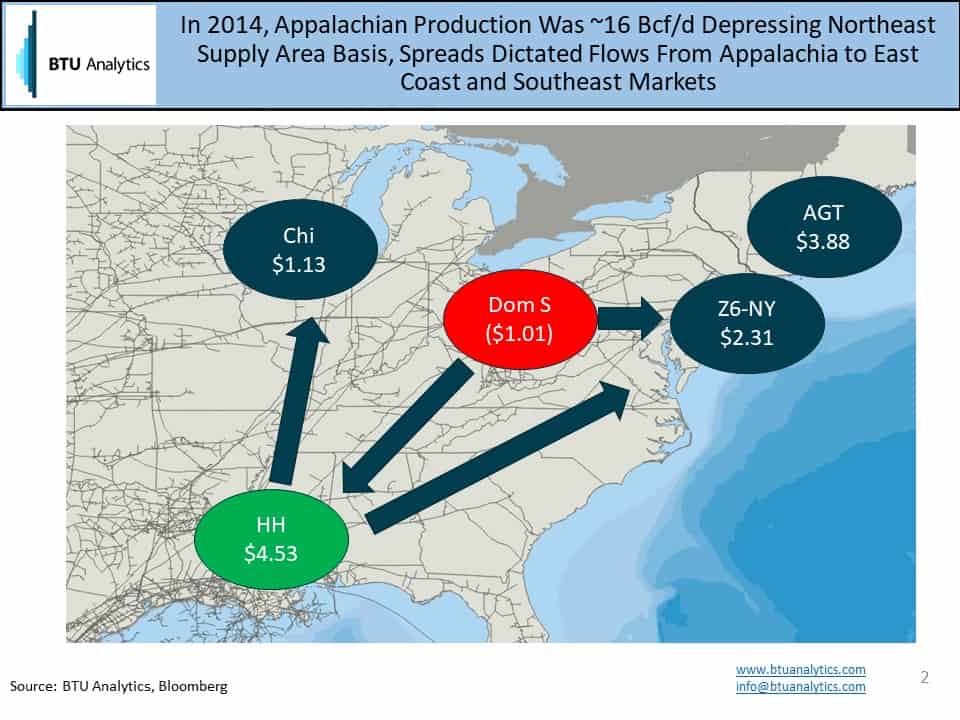

However, in 2008, some Northeast producers were already starting to evaluate and execute firm back-haul contracts to Louisiana to reach Henry Hub at rates that ranged from $0.25 to $0.40/MMbtu meaning they were contemplating a close to flat Henry Hub realized price when a producer selling only into the local markets was receiving a premium to Henry Hub. Tennessee Gas Pipeline and TETCO were some of the early movers to offer these rates and created “null” points in their systems allowing for bi-directional flow for producers. For other Appalachian E&Ps, at the time, these deals seemed laughable. In retrospect, they were clearly bargains as Dominion South prices in 2014 and 2015 have been more than $1/MMbtu behind Henry Hub driving commitments in greenfield pipelines that have tariff rates in excess of $0.70/MMbtu for Mountain Valley Pipeline and $0.80 for Rover pipeline

Based on previous FT rates, the assumption would be seeing reported producer rates now that are higher, because of the wider spreads (seen below) and greenfield pipeline developments such as Rover and Mountain Valley pulling average rates higher for producers. However, we are seeing a number of recently reported average firm transport rates through 2018 of anywhere from $0.28 to $0.60/MMbtu for producers like CNX, RRC, AR, COG, ECR to name a few. Why such a large range of “cost to market” for producers accessing similar infrastructure? Why are some producers reporting that their expected average cost of transport in 2018 has actually declined when new capacity has only become more expensive? Did some producers enter the market for capacity early and thus secure the cheapest capacity or do some producers more accurately reflect their total costs to market then others?

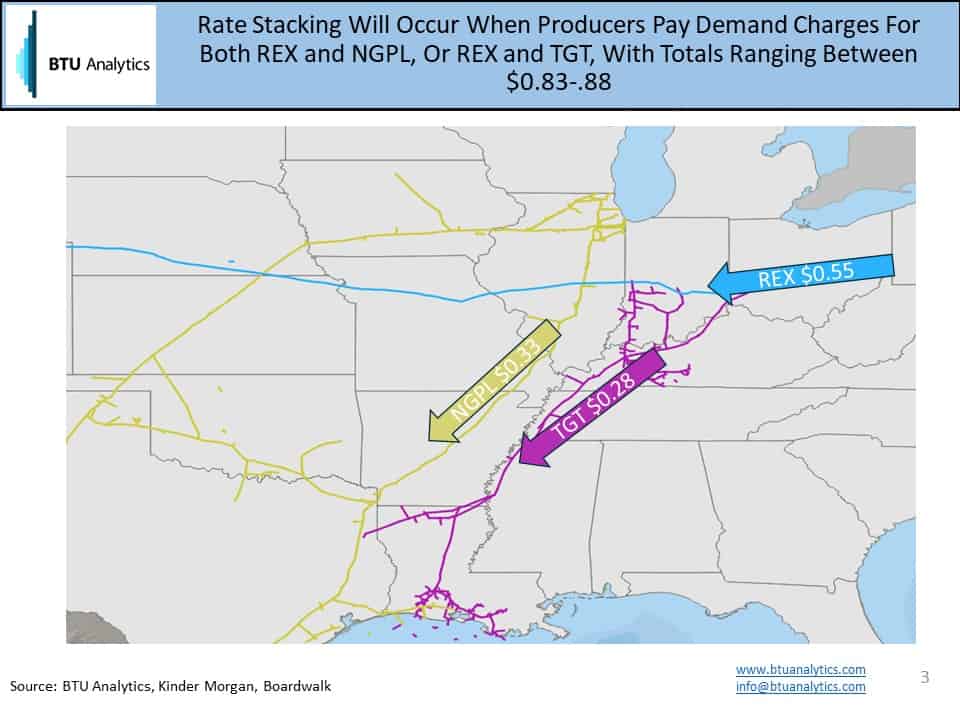

Our analysis of several of these producers indicates that it comes down to how producers account for firm transport contracts. If we look at Northeast pipeline tariffs for demand charges, we find posted rates of roughly $0.12 for Dominion (postage stamp), $0.28 for Texas Gas (Z1 to Z4), $0.32 for TETCO (M2 to ELA), $0.33 for NGPL (IL to LA), $0.44 for Transco (Z5 to Z1), $0.55 for REX (Z3 to Z3) and $0.55 for Tennessee (Z4 to Z1). These rates fall in line with some of the reported numbers we are seeing. If taken on face value, it also appears that Texas Gas is a lower priced transport option than say Tennessee.

For Appalachian E&Ps, a real distinction needs to be made between getting on one pipe to get to market vs. stacked rates (getting on 2 or 3 pipes to get to market). Some E&Ps are taking liberties in these calculations. If an E&P with gathering tied into Dominion wants to move gas to the Louisiana market on TETCO this would mean $0.12 for Dominion postage plus $0.32 for TETCO resulting in a total demand charge of $0.44 (assuming no negotiated rates) in addition, the producer would be liable for fuel charges of up to 6%. Thus, if a producer has a contract for 100,000 MMBtu/day with each pipeline it could report an average demand charge of just $0.22/MMBtu, while their netback price for 100,000 MMBtu/d of production would be Henry Hub – $0.44-(Dominion South x 6%).

Another example would be REX to NGPL, which have firm demand charges of $0.33 and $0.55 respectively. If an E&P contracts for equal capacity on both pipelines they could report an average demand charge of $0.44, when in fact the total cost to get to market is $0.88 since Northeast producers can not connect to pipelines like NGPL, ANR, and TGT directly with their gas.

As more E&P’s roll out new investor decks this fall, be sure to take a close look at how these companies are reporting the costs within their firm transportation portfolio. If you are interested in seeing BTU Analytics’ view on future basis and firm transportation costs, check out our new quarterly report focused on Northeast supply, demand and pricing dynamics.

Don’t forget, BTU Analytics is hosting a complimentary webinar covering our views on the impacts of DUCs, oil and gas production over the next 5 years, and how new data sets can strengthen your analysis. Register HERE