In 2016, the Permian Basin was the place to be more than ever as oil prices recovered and Wall Street rewarded those who have always been there and allowed non-Permian players to become ‘New Entrants’ to the Permian, driving frothy acreage valuations. The result is growing oil production forecasts along with expected associated gas production growth. While oil still has the benefit of midstream developments put into action pre-November 2014 providing ample oil takeaway, is Permian gas takeaway headed for tight times?

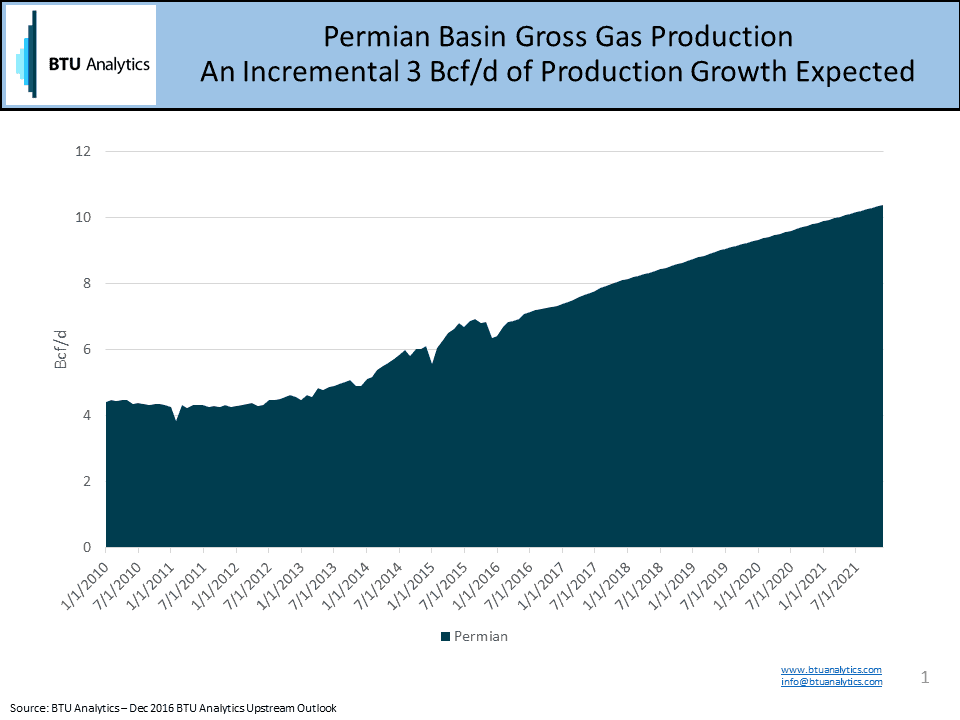

Below is the BTU Analytics’ gross gas production forecast for the Permian Basin (Delaware Basin, Central Platform and Midland Basin) showing production growing from roughly 7 Bcf/d today to over 10 Bcf/d by 2021. One common view we hear is associated gas growth takeaway is not a problem in the Permian thanks to the CFE and others backing an incremental 7 Bcf/d plus of new pipeline capacity to Mexico with many of those projects connecting to the Waha hub in West Texas.

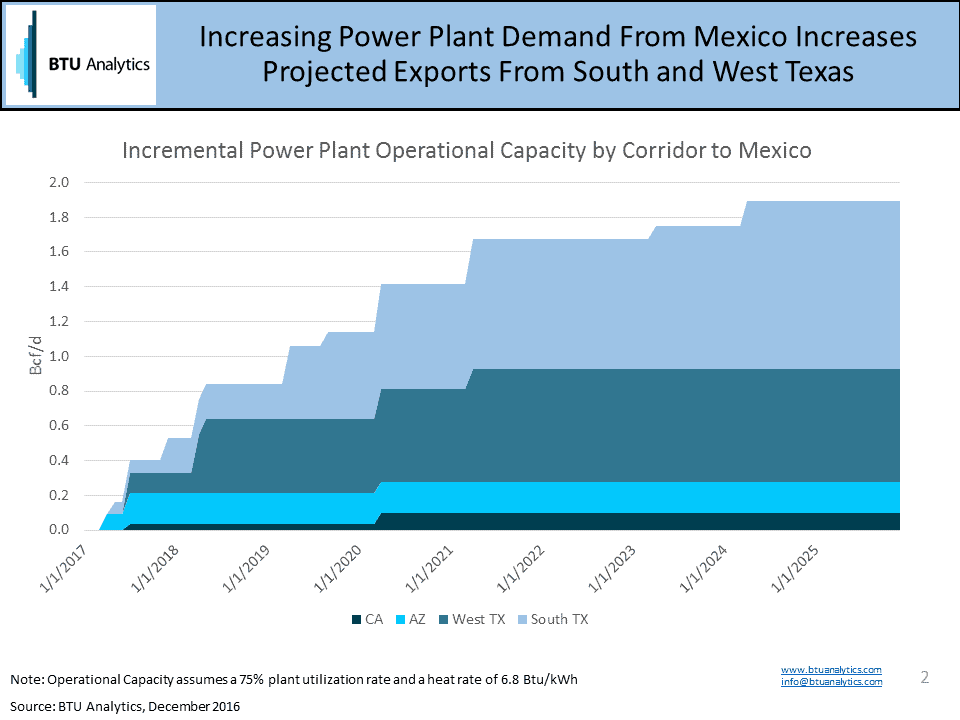

Here is the rub, when BTU Analytics looks at current Mexico export levels and looks at CFE power plant development through 2025, we see the potential for under utilization of pipes being built into Mexico. Current total US gas exports to Mexico are approximately 3.4 Bcf/d 2016 YTD while capacity is about 5.6 Bcf/d. Planned US export pipes to Mexico are expected to drive capacity to over 12.5 Bcf/d by 2021. However, BTU Analytics’ view is that these pipes are being built for peak days and average annual utilization less the 50%. Further, BTU Analytics tracks Mexico exports by 4 corridors: California, Arizona, West Texas and South Texas. In the Permian, BTU Analytics sees approximately 0.35 Bcf/d flowing to Mexico via West Texas today and only expects an additional 0.5 Bcf/d of power plant demand growth through the West Texas corridor – see chart below.

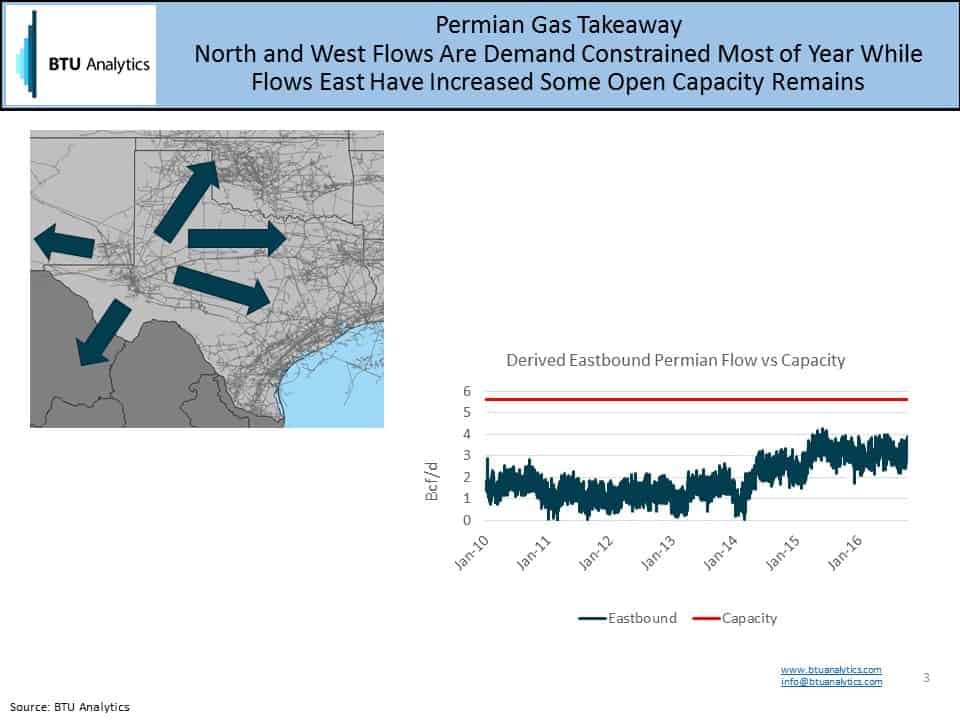

When we look at gas flowing out of the Permian today, the challenge is most of the year gas flowing West to California and North to the Upper Midwest is demand constrained, meaning the combination of lack of incremental seasonal demand (shoulder and summer seasons) and the competitiveness of other markets (i.e. Rockies and Canada) results in open capacity into these markets from the Permian. As addressed above, if export capacity to Mexico out of West Texas is overbuilt but demand is not there, it only leaves growth volumes of associated Permian gas to flow West-to-East across Texas on intrastate pipelines where flows are around 4 Bcf/d with capacity between 5 and 6 Bcf/d – see slide below.

Back to the problem – 3 Bcf/d of Permian incremental associated gas production growth by 2021 with limited outlets West to California or North to the Midwest (Competing with SCOOP & STACK & Rover). Mexico provides limited outlet to Waha, except for on peak power generation days in Mexico, and only 1 Bcf/d of open capacity on Texas intrastates flowing East. Despite all the pipes out of Waha, it looks like Permian associated gas may need a new pipe headed eastbound from Waha. For more information on BTU Analytics view on infrastructure development and production, request a sample of the BTU Analytics Upstream Outlook.