In the Marcellus and Utica, new pipelines inch closer and closer to reality. These long awaited pipes are expected to bring basis relief to the region and improve producer netbacks, but who will bear the costs of these new natural gas expansions? And what are the risks of taking firm transport (FT) on new projects?

Our new E&P Positioning Report helps to answer these questions. This is the fifth installment of our series surrounding the report. To get caught up, in our previous installments we have discussed operator Acreage Quality, Lowest Cost Producers, Growth Potential and Impacts of New Pipelines.

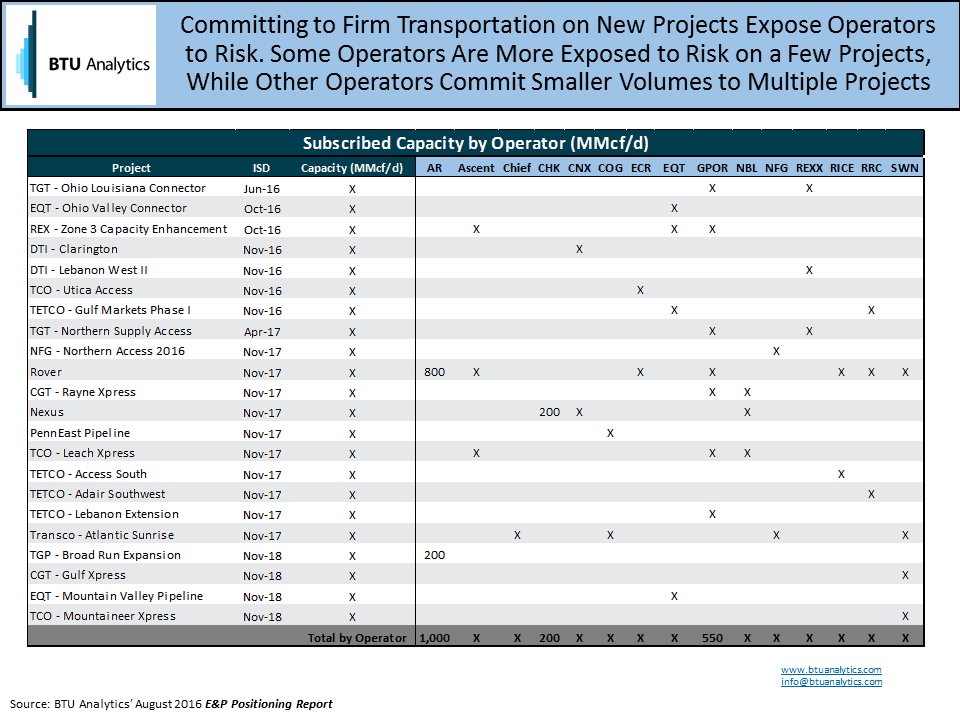

The following table shows which producers have firm transport on which projects. A complete version of operator commitments is available in BTU’s E&P Positioning Report. Below, the in-service dates (ISD) show official project ISDs and not the BTU Analytics’ risked in-service dates.

Operators can choose to employ a range of FT strategies. Operators such as Antero have committed a large amount of their upcoming commitments to Energy Transfer’s Rover Pipeline, while Gulfport has committed smaller volumes to multiple projects. Of course, to a certain degree, each operator’s individual circumstance can dictate their FT strategy, but also their outlook on new projects’ risks, as well as costs, will also influence their choices.

And there are plenty of risks to be concerned with. For the most part, the projects above are fully committed, with one exception with an impending ISD. Spectra’s Nexus Pipeline, which is due to be in service by the end of 2017, is only about 50% committed according to documents published in July. In a time where virtually every greenfield project faces significant opposition, not having support from shippers might be one obstacle too many. This would put growth strategies for producers who have commitments on NEXUS, like Chesapeake, Consol and Noble, at risk.

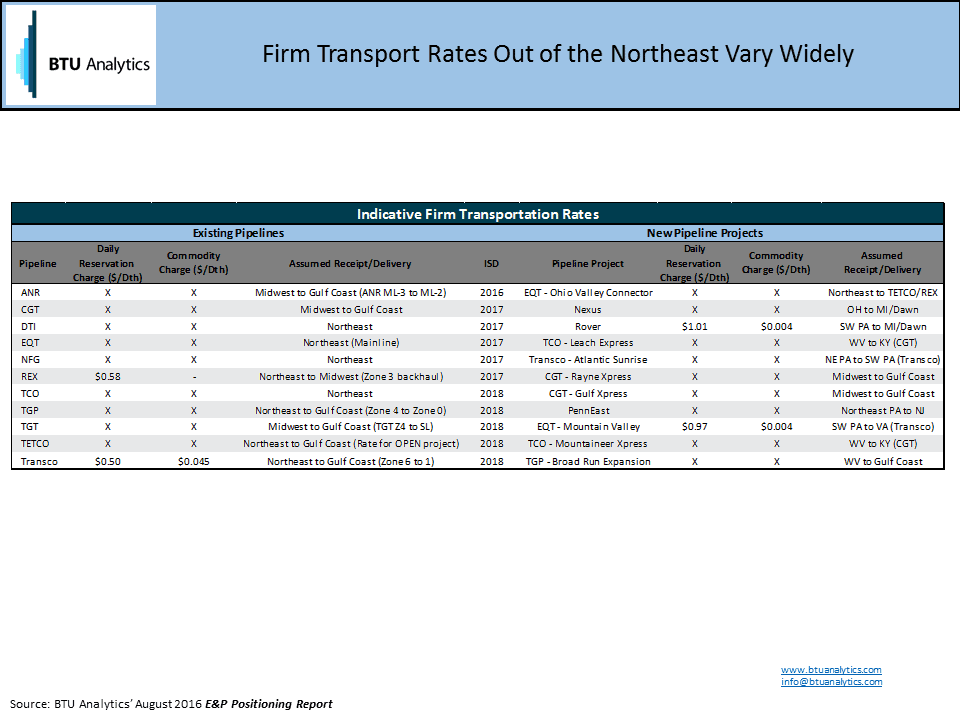

In addition to risks of delay and cancellation, cost is another factor that must be taken into account when comparing producers’ firm transportation strategies. Building new greenfield pipe is more expensive than simply adding compression to existing pipe and that increased cost gets passed on to shippers. Albeit the majority of the Northeast pipeline compression and reversal projects have already been completed. The table below shows selected pipeline rates for different existing and future routes.

Higher cost projects increase the risk to producer netbacks if those projects eventually bring online more capacity than is needed or can be filled. Open capacity brings with it collapsing spreads between receipt and delivery markets, reducing netbacks for operators who are saddled with a project’s expensive FT commitments. If a project were to bring open capacity to a region, then a strategy of holding little FT would be the most profitable, since an operator would be able to buy excess capacity on the release market and ship their gas without being burdened by reservation costs.

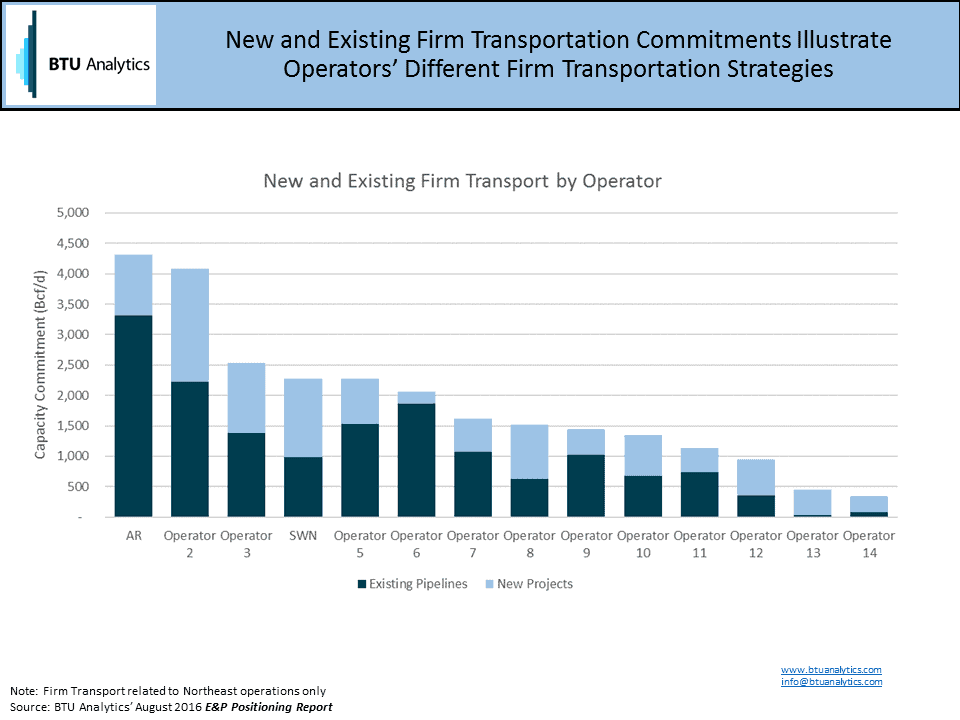

Beyond new projects, operators also have existing amounts of firm transport. The graphic below combines new and existing operator commitments relating to producers’ Northeast operations only.

Here, Antero and Southwestern illustrate diverging views on firm transport. While Southwestern produces more gas, Antero holds more firm transportation. This results in the need for Antero to grow production well beyond current levels to meet their commitments. Something which Antero is beginning to make strides to do with the purchase of Southwestern’s Marcellus assets in West Virginia as well as their stated intent to grow production elsewhere within their asset base.

While strategies can differ, each operator must make a bet on how much FT to hold and which projects will provide the best return for the associated risk. This choice of strategy, and other factors, will determine how competitive an operator will be among their peers. For more on this, and which E&Ps will be best positioned in the coming years, join us for our free webinar Price Makers vs. Price Takers.