(This is part I of a series where BTU Analytics will highlight the potential implications to market fundamentals from the new Northeast pipeline projects.)

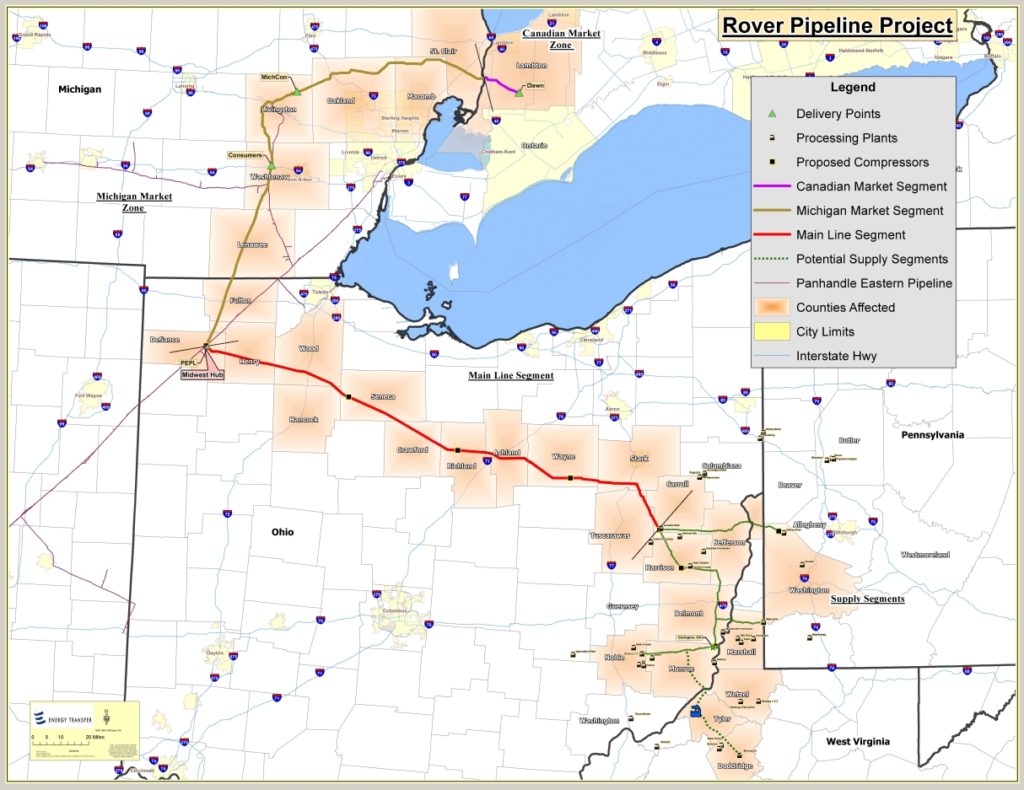

On Thursday, June 26, 2014 Energy Transfer Partners (ETP) announced the ET Rover pipeline. The ET Rover is the latest in a slew of projects designed to take Marcellus & Utica gas from producing areas in Eastern Ohio & Western Pennsylvania to markets in the Midcon, Canada and the Southeast. Following the compounding effect from previously announced Northeast driven reversals, this pipeline could be the proverbial last straw that breaks west natural gas basis (in particular CIG, AECO, TexOK). ET Rover has already received firm commitments for 1.2 Bcf/d of supply, is expected to have an initial capacity of 2.2 Bcf/d and could be expanded to as much as 3.2 Bcf/d pending the results of the open season. The pipeline is expected to commence service to PEPL in late 2016 with service on to Dawn in 2017.

Source: Energy Transfer Partners

The ET Rover project will consist of a new 42” mainline from the heart of expanding natural gas processing capacity located in Carroll & Harrison County, Ohio and will traverse Northern Ohio to connect with the 2 Bcf/d Panhandle Pipeline (PEPL). Before we explore the potential implications of the interconnection with PEPL (to be covered in Part 2) let’s take a step back and look at current Midcontinent flow dynamics.

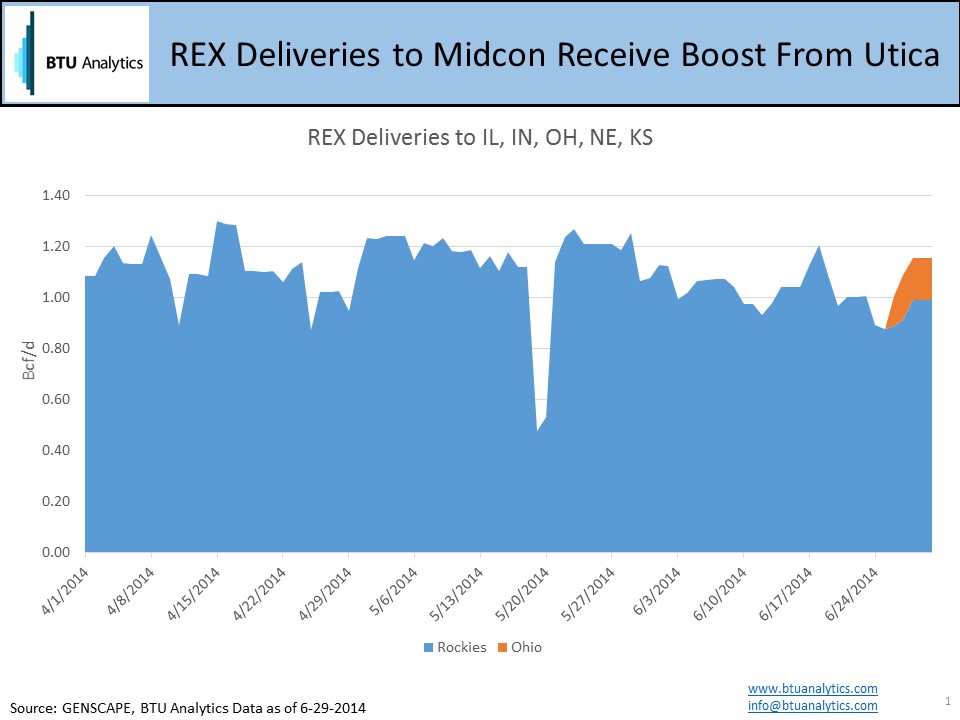

On the same day ETP announced the ET Rover pipeline, REX pipeline began flowing gas into the Midcontinent from both ends of the pipeline following the completion of the 0.25 Bcf/d reversal into Zone 3 in Ohio, Indiana and Illinois. Natural gas nominations data from Genscape indicates deliveries over the weekend from the REX pipeline into the Midcontinent totaled 1.156 Bcf/d, an increase of 0.1 Bcf/d from the prior 30-day average. The increase is due in part to the Markwest (MWE) Seneca gas plant located in Southeast Ohio delivering over 0.16 Bcf/d of Utica production to the pipeline.

The first phase of the REX reversal is a prelude to events to come as additional expansion and reversal projects come online. Over the next 24 months, over 5.1 Bcf/d of reversals & expansions are slated to come online displacing traditional South to North flows on PEPL, Trunkline, Texas Gas, ANR, Columbia Gulf (CGT), Texas Eastern (TETCO), NGPL, & Tennessee. These reversals could cut off traditional outlets for Rockies & Anadarko producers to the Midcontinent as Northeast production soars above 20 Bcf/d from growth in the Utica & Marcellus by the end of 2015.

What makes ET Rover different is it will follow the impact of the REX Zone 3 reversals which we expect to put pressure on Henry and CIG via interconnects with NGPL, Trunkline, ANR and Texas Gas. The ET Rover interconnect with PEPL in northeast Ohio (Defiance county) will put Northeast production in direct competition with over 1 Bcf/d of Anadarko production on PEPL currently serving the Michcon market.

Who will come out on top when Rockies, Anadarko and Canadian production clashes with Marcellus and Utica production in the Midcontinent? Could Phase 1 of the REX reversal be the first blow to producer realized prices and ETP the bell ringing knockout? Or are LNG exports occurring in time to drain Midcontinent pipelines? Are producers over-committing to pipeline capacity or is production so robust that more pipelines will gain commitments? For additional analysis of the role of pipeline reversals on basis stay tuned for Part II of our analysis. Call (720-552-8040) or email (info@btuanalytics.com) now to get your company on the upcoming BTU roadshow to discuss evolving trends in natural gas, natural gas liquids, & crude oil markets.