June has been an exciting month for flow dynamics in Southwest Appalachia (as exciting as flow dynamics can be, anyway), led by Rover’s full mainline startup and the Leach XPress force majeure impacting takeaway and corridor flows. Today’s analysis will dive deeper into the latest on both pipes and look at how Dominion South pricing has responded, and check out the Northeast Gas Outlook publishing later this week for the latest developments on Mountain Valley Pipeline, Mariner East, and more.

Rover Mainline Full Startup

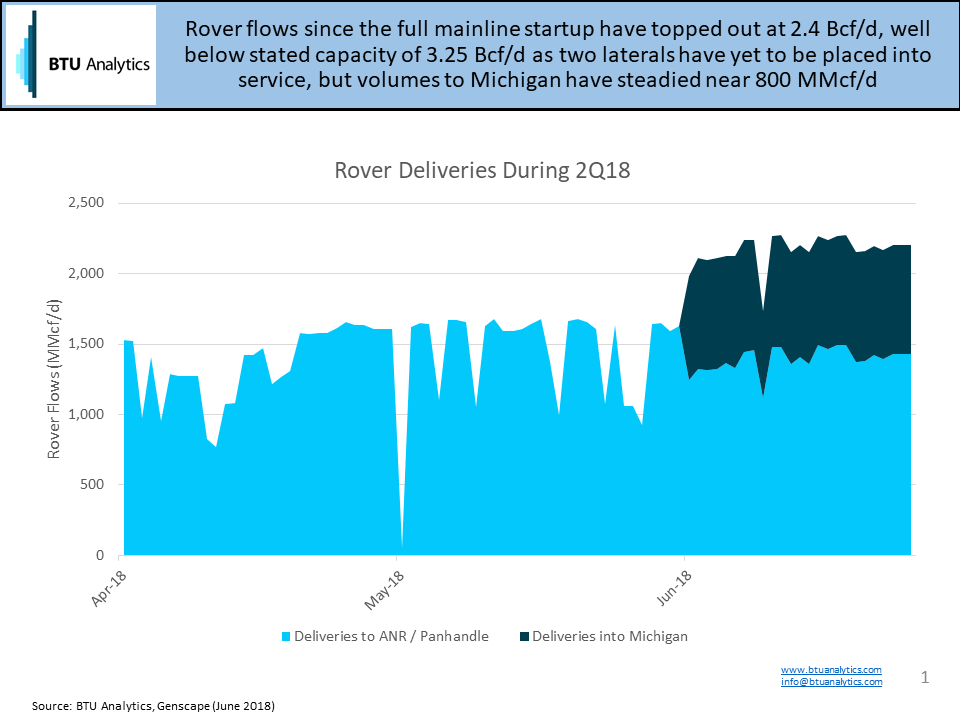

On June 1, Rover placed all mainline facilities into service, including the segment into Michigan, with the full 3.25 Bcf/d of capacity available. Approval is still pending for the Majorsville and Burgettstown laterals, however, and could explain why volume has peaked at about 2.4 Bcf/d. Rover’s capacity into Michigan is about 1.04 Bcf/d, and flows into Michigan have remained at about 0.8 Bcf/d since June 1, with the balance flowing onto ANR and Panhandle.

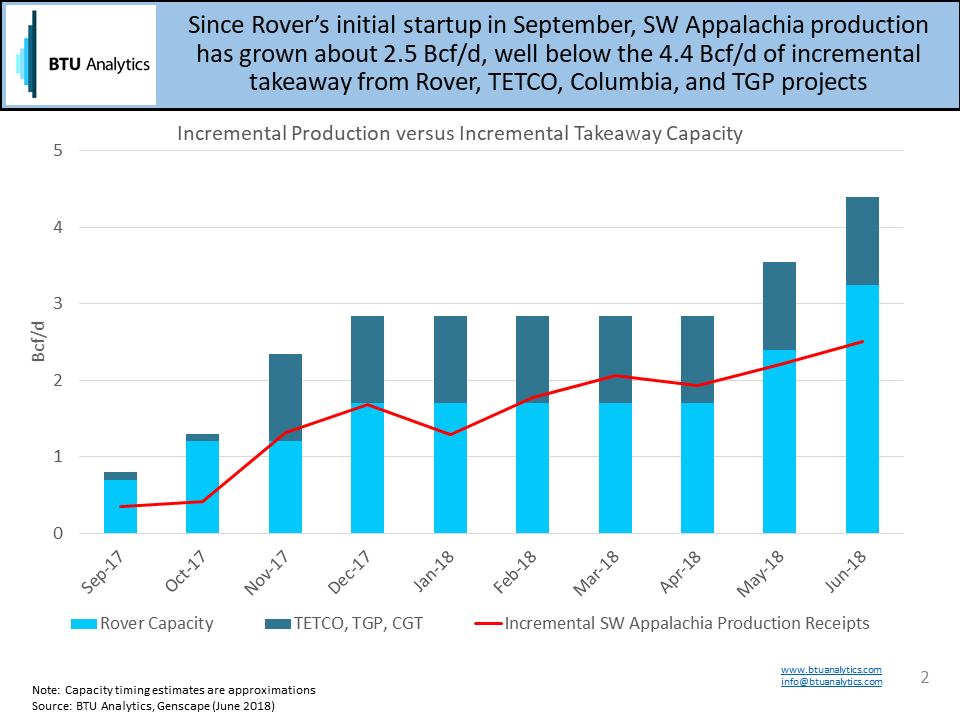

Since Rover’s initial startup in September, along with multiple others late in 2017, Southwest Appalachia production receipts have grown about 2.5 Bcf/d, well below the estimated incremental takeaway capacity of 4.4 Bcf/d as shown in the chart below.

Leach XPress Force Majeure

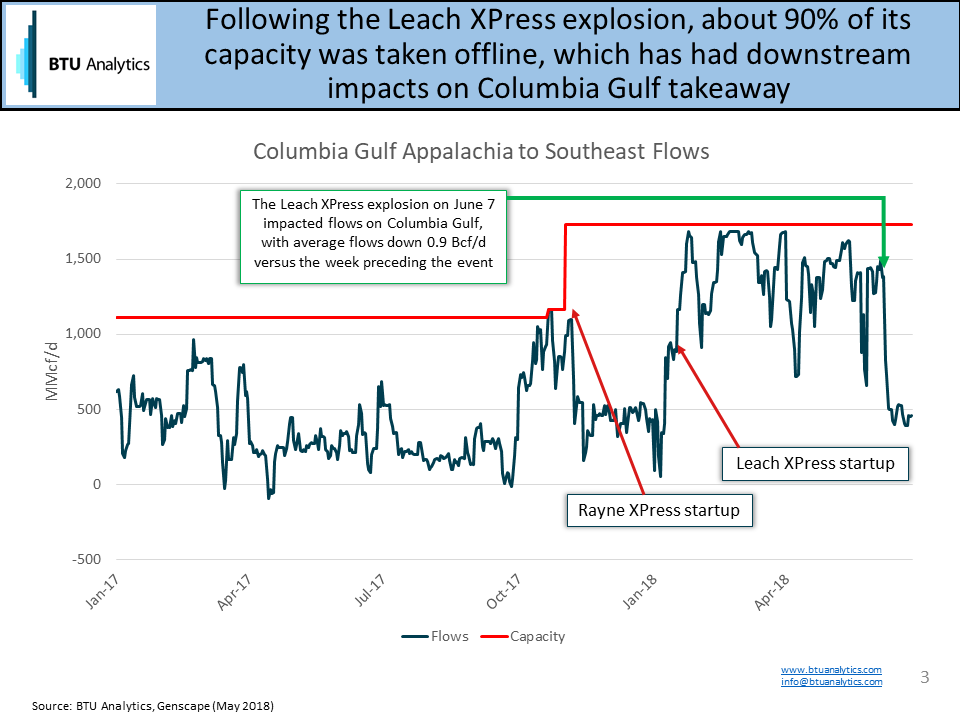

Leach XPress declared a force majeure on June 7 following an explosion in Marshall County, West Virginia that rendered 1.3 Bcf/d of firm transportation service unavailable. The latest update from Transcanada is that the pipe will be restored by early July, but challenging weather conditions have been slowing progress. Gas was mostly able to be redirected along REX and other pipelines, with the total production impact estimated to only be about 100 MMcf/d. The more critical dynamic that we’ve been monitoring are the decreased flows on Columbia Gulf.

Last year, Rayne XPress started up in November, but the increased regional takeaway capacity was not available until Leach XPress was completed in January. With Leach XPress mostly out of commission, flows on Columbia Gulf downstream have been impacted by about 0.9 Bcf/d.

Dominion South Pricing

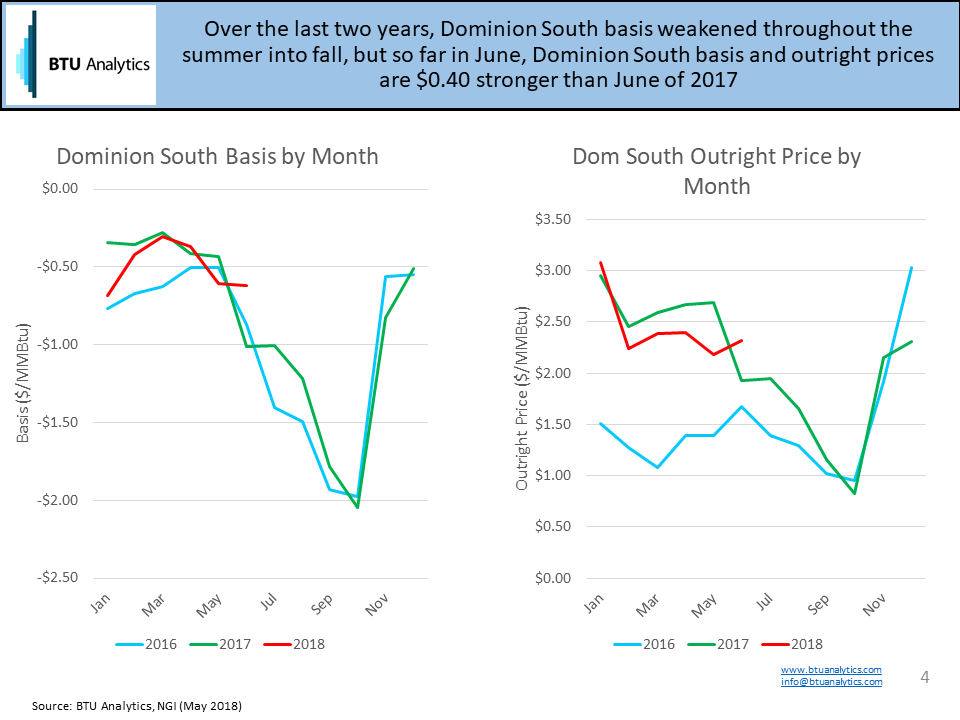

So far, Dominion South pricing in June has been seasonally strong, outpacing June 2017 prices by about $0.40, as production growth has not kept pace with increased takeaway. Over the last two years, basis weakened throughout the summer until winter demand materialized in November as seen in the charts below.

As the second quarter comes to a close, the pace of production growth and pipeline project progress will be key to forecasting pricing dynamics through the end of the year and beyond. Will Dominion South basis crumble again this summer, or will increased capacity help support stronger pricing? To keep up to date on the latest Appalachia infrastructure projects and their impacts on prices and production, subscribe to the Northeast Gas Outlook. For more on the interplay between supply basins across the country, check out the latest Upstream Outlook.