It has been a bumpy ride, but the Northeast has finally begun flows on the first major greenfield project to come to market in almost a decade – Energy Transfer’s Rover. This begins a major shift in Marcellus and Utica production dynamics, with implications for the future of Dominion South and Henry Hub pricing– but what is changing in the here and now?

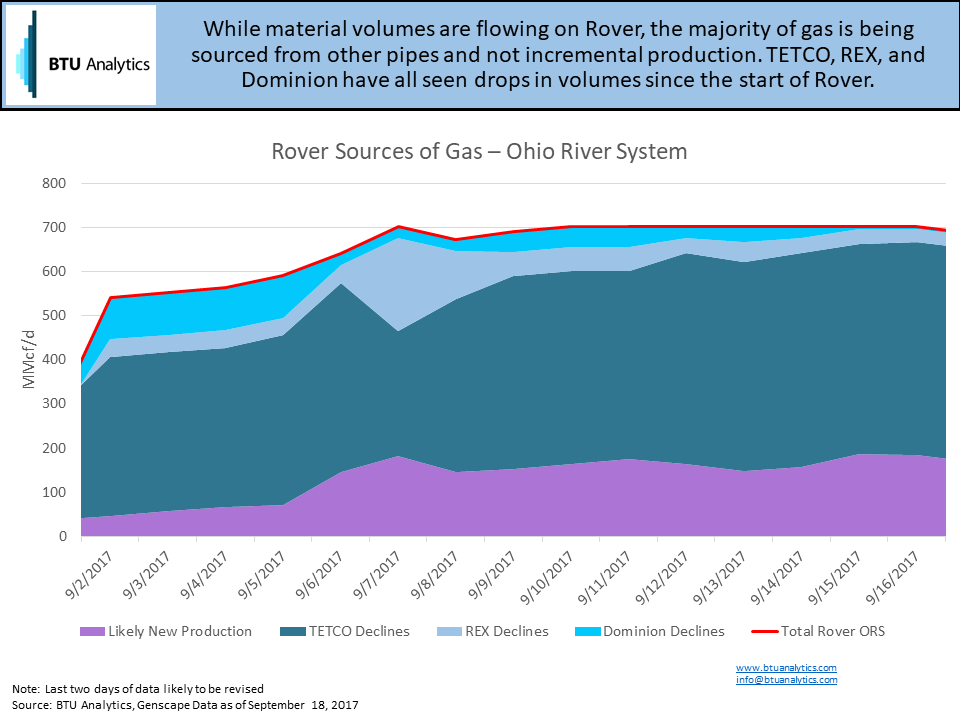

Rover received a notice-to-proceed yesterday for horizontal directional drilling activity which will bring critical capacity to market (we expect a November start-up for the next tranche of Rover capacity), as of today, Rover is receiving volumes only at two points along the Cadiz lateral: MarkWest’s Cadiz processing plant and the Ohio River System. Today we’ll take a granular approach and look at receipts only around those two points. We can see in the graphic below, which compares Rover receipts from the Ohio River system with declines seen on other pipelines, that while Rover has been flowing full at its current 700 MMcf/d capacity, that gas is coming at the expense of other pipes, mainly TETCO.

So now we can answer one of the market’s big questions: how much new production will come online with Rover? To date, we have seen about 150 MMcf/d of new production directly attributable to Rover, which is in line with our Northeast production forecasts.

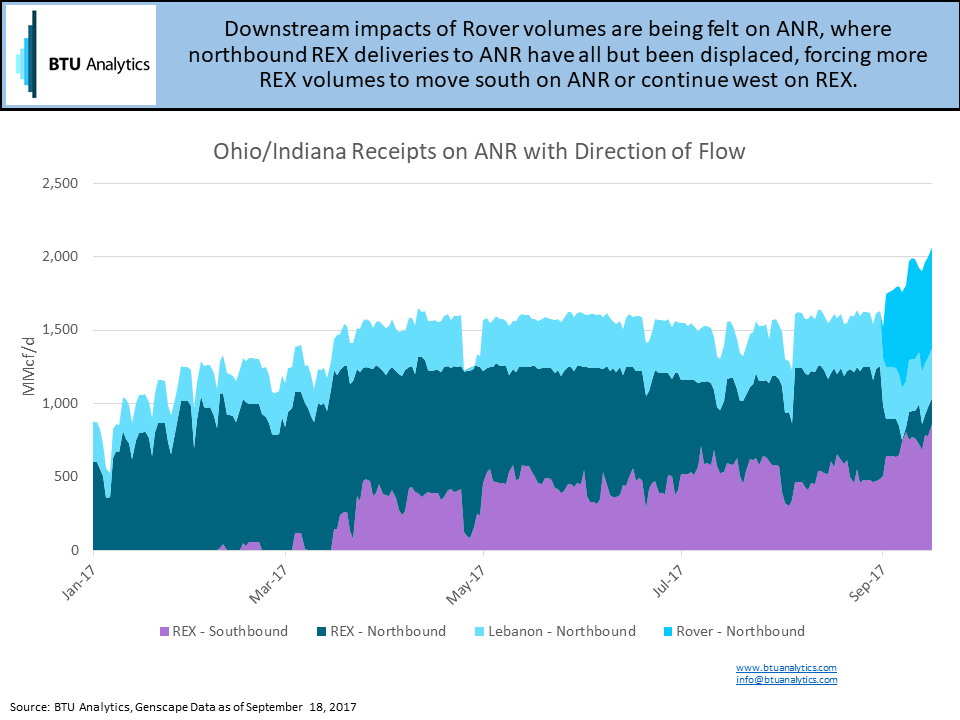

But what about the other end of Rover? Where is that 700 MMcf/d of gas actually going? Currently, almost all of Rover’s volumes are being delivered to ANR, but again, a good amount Rover volumes are displacing volumes from other pipes. Rover deliveries are displacing REX deliveries to ANR. Because of this displacement, REX deliveries to ANR are moving southbound and more gas is moving further west on REX.

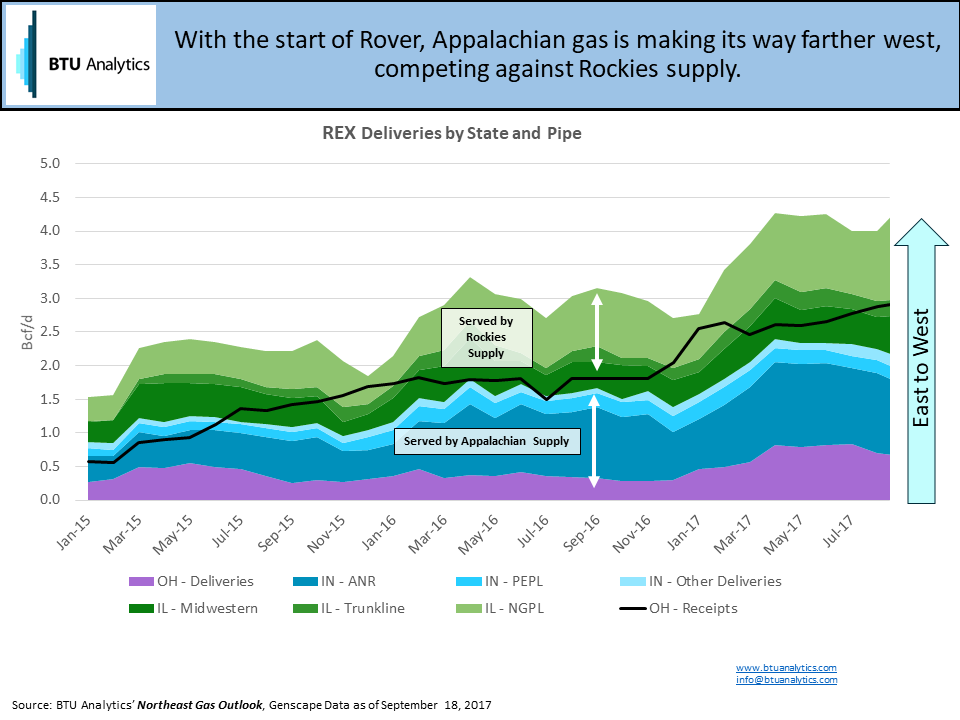

While above we have discussed the direct impacts of Rover, there are other important dynamics taking place a degree removed from Rover. Last week we discussed Tallgrass’s new Cheyenne Connector project with the aim of pushing more gas east out of the Rockies. However, with the start-up of Rover and the displacement of REX gas seen above, an increasing amount of Appalachian gas is making its way farther west, as shown in the graphic below, where deliveries under the black line are being served by Appalachian supplies.

It is likely that winter weather will mask some of the changes taking place. However, assuming a normal winter this year, by Spring 2018, when Rover’s full volume is online and seasonal demand ebbs, we will most likely see two things occur: more Appalachian gas displacing Rockies volumes out of the Midwest and weak supply basin basis as prices come down to force producers to curb volumes. What basis points will be most impacted? And where are operators at the most risk of shut-in volumes? See our Northeast Gas Outlook for the above answers and more insight on the changing dynamics in the US natural gas market.