Permian gas has had far reaching consequences on the US, and even the global, natural gas markets. Permian associated gas production has dragged down NYMEX, pushed Waha prices negative, and ramped up the pain on adjacent basins. However, in the Western Rockies, where Opal pricing has already traded at a premium, growing Permian pressure will continue to force San Juan gas production down and prices higher.

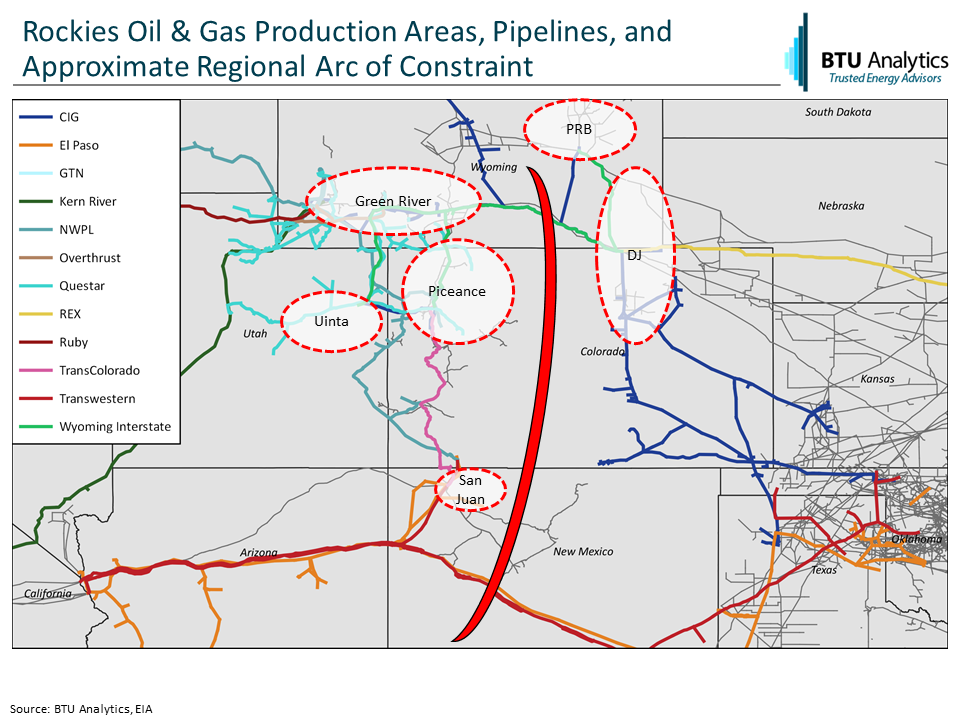

Let’s start with a lay of the land. The following map shows major producing areas west of the Permian, major pipelines, and approximate capacity constraints within the Rockies.

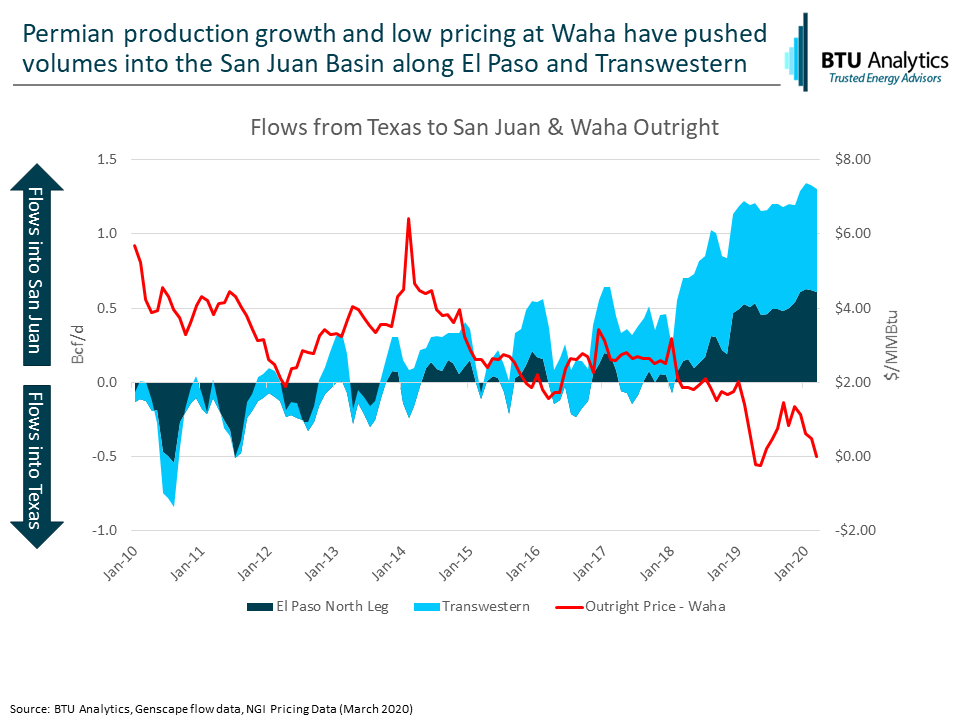

For the Rockies as a whole, the most direct impact of Permian gas growth has been westbound flows out of the Permian along Transwestern and El Paso’s North Leg. Not very long ago, these pipes flowed with San Juan volumes towards both Texas (seasonally) and the Southern California market. However, today those routes are full of Permian gas as shown below.

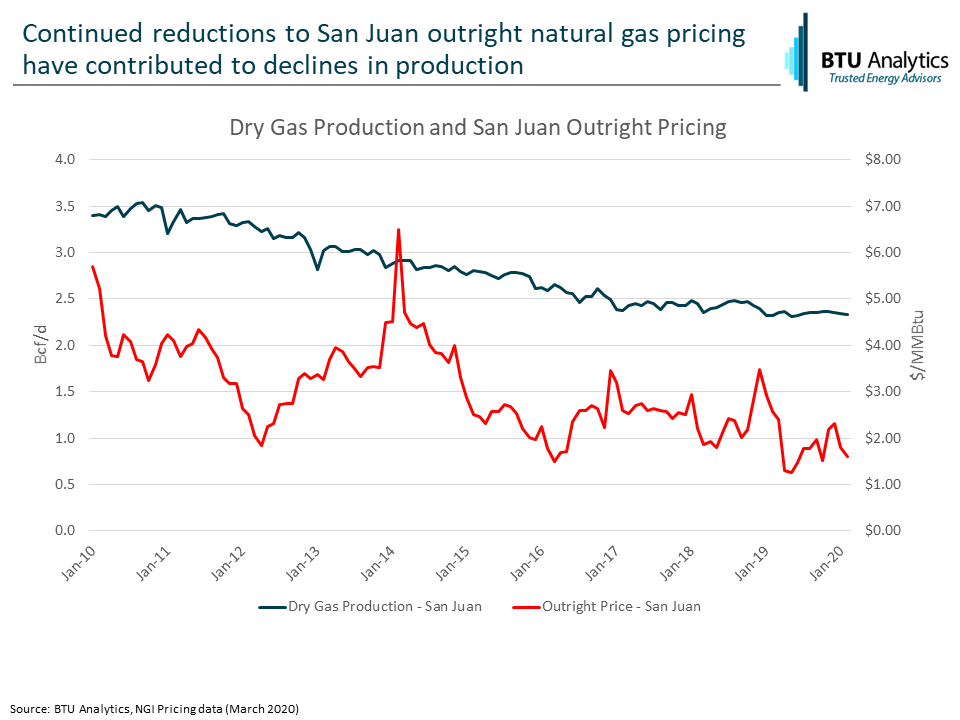

For the San Juan specifically, this loss of demand centers to the south and east put downward pressure on pricing, and pushed production into decline. The graphic below shows the declines we have seen in San Juan gas production, this same story is echoed in other gas-focused plays in the Rockies (Piceance, Green River, Uinta).

And this trend doesn’t show any signs of reversing. Hilcorp recently announced that they don’t plan to drill any wells in the San Juan in 2020 and BP has announced they will be divesting their San Juan assets. From 2018 to 2019, Hilcorp and BP accounted for nearly 30% of drilling activity in the San Juan, signaling that their cutbacks will have a strong negative impact on drilling activity and production in 2020 and beyond.

But with such a bearish outlook for regional producers, how and why would prices be pushed higher? In a recent post, we highlighted the tenuous supply/demand balance in the Western Rockies driven by Canadian supply outages and infrastructure constraints and its effect of pushing Opal prices higher. While the Canadian outages have been resolved (in fact, Canadian supply into the Pacific Northwest/Rockies is expected to grow), declining regional production in the San Juan and other areas will perpetuate the imbalance. Lower local production, along with infrastructure constraints restricting incoming supply from the Eastern Rockies will force Opal and Pacific Northwest prices higher creating demand destruction.

How high will Opal prices have to run? See the Rockies’ section of our most recent Gas Basis Outlook for a deep dive into Rockies’ production, flows, and pricing outlooks.