While COVID-19 ravages demand for services and crude oil in 2020, one bright light for natural gas producers is the rapid imbalance coming to natural gas markets in 2021. Unlike crude oil, natural gas demand in the transportation sector is negligible. Thus, natural gas demand is proving much more resilient to current macroeconomic dynamics at a time when the outlook for associated gas is changing dramatically. Today’s energy market commentary will explore the possible changes in natural gas supply and price in 2021.

On March 19, BTU Analytics published updated capital budget announcements and hedges from producers for our Upstream Outlook D&C Budget Update – 3/19/20. The key takeaway from these budget announcements is that capital budgets are expected to fall at least 36% in 2020 compared to 2019 levels for the 37 US public E&Ps sampled. Not all budget cuts have been equal though. Plummeting commodity prices have left some producers scrambling to cut completion crews immediately, while hedges have insulated some producers allowing them to take a more gradual pace to reducing activity in 2020. However, crude prices have continued to stagnate below $30/bbl putting in question even the revised budgets that have been published from crude oil producers.

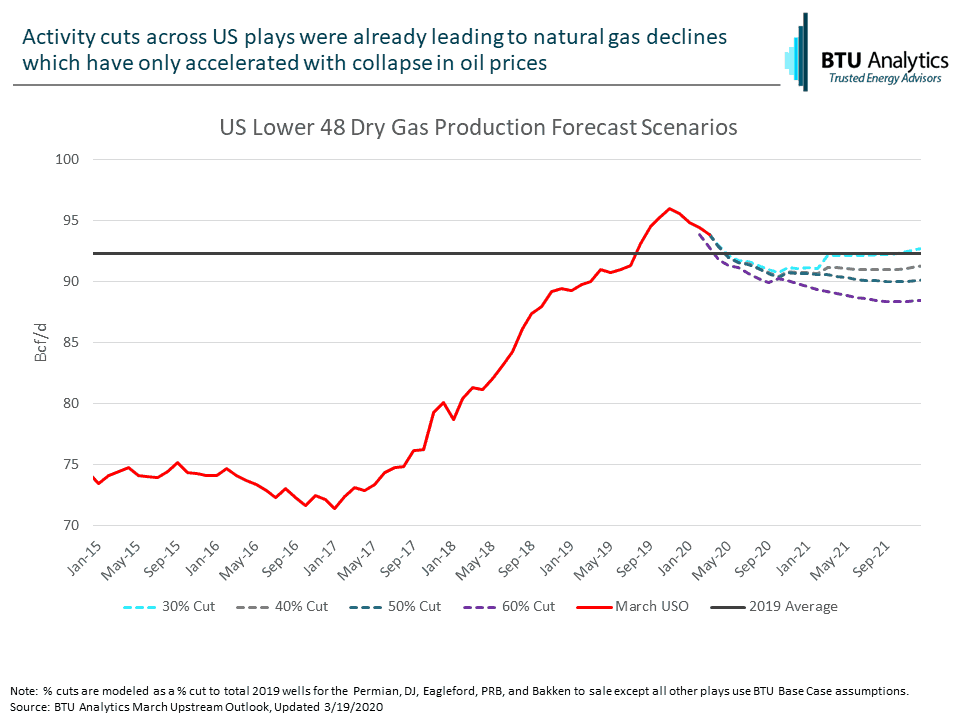

The below graphic highlights potential outcomes for natural gas under BTU Analytics’ base case assumptions for dry gas plays and various activity cut scenarios for the Permian, Eagle Ford, DJ, PRB, and Bakken.

In all the scenarios, natural gas production is set to decline below 2019 average levels by May 2020 and in the most aggressive scenarios, natural gas production could reset below even in January 2019 levels. All of the scenarios account for expected changes in Permian flaring and shut-ins as highlighted by the jump in production in March 2021 following the expected start of Kinder Morgan’s Permian Highway pipeline.

With production declines accelerating from the drop in oil prices, how is the outlook for natural gas prices changing?

The drop in crude prices has provided little strength to natural gas prices in the near term. On March 9, as crude 12-month futures dropped 24% to $33/bbl, natural gas prices experienced a two-day rally that resulted in the 12-month average futures price to climb from $2.08 on March 8<sup>th</sup> to $2.27 on March 10<sup>th</sup>. Since that time, crude futures have fallen to just $30.58/bbl and natural gas prices have given up most of the rally falling back to $2.18 over the same 12-month span.

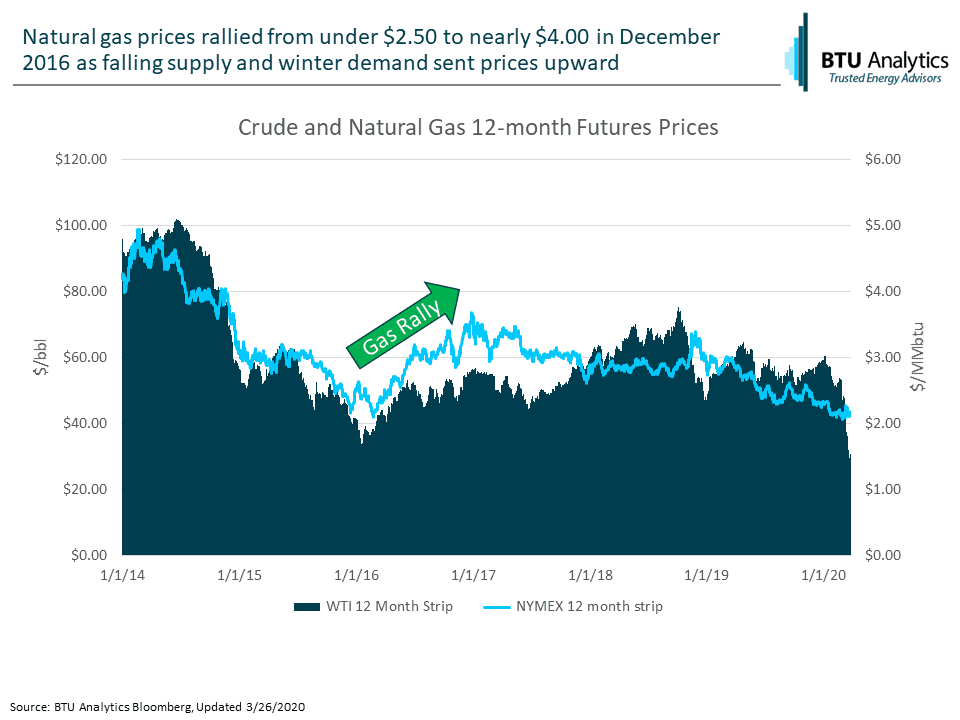

History has shown that falling crude prices can lead to much stronger natural gas prices. The chart below highlights the 12-month futures curve for natural gas and crude oil since 2014.

In 2015, a warm winter combined with the beginning of the first Saudi production surge left prices below $2.50/MMbtu for natural gas and crude oil below $40/bbl in January 2016. By March of 2016, US natural gas production was in decline and declined until January 2017. Over that time frame, US natural gas production declined by 2.6 Bcf/d and set the market for a strong rally in both cash and futures prices during the winter of 2016/2017.

With natural gas production already off over 2.0 Bcf/d from its peak in November 2019 and declines accelerating in oil plays, the extent of the rally in 2021 will only be limited by the level of US demand over the winter of 2020-2021. BTU Analytics’ Henry Hub Outlook clients will receive our latest thoughts on Henry Hub winter pricing in the report publishing March 31, 2020