The natural gas industry has been intensely focused on what is going on in the Permian over the past year. For good reason too. What happens with the associated gas molecules out of the Permian will have far reaching impacts to the broader natural gas market, even impacting Dominion South pricing and production 1,500 miles away. We have discussed these dynamics in detail in our most recent edition of our Northeast Gas Outlook, but today I wanted to take a step back and look past the next couple years to what is yet to come after the first wave of new Permian gas takeaway.

To start with, where do we stand today? Permian associated gas production is surging. Waha continues to weaken. And a spate of gas takeaway projects have been announced. Kinder Morgan and DCP’s Gulf Coast Express seems to be the farthest along with a firm in-service date of October 2019. Other projects announced include NAmerico’s Pecos Trail slated for late 2019, Sempra and Boardwalk’s P2K (Permian to Katy) project, expected in 3Q 2020, and Tellurian’s Permian Global Access Pipeline, which just recently began a non-binding open season.

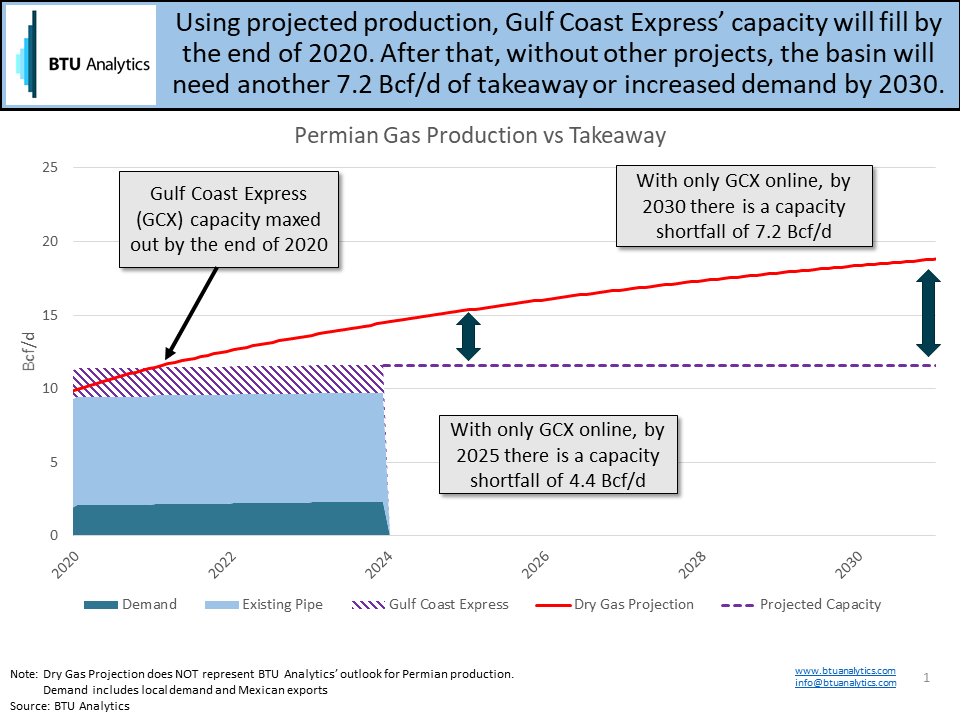

The next natural question is does the market need this approximately 8 Bcf/d of new takeaway out of the Permian? To answer that let’s move our point of reference out a few years. The graphic below shows a projection of Permian dry gas production, using current activity levels. Note that this does not represent BTU Analytics’ outlook on Permian production, which considers additional factors in its forecasts. Included with that production projection is demand (local as well as exports to Mexico), existing pipe capacity, and Gulf Coast Express’ proposed capacity.

Based on projected production, Gulf Coast Express alone won’t provide takeaway relief to the basin for very long, with its capacity full by the end of 2020. Projecting that capacity and demand forward gives us a capacity shortfall of 4.4 Bcf/d by 2025 and 7.2 Bcf/d by 2030. Compare that to the additional three projects following Gulf Coast Express that have a capacity of approximately 6 Bcf/d. That would suggest that all of the announced projects’ takeaway will be needed by 2030. However, there is another potential solution just across our southern border.

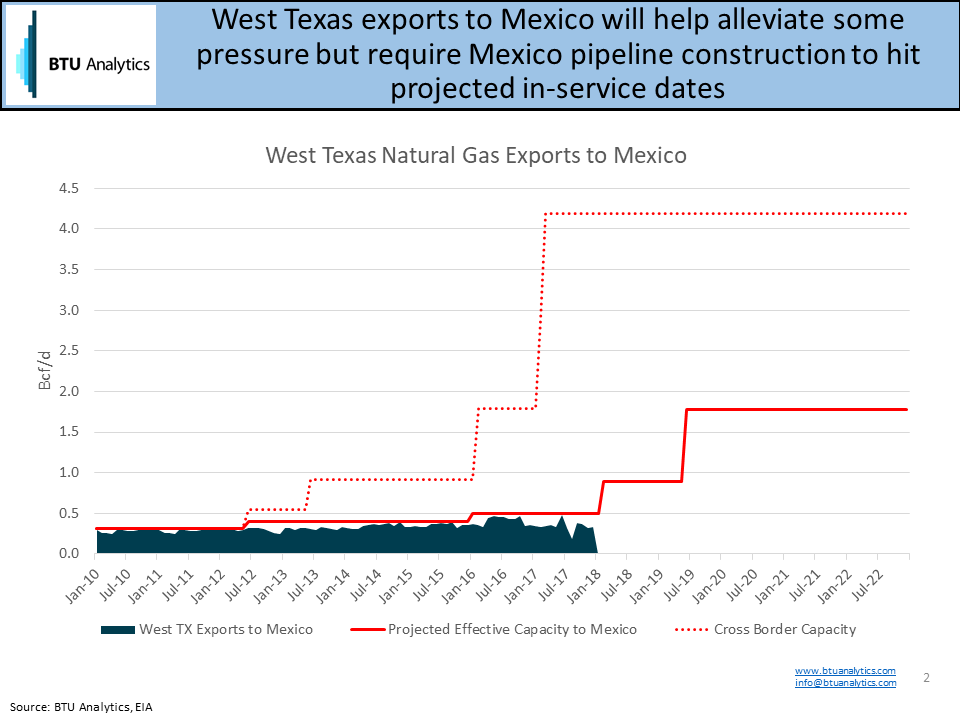

Permian exports to Mexico have provided ever elusive hope for relief out of the basin. As shown by the graphic below, exports out of West Texas have shown little growth even with surging Permian associated gas and cross-border capacity. The limiting factor seems to reside on the other side of the border, where projects have been plagued by delays and opaque statuses.

That being said, with projects in Mexico set to eventually come online over the next year, we would expect the effective export capacity across the border to increase. However, once that effective capacity comes online one of two things can happen: imported gas from the Permian can serve new demand in Mexico, or exports out of the Permian can displace exports out of South Texas (Agua Dulce), thereby helping the Permian, but impacting the broader US gas market.

What does this all mean for gas prices at Waha and Henry Hub? And how will this affect both Permian oil and gas production? For the answers to these questions, and more, see our Spotlight Report in the February edition of the Upstream Outlook.