Low storage inventories and some early winter weather have pushed spot natural gas prices in supply basins to levels gas-focused US producers have only dreamed of. Higher prices may lead to unexpected cash windfalls this winter, but what impact will these higher prices have on production and supply going forward? Is Santa going to bring a higher rig count?

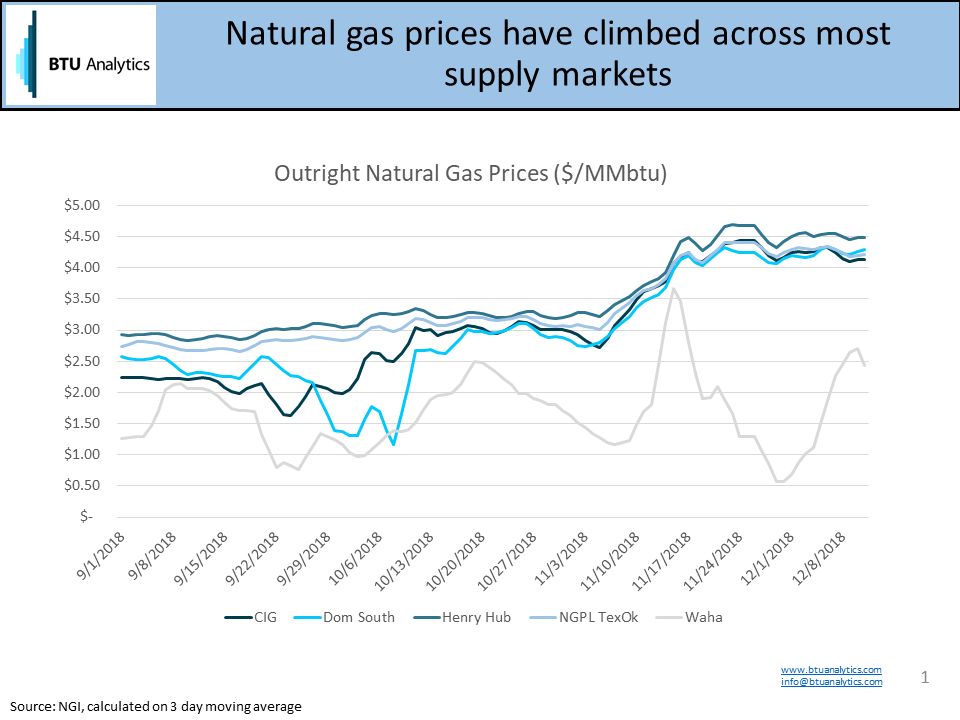

The chart above highlights the run natural gas cash prices have been on since September. Henry Hub averaged $2.94 through the first ten months of 2018. At the beginning of November, prices started their rise, with Henry prices over the last thirty days averaging $4.43/MMbtu. But what makes this climb in prices different than recent history is that supply basins are also along for the ride, with Dominion South averaging $4.13 over the past thirty days.

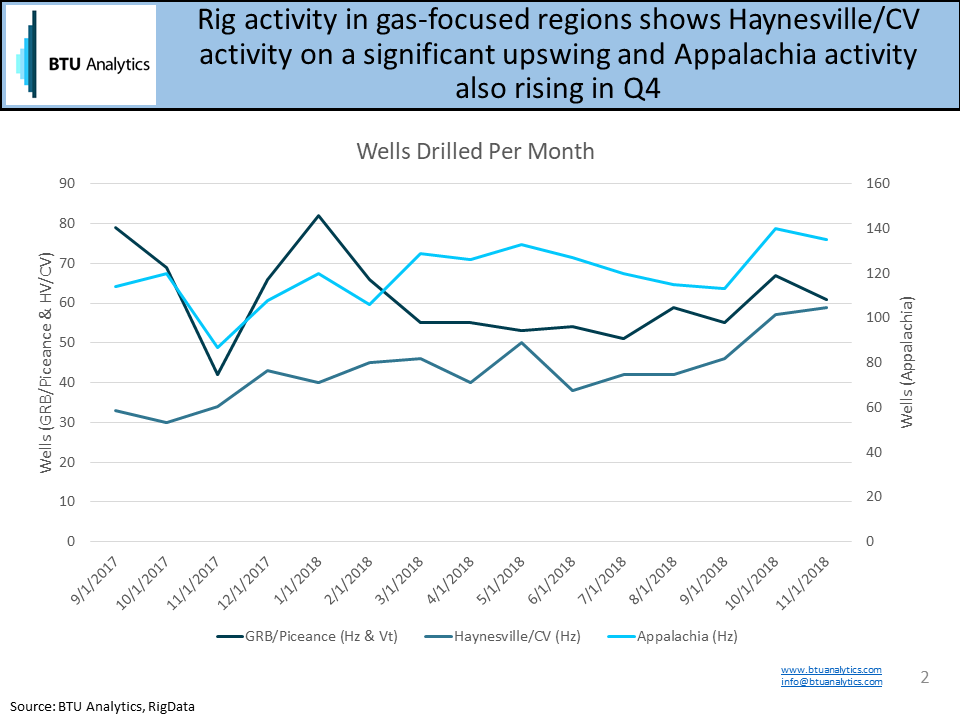

While it’s still a bit early to relate rig counts to the run in prices, it is worth looking at wells drilled per month (an alternative to rig count which is preferred by BTU Analytics) to see where activity has been trending in gas-focused regions.

It is notable that activity in the Haynesville/Cotton Valley region has been climbing since mid-year 2018. Activity in the Green River Basin/Piceance fell off from higher levels at the beginning of 2018 but has since made a bit of a recovery. And in Appalachia (whose activity is charted on the secondary axis to adjust for scale), activity made a noticeable jump in October.

With producer cash flow increasing (at least for unhedged volumes), would we expect these trends to continue higher? Unfortunately, circumstances are a bit more complicated. The first complication is that the amount of time from when a price signals a desire for higher supply to the time new production can arrive at the market based upon that signal isn’t trivial. For most basins, average spud-to-sales time is between 3 and 6 months, and that would be the minimum amount of time necessary for a production response based on new drilling. This is the reason forecasters lag the relationship between commodity prices and rigs.

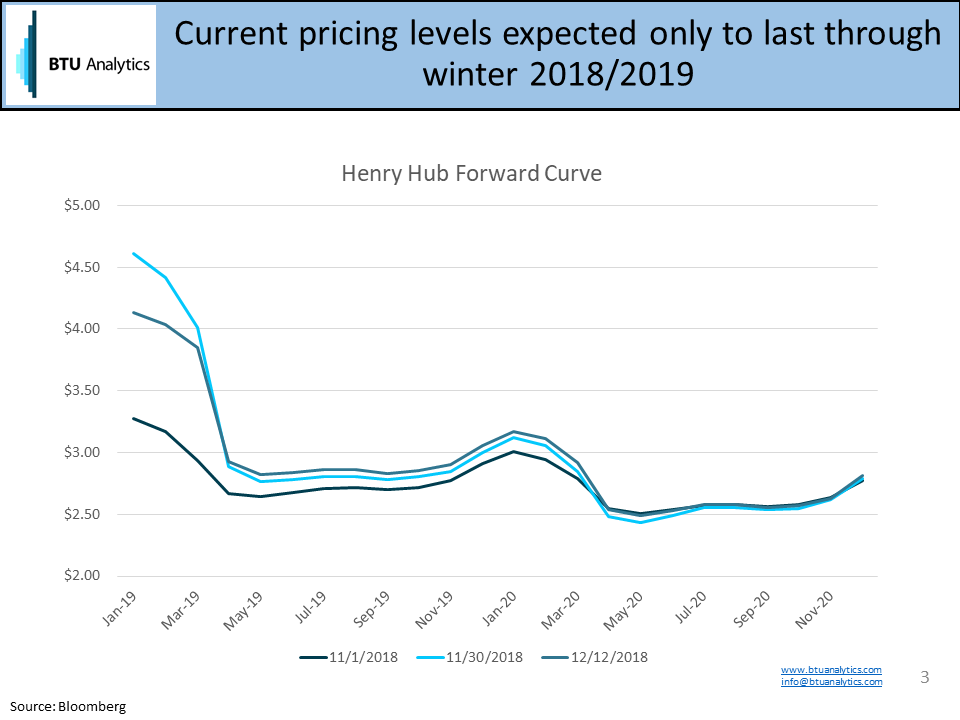

This is also the reason producers look to the forward curve for an indication of future prices. Producers can layer in hedges for future production using the forward curve. Unfortunately, despite a nice run in natural gas cash prices, the futures market isn’t nearly as hospitable. The chart below shows the forward curve for Henry Hub at the beginning of November, the end of November, and yesterday. While winter prices reflect the market’s concerns over this winter’s storage levels, the market is pricing a return to sub $3.00 pricing in May.

While producers can’t necessarily hedge out higher prices and ramp up activity, the windfall from higher prices this winter could still have an impact on how producers react to future price signals. For more on BTU’s thoughts on how today’s prices impact future activity, request more information on our Upstream Outlook service which this month includes a deep dive on the supply and demand outlook for 2019.