Earlier this month, a bi-partisan group of US lawmakers introduced legislation expanding US sanctions regarding the Nord Stream 2 gas pipeline currently under construction between Russia and Germany. European gas storage is already facing constraints due to an oversupplied global LNG market, and a new source of cheap gas from Russia could place even more pressure on the European market. With the pipeline scheduled to be complete as early as 4Q 2020, Nord Stream 2 could further inhibit a rebound for US LNG exports in 2021. Today’s energy market insight will provide an overview of the project and potential implications on US LNG exports.

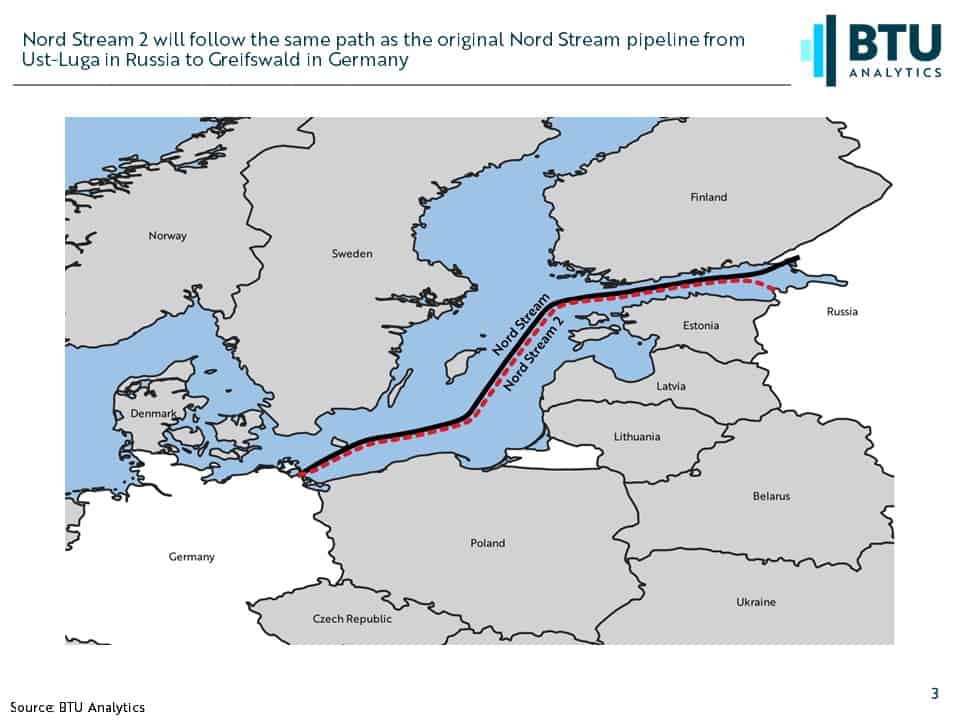

Nord Stream 2 is a pair of pipelines with a capacity of approximately 5.3 Bcf/d running from the Russian city of Ust-Luga to Greifswald in Germany. Despite originating at a different port, it will effectively follow the same route as the original Nord Stream pipeline currently in operation doubling the undersea capacity from Russia to Germany to 10.6 Bcf/d. Once complete, Russia will have the ability to significantly increase gas deliveries into one of Europe’s biggest markets while also moving away from more expensive routes through Ukraine or Poland. The US, fearing increased European reliability on Russian supply as well competing for market share with US LNG exports, has moved to increase sanctions on those who help get the project over the finish line.

Best case scenario for the US? Gazprom decides to abandon the project and considers the ~$10.5 billion USD already invested in the project a sunk cost. While this scenario seems unlikely, Gazprom is facing significant regulatory hurdles from Denmark and Germany, in addition to the pending threat of sanctions from the US, that could force them to give up on the project despite being just 100 miles from completion. However, as with the Power of Siberia in Eastern Russia, the motivations behind Nord Stream 2 are as economic as they are geopolitical making it even more likely that the project will be completed no matter the cost.

Assuming the project is completed, whether that be in late 2020 or sometime in 2021, the resulting pipeline could potentially bring up to 5.3 Bcf/d of additional gas into an already oversupplied European gas market. As BTU Analytics discussed in a blog earlier this month, European storage is already in a precarious position requiring sustained cuts to US LNG to avoid reaching capacity. The addition of an incremental 5.3 Bcf/d of cheap supply would surely overwhelm the European market. As a result, Nord Stream 2 is more likely to displace existing sources of supply rather than adding even more gas into the European market.

Germany currently imports over 90% of its gas supply with Russia the largest supplier followed by Norway and the Netherlands. Thus, some of the first sources to be displaced are likely to be the piped imports Germany already receives including some from Russia via alternate routes. Gazprom has already indicated that upon completion of Nord Stream 2 they will begin to ramp down service from approximately 6.3 Bcf/d that currently runs through Ukraine to approximately 3.85 Bcf/d in 2021 and beyond. Russia could also choose to decrease deliveries through the Yamal pipeline (3.2 Bcf/d) that runs through Poland, especially in light of the recent fine levied against Gazprom by Poland after failing to cooperate with an anti-monopoly investigation.

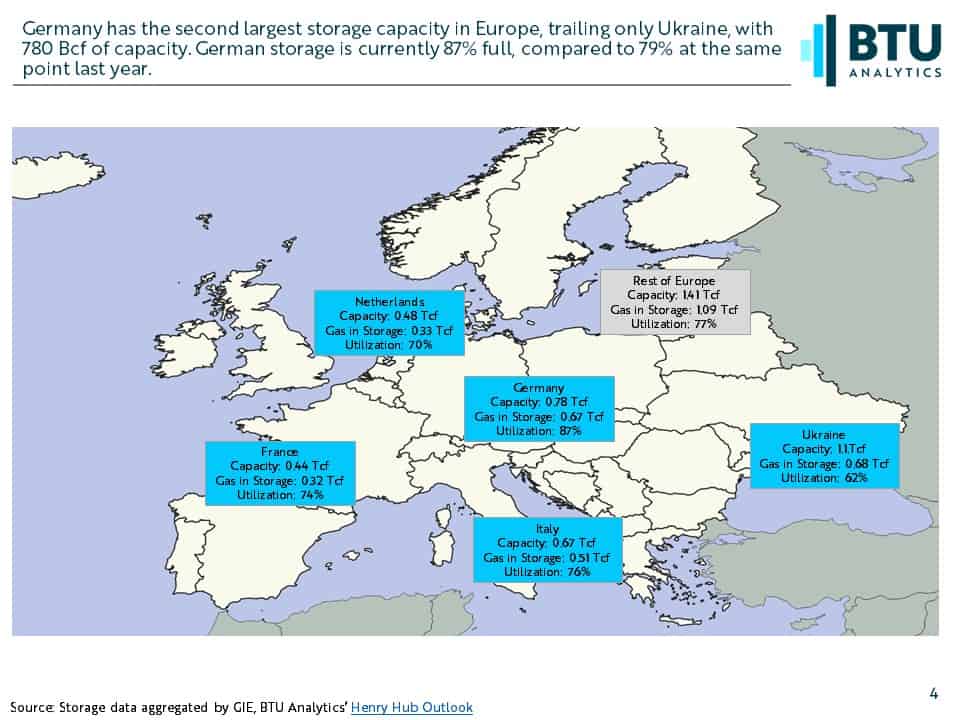

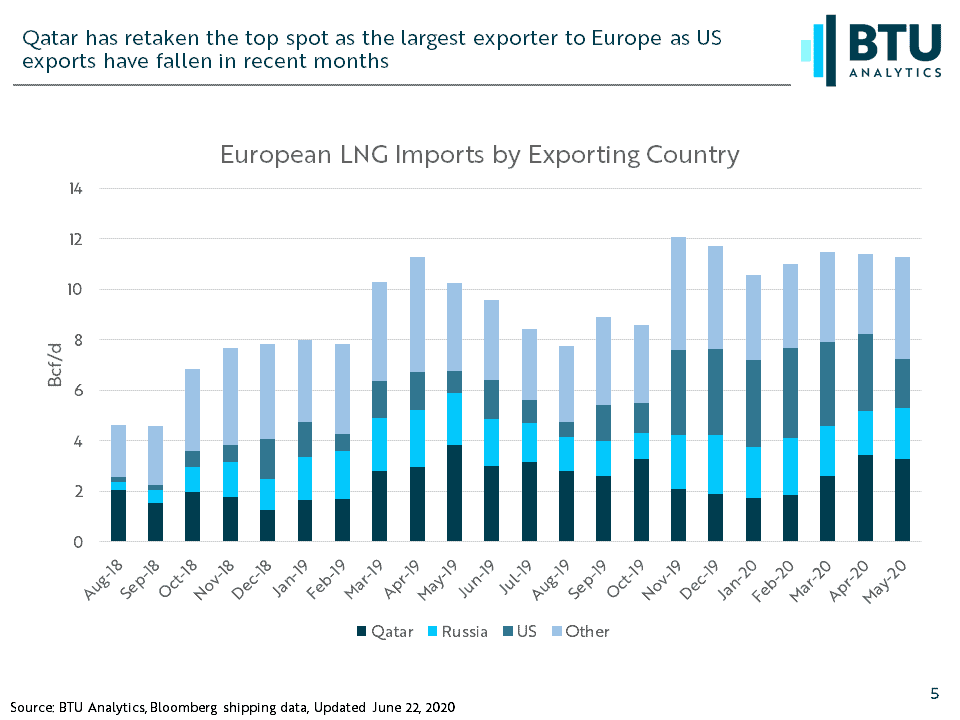

While Germany does not currently import any LNG (although there are proposals to build up to four import terminals in the future), increased Russian supply via Nord Stream 2 would have knock-on effects that could potentially decrease European LNG imports. Crucially, Germany has a considerable amount of natural gas storage. With over 770 Bcf of storage capacity, Germany ranks second in Europe behind the Ukraine who has approximately 1.1 Tcf of capacity. Excess supply from Russia being absorbed by storage in Germany would significantly hamper the ability for Europe to absorb excess LNG cargoes, predominantly from the US, as it has over the past two years. In addition, the US must compete with Russia and Qatar as the other major providers of LNG to Europe. While the US briefly overtook the top spot earlier this year, Qatar has re-emerged as the top supplier and has indicated it will not slow down deliveries despite the concerns around storage levels.

If Nord Stream 2 comes online as expected, the influx of supply into Europe could place further pressure on a US LNG recovery in 2021. With Europe no longer able to serve as a sink for excess LNG, attention will once again turn to Asia where a resurgence in gas demand would be key for US LNG producers. For more on Europe’s impact on US LNG and how it impacts US gas fundamentals, request a sample of BTU’s Henry Hub Outlook.