With the news on April 20 that Kinder Morgan is suspending further work on Northeast Energy Direct (NED), which was proposed to connect NE PA with New England, and the announcement that Williams Company was denied a key permit necessary to build the Constitution pipeline out of Northeast Pennsylvania on April 22, those bullish on Northeast production are suffering growing anxiety that the expected relief from regional infrastructure constraints might be delayed further. But what if that relief doesn’t come at all?

In the past we’ve discussed the expected flood of new Northeast pipeline infrastructure backed primarily by producers seeking to escape painful regional pricing differentials in the local market. In their excitement to get to a future where pipelines no longer constrained production, we argued that individual Northeast producers didn’t account for their own ‘groupthink’, and too many producers backed too many projects all chasing the same expected demand growth in the Southeast. But organized opposition is having an impact on the timetables for many of the larger capacity projects as environmental opponents seek to sink pipeline projects as a way to limit future fossil fuel development.

What would the US natural gas market look like if we didn’t build another greenfield pipeline out of the Northeast?

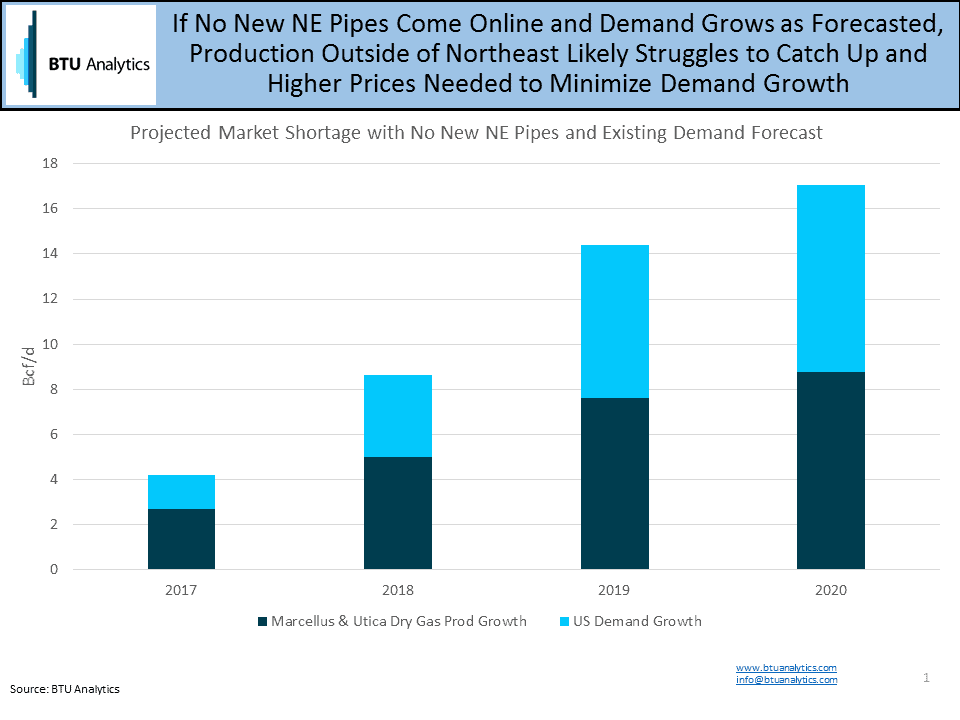

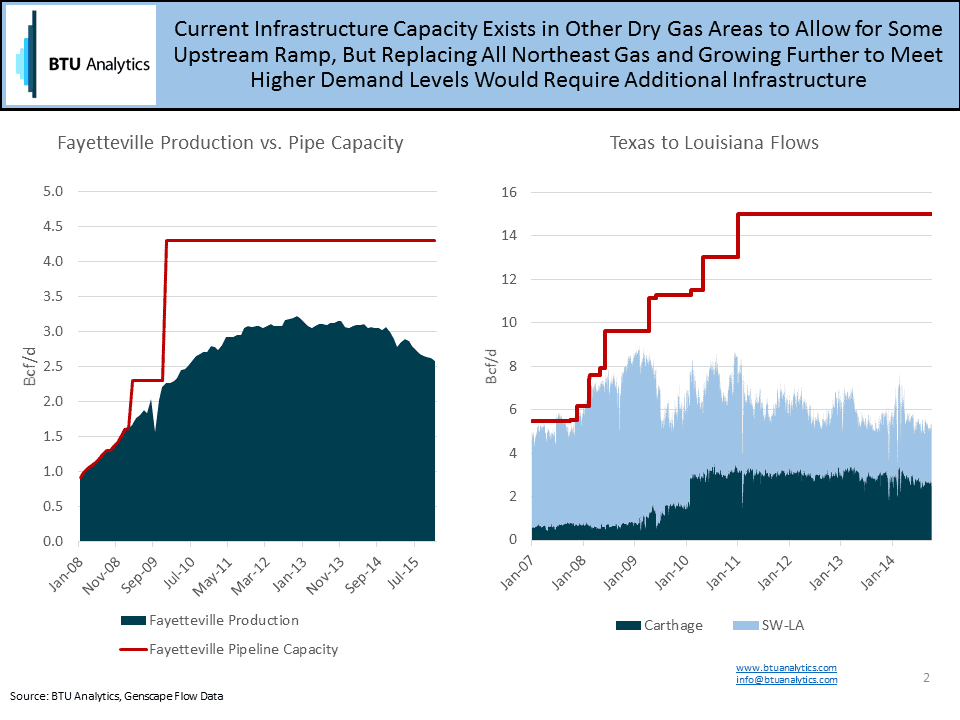

It will depend on the path we take to get there. The first path assumes that the market has certainty that no new pipes are coming. If all greenfield projects were suspended tomorrow, we would likely see the futures curve shift significantly higher as Northeast producers would no longer jump on any opportunity to hedge future production anytime the futures curve wants to push above $3.50/MMbtu. US supply would respond to the higher price signal and outside capital would flow to producers with dry gas acreage in the Haynesville, Fayetteville, SCOOP, Dry Eagle Ford and Rockies as more production from these plays is priced into the future supply stack. New infrastructure would also need to be conceived to route this new production to growing demand in the Southeast and Southwest. But overall, US supply could respond relatively efficiently to the new environment, although we would have higher overall prices.

The second path is a purgatory of sorts — projects continue to be delayed, but because the market is uncertain of how many Northeast projects will come to market and when, supply outside of the Northeast fails to respond. Producers outside the Northeast aren’t able to lock in hedges to ramp up capital programs because Northeast producers continue to hold down the futures curve. Volatility returns to the gas market in a big way as higher prices will be necessary to destroy potential demand since supply lacks the ability to keep pace.

In a previous era of shale development, we had more risk-takers who were willing to make big bets on which way the commodity price winds would blow, but many of those risk-takers have either cashed out and moved on or have been silenced by their lack of liquidity and capital resources. This cyclical industry is prone to overcorrecting, but has everyone on the upstream side gotten too conservative after two years of depressed natural gas and crude oil prices? As it looks more likely that we’ll enter pipeline purgatory, we can’t help but miss the brazen actions of some of shale’s early players. It seems that traders might be the biggest winners in any case.

For BTU Analytic’s latest views on Northeast infrastructure, project timing and production forecasts, request a copy of our latest Northeast Quarterly Report.