Second quarter earnings announcements have shaken up the outlook for gas plays going into the second half of 2019. Diversified operators, such as Chesapeake, intend to pivot to growth in oil production, but not all producers can toggle between gas and oil asset development within their acreage positions. Montage Resources plans to grow liquids production in the second half of 2019 by 40-45% compared to the previous six months to offset diminishing returns on dry gas production. While it is true that wet gas production has exposure to NGL uplift from liquids, current pricing for NGLs does not promise significant economic improvement for wet gas play economics. Today’s Energy Market Commentary will explore historic NGL pricing trends, highlighting how current liquids pricing relationships differ from historic norms.

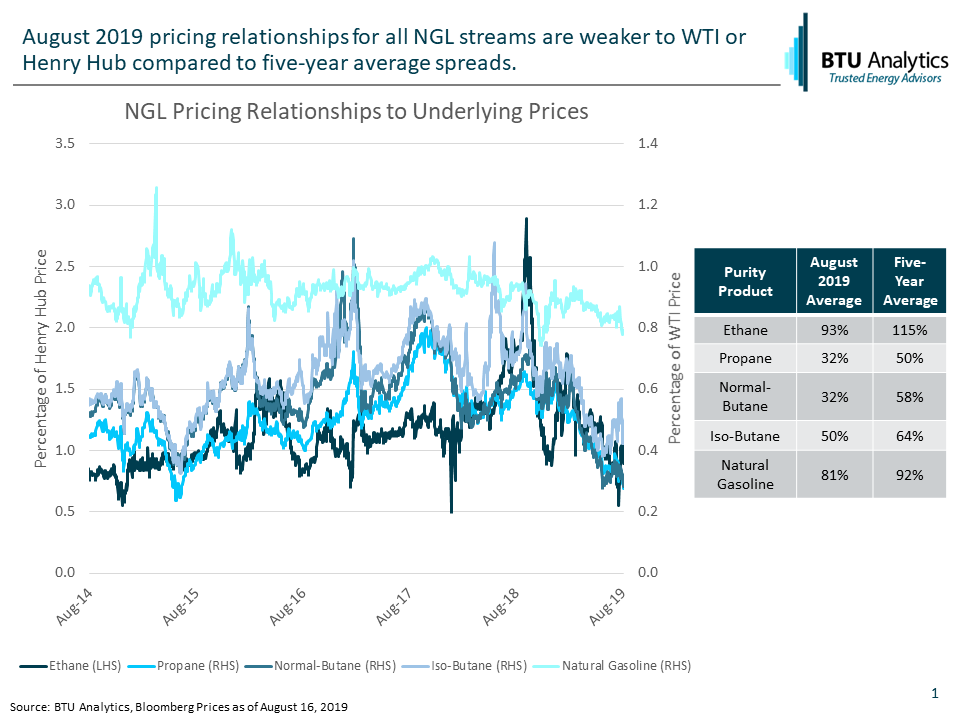

The price ratio of natural gasoline (C5+) to crude pricing is the most predictable due its primary use being as blend stock in the motor gasoline pool or as diluent for heavy crude oil. As a result, natural gasoline prices historically have been highly correlated to oil prices with a very narrow discount to crude oil. However, in 2019, natural gasoline prices have begun to disconnect from crude oil. Growing supply in Canada combined with declining Venezuelan oil production has reduced the call on natural gasoline as diluent. In August 2019, natural gasoline pricing stands at just 81% of WTI compared to the five-year average of 92%.

While natural gasoline is trading at a 10% discount to normal levels, all other NGL streams have even weaker spreads compared to their five-year averages currently. Ethane, whose pricing is pegged to Henry Hub, experienced a run up in pricing around this time last year. The culprit in the price blowout? The combination of several new steam crackers starting service and bottlenecks in NGL fractionation capacity. As a result of the inability to fractionate additional ethane from the NGL stream, ethane prices ran to 290% of Henry Hub on September 18, 2018. However, new fractionation projects combined with producers saturating the market with ethane to avoid natural gas pipeline constraints in the Permian have resulted in ethane prices trading below Henry Hub at Mt. Belvieu. A situation that shouldn’t occur except that regional natural gas prices in the Permian, Oklahoma, and Rockies are so weak that producers make more revenue selling discounted ethane than selling into the local natural gas markets.

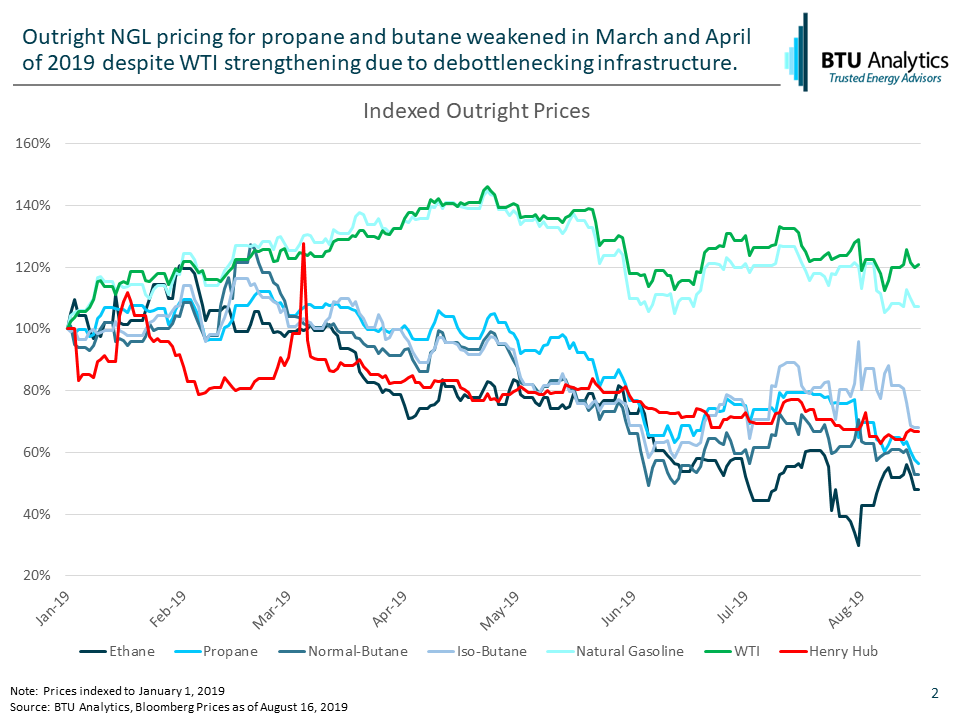

In addition to weak ethane pricing, propane and butane prices have plummeted significantly from the beginning of the year, as highlighted in the chart below. Propane and butane prices are trading at just 60% of the value in January despite crude oil prices remaining relatively flat. As a result, propane, normal butane, and iso-butane are trading at just 32%, 32%, 50% of crude respectively.

The decline in prices put all three streams at least 20% below their normal range. A combination of export bottlenecks, surging supply in the US, and competition internationally has placed downward pressure on US LPG pricing.

While NGL uplift might provide some relief to producers exposed to current natural gas prices, the revenue boost from NGLs appears to be waning. The onset of winter demand could help bolster LPG demand, but for the time being, the NGL uplift appears to have dried up in 2019. For more on the impacts of changes in producer investment strategies in response to evolving price dynamics, check out BTU Analytics’ Upstream Outlook.