As a new wave of pipeline projects out of the Marcellus and Utica gets set to flood the Midwest market, Canada and the Midcontinent molecules are beginning their search for new demand centers. As we mentioned earlier, Alliance is expected to weather the storm better than most other pipes because of its unique processing dynamics and economics, leaving 1.3 Bcf/d of Canadian gas from Northern Border Pipeline and Great Lakes left to fend for scraps. Will Canadian producers be able to find new outlets for their gas or will Canadian supply at AECO be priced to low to discourage long term investment, even in the liquids rich Montney and Duvernay?

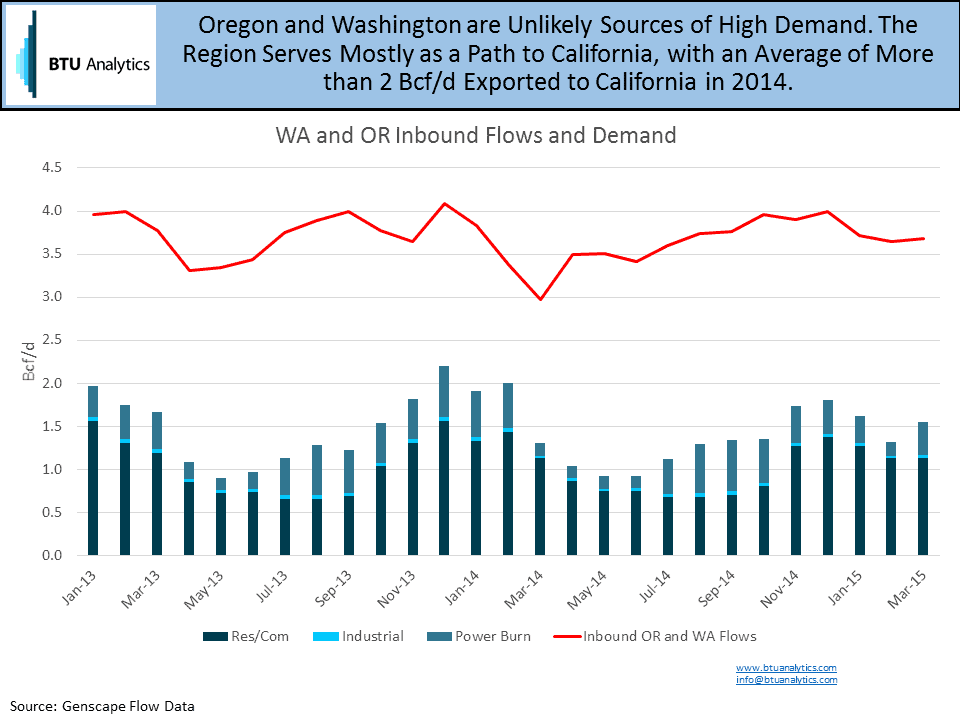

One potential and existing outlet for Canadian producers is the US Pacific Northwest, but Oregon and Washington are unlikely sources for natural gas demand. Taken together, they only account for only about 2.5% of nationwide natural gas demand, serving mostly as a pass-through to California.

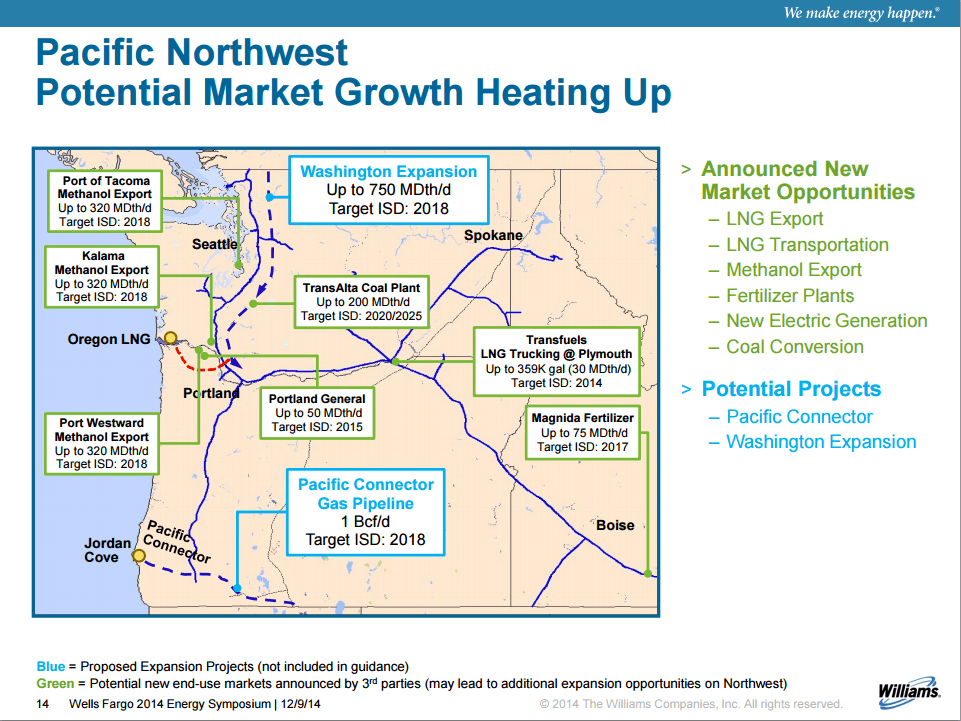

So, continuing the status quo won’t improve the situation considering the needed natural gas demand, but some announced projects may provide relief. The largest of these projects are two proposed LNG terminals: Jordan Cove and Oregon LNG. Combined, they could potentially bring up to 2.45 Bcf/d of demand to the region, although projected in-service dates aren’t until 2019 and 2020.

New industrial and power plants may provide another outlet for wandering molecules. Northwest Innovation Works has proposed three methanol plants, which can consume up to 0.96 Bcf/d in total, coming online in late 2018. Couple that with power plant projects currently in the works that will bring online an additional 1,600 MW (about 0.144 Bcf/d) of natural gas fired electricity in 2018 and 2019.

These proposed projects paint a rosier picture than the likely reality. If history is any indication, these projects will face strong regulatory headwinds that will put their completions in jeopardy. Well organized community and environmental groups have been successful in forcing companies to cancel past projects, particularly in the coal industry where at one time in Washington and Oregon at least six proposed coal export facilities were in the works. Of the six, four have been shelved due to environmental, regulatory, and finally market conditions. So a better solution might be one that requires no new construction or facilities at all. Nature might provide the answer to natural gas producers’ prayers in the form of the ongoing drought on the west coast.

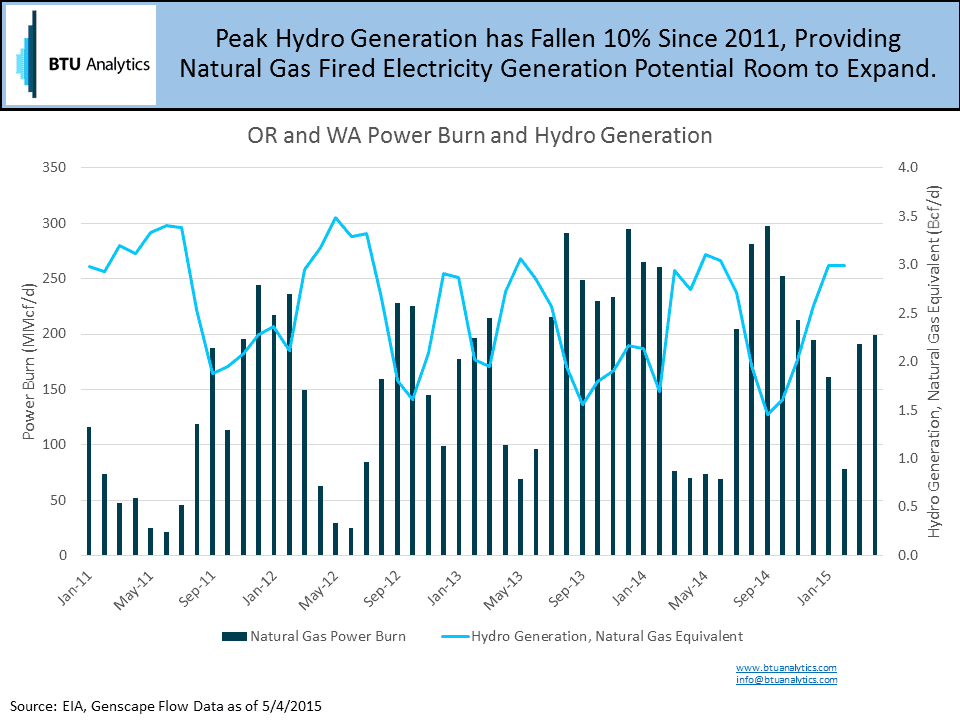

Since the region relies on hydroelectric generation for the majority of its power (64% in 2014), reduced river flow due to a prolonged drought could be an advantage for natural gas demand. With only two coal power plants in the region, both of which are being retired, natural gas stands to gain from any drop in hydro generation. If we look at the hydro power produced in Oregon and Washington and convert that to a natural gas equivalent, there is between one to two Bcf/d of potential demand for natural gas.

While the proposed projects could provide relief to the broader market, taking market share from hydro power would provide the most readily available source of demand. That is, if the weather stays sunny and the sky clear as Rover, Nexus, and REX’s expansions move closer to their completion.