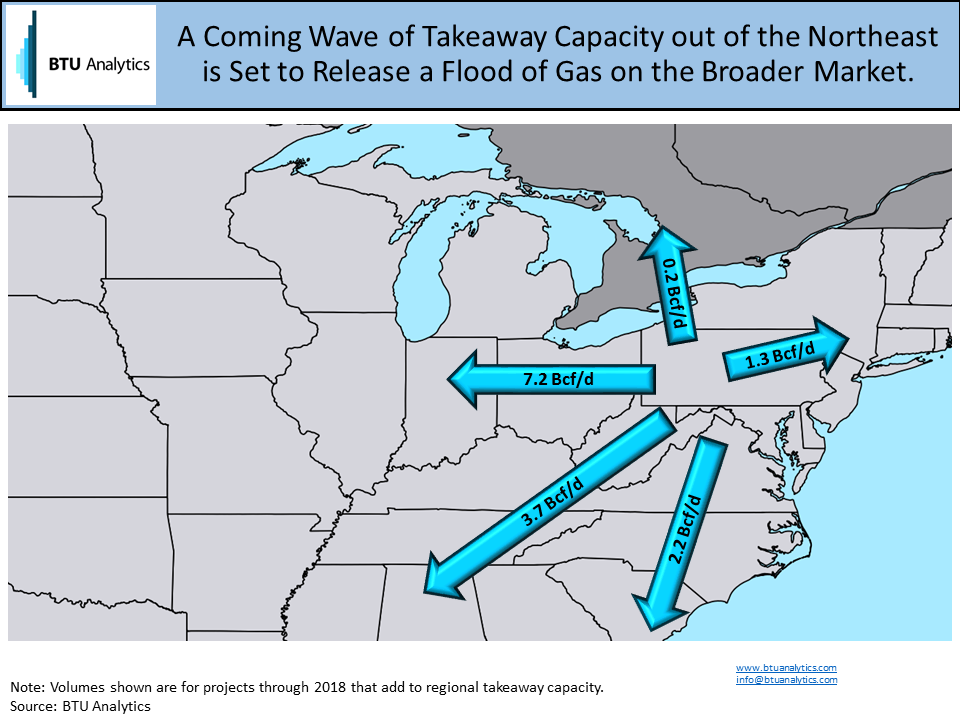

The dam is about to burst in the Northeast. The question is who will drown in the coming flood of natural gas? BTU Analytics is currently tracking 42 Bcf/d of Northeast projects coming online through 2018. Of that capacity, 14.6 Bcf/d will help carry gas out of the region. Some of the most notable of these projects are Energy Transfer’s Rover Pipeline at 3.25 Bcf/d, Spectra’s Nexus Pipeline at 1.5 Bcf/d, and a series of REX Pipeline expansions bringing the pipe’s total east to west capacity to 2.6 Bcf/d.

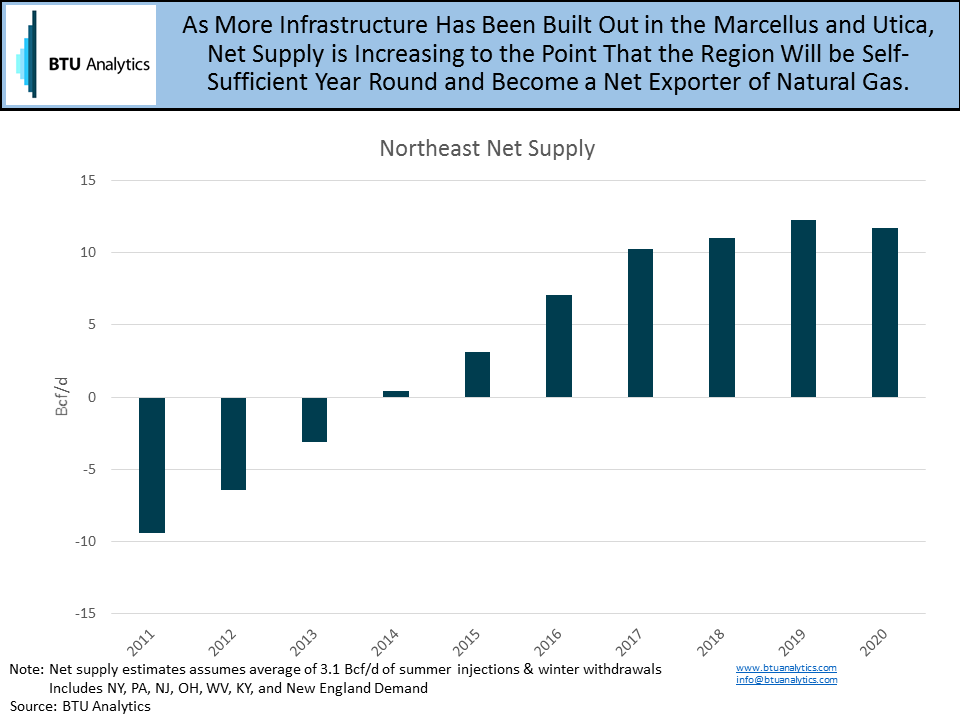

Infrastructure constraints in the Marcellus and Utica have been the norm since 2011 and because of this, many wells were either choked back or forced into backlog. Persistent basis differentials became the norm as supply overwhelmed demand and pipe takeaway, as evidenced by Dominion South spreads, where a one (sometimes two) dollar discount to Henry Hub is not out of the ordinary. That time is coming to an end, however, as build outs that contribute to regional takeaway capacity will let production flow freely. We have seen this in the past as the Northeast’s net supply (Marcellus and Utica production less regional demand) has made a steady march upward. Once reliant on importing gas from other regions to serve seasonal demand, the Northeast will soon be able to meet demand year round from its regional supply and storage. Looking at the same data on an annualized basis shows that the Northeast has already become a net exporter of natural gas, expecting to average a net supply of more than 10 Bcf/d in 2017.

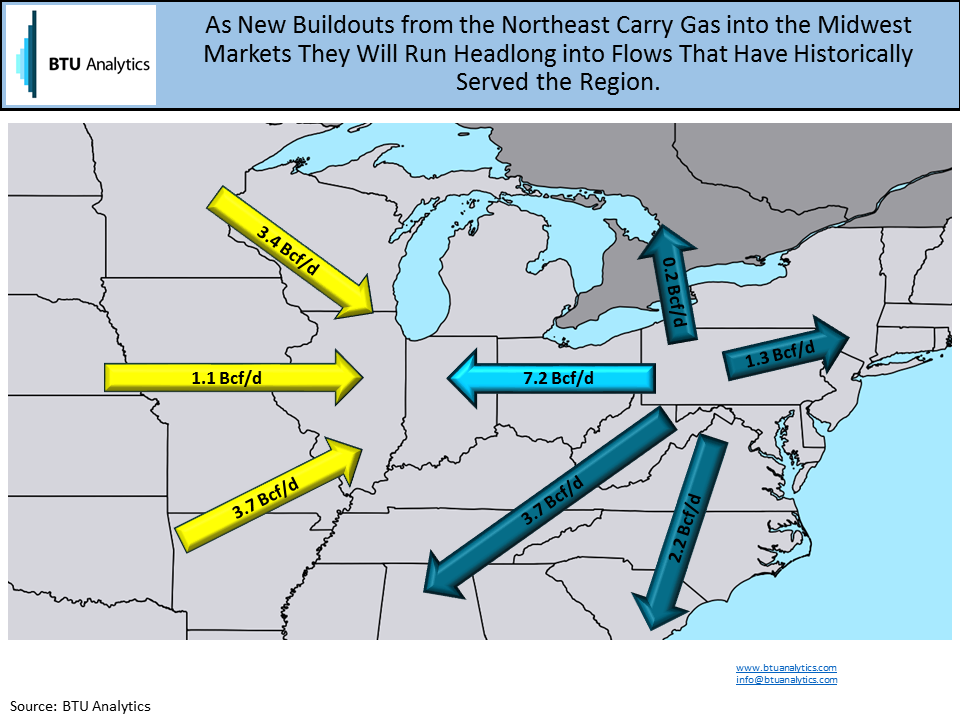

That surplus gas will push out into other regions and, judging by upcoming projects, its most viable paths will be to the Midwest and Gulf markets. If we focus on the Midwest, this deluge of recently freed gas will rush headlong into Canadian, Rockies, and Permian gas that has traditionally served the Midwest. In 2014, these pipes delivered an average of 8.2 Bcf/d to the Midwest market, enjoying an average variable spread between their respective supply markets and the Chicago market of $1.41.

Narrowing our scope, even more, the conflict will be the most pronounced in the upper Midwest’s Michigan and Dawn markets, where both Rover and Nexus are set to deliver significant volumes of gas. This area was once held firmly by long-haul pipes: Great Lakes, Trunkline, Panhandle, ANR, and Vector (supplied by Alliance and ANR). Combined they averaged 4.5 Bcf/d of deliveries into the upper Midwest in 2014, but how will they fare against the soon-to-be flood from the Northeast? And what will be the aftermath on the broader market? Check back to our Energy Market Commentary in the coming weeks for more.