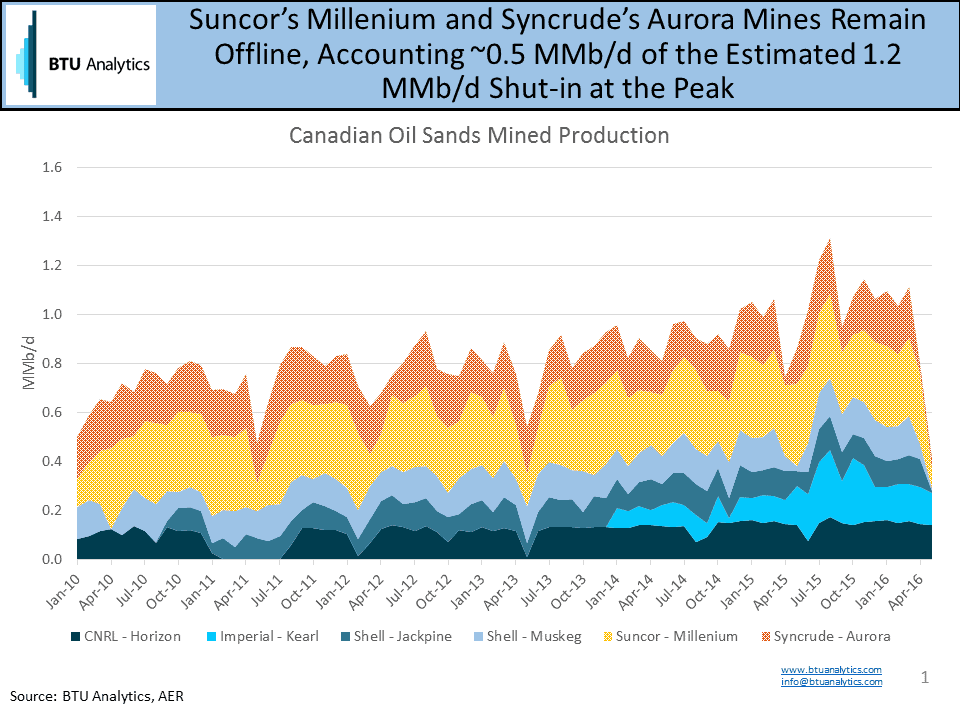

Supply disruptions in Nigeria, potential cutbacks to investment in Iraq, escalating civil unrest in Venezuela, and as much as 1 MMb/d of Canadian production shut-in due to wildfires have the oil bulls emerging from the woodwork. However, it’s important to consider the scale and longevity of these events. While both Nigeria and Venezuela have potential to be longer-term events (could last for 6+ months) the magnitude of production that has been impacted between March and April, according to the IEA, is 160 Mb/d. These declines are easily offset by almost 200 Mb/d of gains in Iraq, 300 Mb/d of gains in Iran, and an additional 100 Mb/d of increased production in the UAE. Ultimately, the biggest impact on oil market pricing in the near term are the shut-ins of the Canadian oil sands mines.

Currently, Suncor’s Millennium and Syncrude’s Aurora mines, which were producing a combined 0.5 MMb/d of mining production in April, are shut-in due to the Canadian wildfires. Additional in situ facilities like Nexen’s Long Lake with a capacity of 72 Mb/d are also idle or operating at reduced capacities. While the duration of this supply disruption is unknown, it is likely to be short-term event. Looking forward to the second half of 2016, bullish market sentiment on Iranian oil production, the restart of Suncor and Syncrude’s mining facilities, and potential increases in production from Saudi Arabia continue to mitigate the impact of sustained declines in Venezuela and potentially Nigeria. While the current WTI strip is averaging $49.53/Bbl between June and December 2016, there is still significant uncertainty in the oil market and BTU Analytics believes the strip is overly bullish for the back half of 2016. At $50/Bbl WTI crude pricing, US crude oil production could begin to stabilize rather than continue its decline, a decline which is necessary to help re-balance the global oil market.

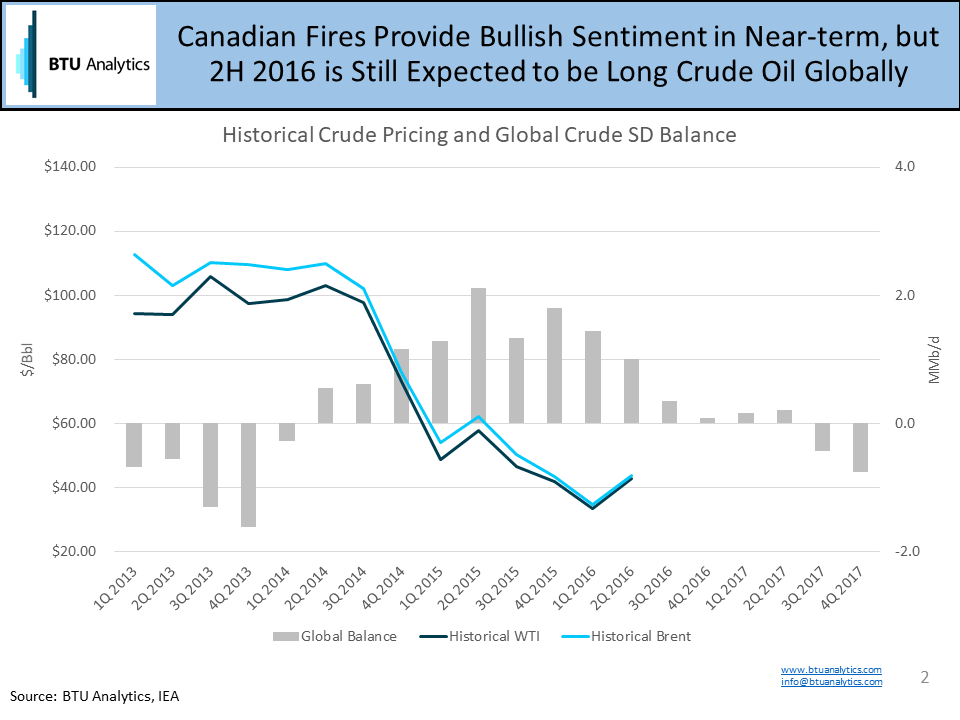

Assuming Canada resumes operations in the next month or two, there have been limited shifts in the overall fundamental picture for the global crude oil market. Despite declining production in Venezuela and Nigeria, without declines in the US, robust growth in Iran, a slowing rate of growth in Iraq, and recovery in Canadian oil production leave the world long crude oil at current strip prices. Not to mention, Saudi Arabia has been increasingly vocal about plans to increase production, limiting the ability for crude prices to go much higher in 2016.

{kind=link}