In the fall of 2014, BTU Analytics released The Battle for Henry Hub – a paper on our 5-year look on natural gas. One of the main challenges we identified was that with $100 WTI and $4 natural gas, almost every North American shale play was economic. The result was that associated natural gas growth from unconventional oil was set to swamp Henry Hub along with prolific Northeast gas production targeting Louisiana through 2018, at which point LNG is expected to save the day. Something had to give. That “something” as everyone is now fixated on, is the weakness in crude oil prices.

The question is, with all the recent E&P capex cut announcements (See December Upstream Outlook for a recap of announcements and their implications), what will be the impact to the natural gas market?

And to be clear, let’s face it, in the short term the gas market is in a bit of a pickle. The storage deficit from the Polar Vortex winter of 2013-2014 has been slowly getting worked off thanks to aforementioned growing supply across almost all regions. This winter got off to a cold start in November but has been a bit of a bust recently helping push prompt month down to $3.15 this week. Unless severe winter weather shows up east of the Mississippi soon, the production momentum from 2014 (which will take months to work off), is going to result in a heavy supply surplus in 2015.

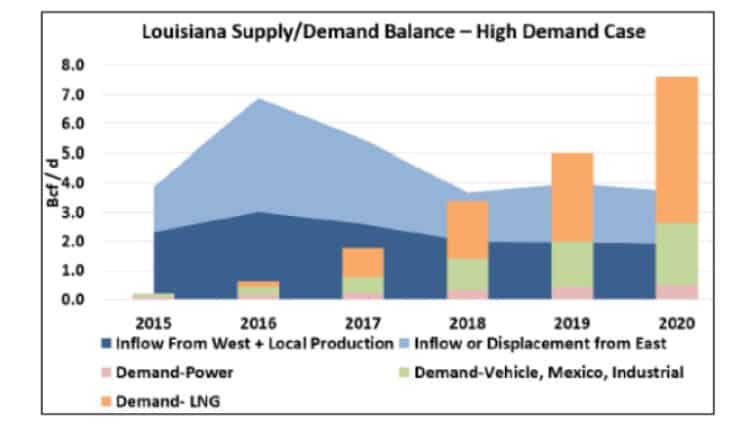

In the medium term however (call it 2016-2018), the US gas market now has a stronger fundamental foundation than it has had in a long time. The impact of weak WTI means that the US natural gas market may get back into a tighter supply demand balance sooner than it would have otherwise. While 2015 may be painful for producers, in 2016, 2017 and 2018 the supply demand balance will tighten incrementally as industrial, power and LNG ramp up on the demand side while supply growth will be slower than previously expected. Below is a chart from the paper showing how we viewed Henry Hub (called Louisiana below) would balance over the next 5 years.

In the Battle for Henry we saw a huge oversupply to the tune of over 6 Bcf/d in 2016 as Louisiana was flooded with production from the Marcellus/Utica via backhaul pipeline projects while gas from the Eagle Ford, Permian, DJ, PRB and Bakken all flooded the market as well.

In BTU Analytics’ forward look on the gas market as laid out in our Upstream Outlook, we see the Northeast being fairly isolated from the impacts of WTI weakness. Yes, marginal players with marginal acreage will get squeezed but we continue to believe that in the core areas of the Northeast producers will fill infrastructure as it becomes available despite weaker realized natural gas liquids prices due to the fall in crude. However, should prices continue to soften into the $2 range at Henry Hub, even Marcellus and Utica producers may see larger budget cuts in 2015. In the mean time, the biggest change to the gas market will come in the form of reduced associated production growth in the West where lower realized oil pricing will remove up to 1 Bcf/d of gas production growth out of 2015, 3 Bcf/d in 2016 and 5 Bcf/d in 2018 as compared to outlooks based on activity just 6 months ago.

There are very few pure-play gas producers left as almost every E&P has been lured by unconventional oil. Perhaps it is time for the oil and gas pendulum to swing back in favor of gas. Southwestern Energy (NYSE: SWN) is one E&P that has stayed the course on natural gas and they have doubled down on gas with recent Northeast acquisitions. At least someone stayed the course on natural gas, however we will have to wait until 2016-2018 to see if their determined strategy will pay off.

Click here to receive our Energy Market Commentary as soon as it’s published