Despite the Brexit, the timing of crude price recovery has been on the minds of many in the energy market. During this recent period of weak pricing, many producers highlighted a key piece of good news amidst the bad: well costs have been brought down significantly across the board. However, those savings have come at the cost of service providers’ profits, and many of those service companies have had their North American margins squeezed to nothing. At some point the pendulum will have to swing the other way, since a business can’t survive with zero or even negative operating margins.

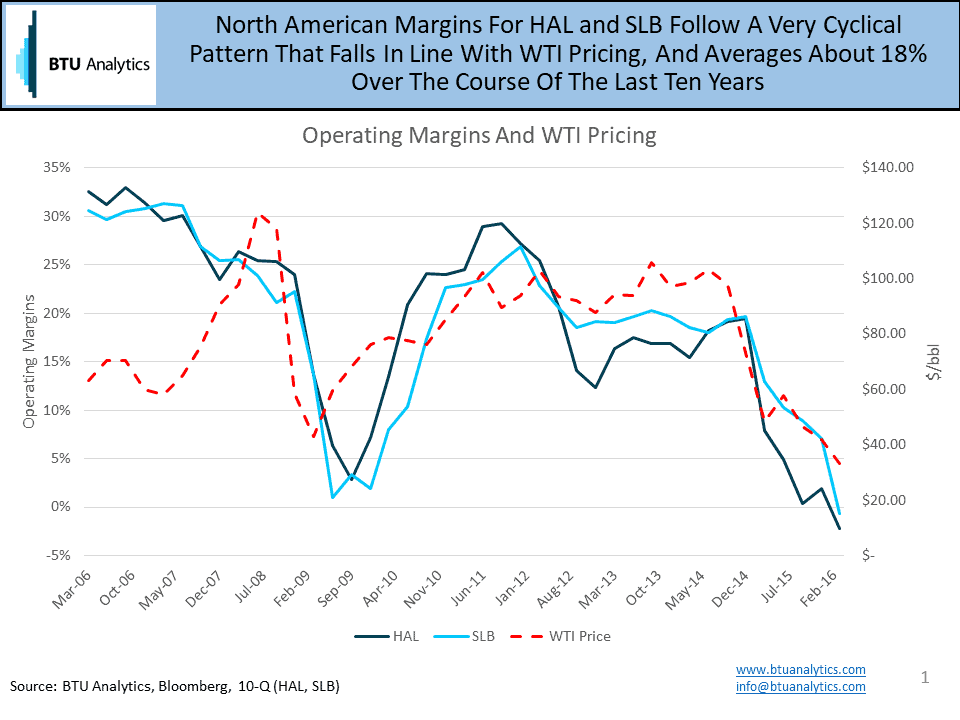

The question that BTU Analytics has set out to answer is just what inflation might we expect to see in well costs, and on what kind of timeline? History provides some interesting perspective. The below graphic shows operating margins for the North American divisions of two of the biggest service companies; Schlumberger (NYSE: SLB), and Halliburton (NYSE: HAL).

The chart shows that margins for these two companies has followed the cyclical trend of WTI very closely since 2008. This gives an indication that as prices make their way back up, operating margins can be expected to do the same thing. Another important metric here is the fact that operating margins average about 18% over this time frame. Using this, as well as the basic assumption of average costs to service providers over the time frame, it can be derived that revenue needs to increase by nearly 60% of what it is today in order to bring margins back to the 10-year average. With a simple model, this means that well costs would need to come up by roughly 60%, or a $5MM well becoming an $8MM well. Increases in service costs will lead to an increase in the price needed for a well to break even. Without getting into a cyclical argument, this will have the effect of the market needing higher prices in order for producers to continue drilling at the same pace. While producers currently are able to tout their low well costs leading to economic drilling even in the weak commodity environment, higher service costs would reduce the economics, to the point where increase in prices could result in only marginal gains in economics.

The other important piece of information that can be pulled from looking at North American operating margins over the past 10 years is the time frame in which the recovery of margins takes place. During the price crash in 2008, margins rebounded back to pre-crash levels in about one year. This points to the fact that it may not take long for margins to come back to their average levels, with one exception; the rebound in crude oil prices for this crash have come at a much slower pace than in 2008.

For a deeper look at how analysis like this impacts other aspects of the market, such as overall production, regional economics, and even wellhead breakevens, be sure to check out BTU Analytics’ Upstream Outlook.