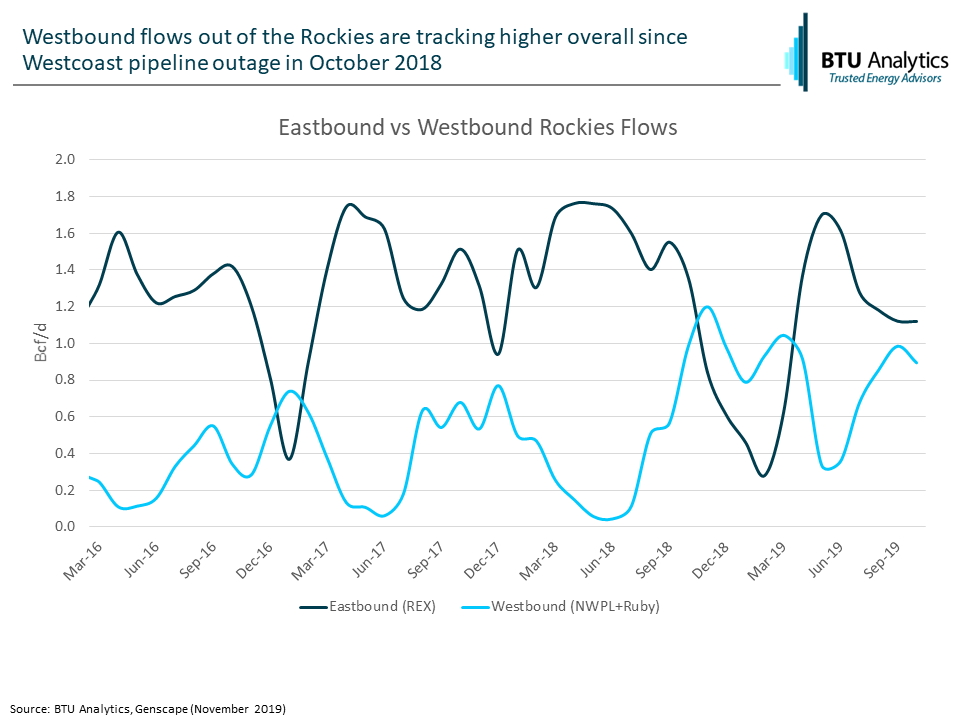

Up until last year, Rockies gas to the West Coast had been on the decline while Rockies gas to the Midwest had been on the rise. However, those dynamics shifted after Enbridge’s Westcoast pipeline ruptured in October 2018. Since the explosion, westbound flows out of the Rockies have risen rapidly at the expense of eastbound flows. Are these dynamics here to stay or will we see a return to the status quo? And how long will Opal natural gas pricing volatility remain?

Historically, flows out of the Rockies have shown substantial seasonal variability. Typically, eastbound flows peak during summer then fall-off during winter when heating demand in Denver and Eastern Colorado ramp up. Westbound flows during winters historically grew as gas was needed in Utah and the Pacific Northwest. However this year, western flows on NWPL and Ruby pipelines in September were almost 80% higher than average September flows over the preceding three years. Conversely, eastern flows on REX were down more than 20% compared to the prior September average.

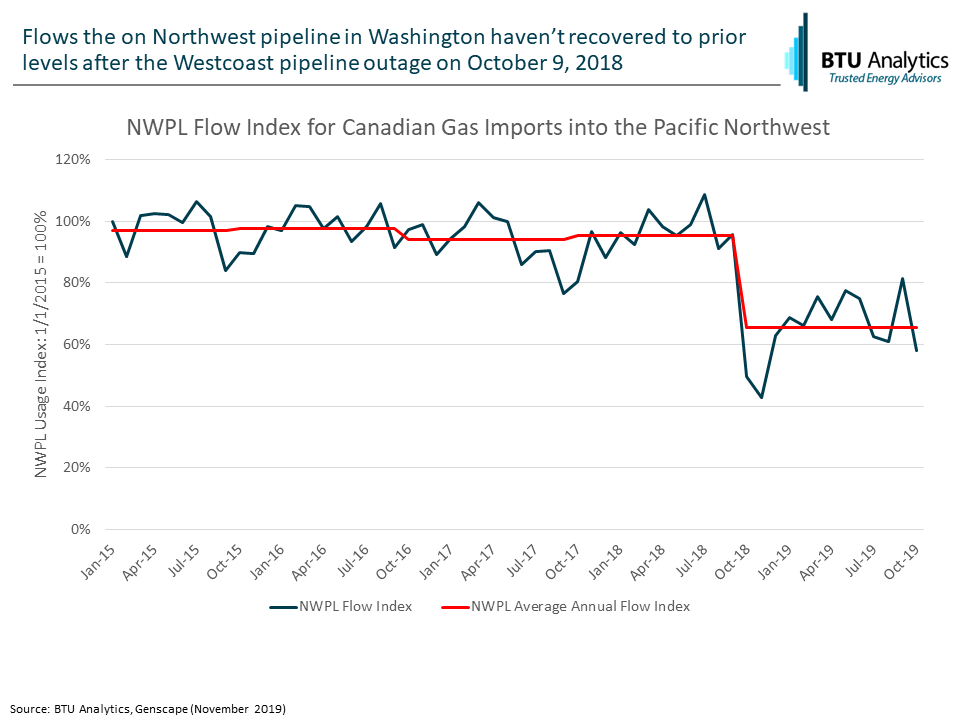

These recent dynamics continue to be driven by the outage on Westcoast pipeline, where imports via NWPL at the Canadian border have still not returned to their pre-outage levels. This has caused the Rockies to strain its limited, east-to-west capacity, in turn driving strength in pricing we will discuss later. Mitigating some of this supply shortfall are expansions of Canadian imports along GTN, 160 MMcf/d which was set to come online this month and additional projects through 2023.

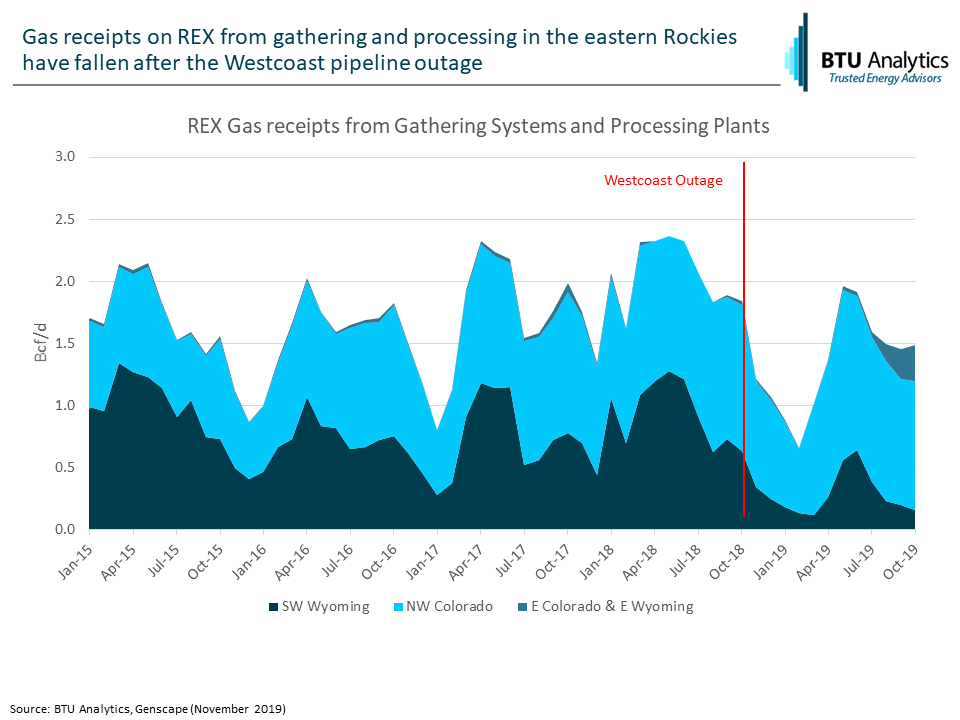

Bridging both the Western and Eastern Rockies, REX plays the role of moving gas from the Western Rockies all the way east to Midwest markets. However, historically REX has sourced the vast majority of its gas from Western Rockies production in the Piceance and Green River. This means that as the shortage in the Pacific Northwest grew, REX eastbound volumes suffered. The graphic below shows REX receipts by area, and despite an uptick in Eastern Colorado volumes, gas on REX is still below historical levels, even after recovering after the sharp drop immediately following the explosion.

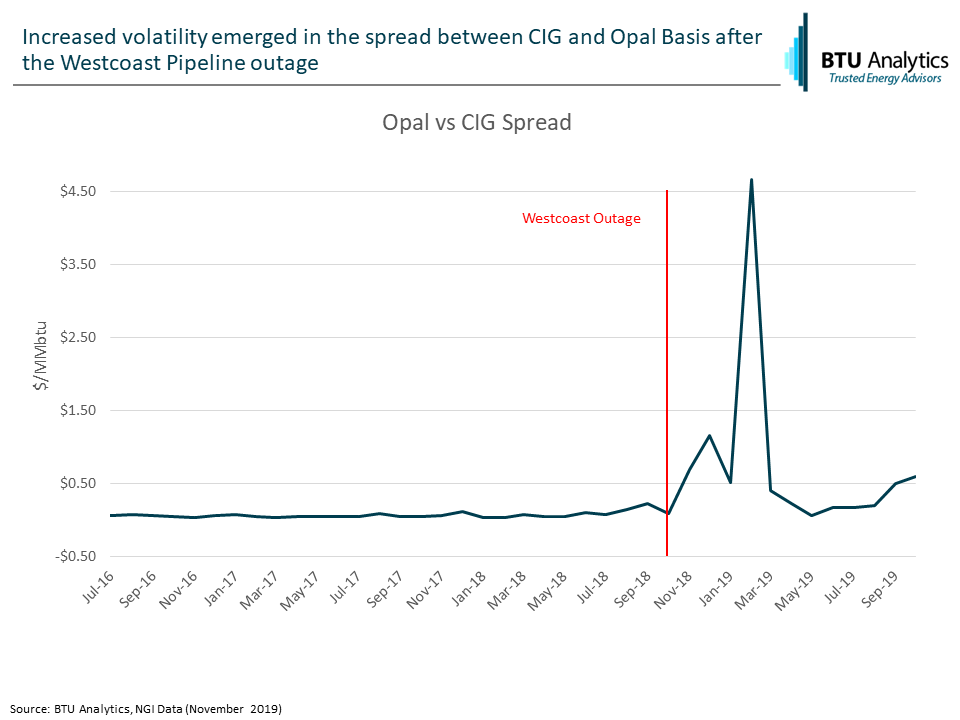

Tallgrass’s Cheyenne Connector, which will connect DJ associated gas production to the Cheyenne Hub, will continue the growth we have seen of REX volumes sourced from Eastern CO/WY. The 600 MMcf/d project slated to come online in the first quarter of 2020, will help to reduce the seasonal volatility in REX eastbound flows, however regardless of how full REX is into the Midcontinent, Rockies infrastructure, as it stands today is unable to solve the shortfall in the Pacific Northwest, as illustrated in the spread between CIG (Eastern Rockies pricing) and Opal (Western Rockies pricing) below.

These spreads within the Rockies have incentivized new east-to-west capacity, with Dominion Energy just closing an open season for its 120 MMcf/d Wamsutter West expansion, which is due to come online before next winter. This sets the stage for volatile Opal natural gas pricing this winter, with the Opal/CIG spread already hitting $1.69/MMBtu in October. While new infrastructure will come online bringing more supply into the West, declining Western Rockies production runs the risk of making this shortfall a more sustained issue. For a complimentary, detailed study on short-term and long-term gas dynamics within the Rockies, email info@btuanalytics.com a with subject line of Rox.